Close-up of hands holding a smartphone with health insurance marketplace application on screen with financial documents glasses and coffee cup blurred in the background

Health Insurance Tax Credit Guide for US Taxpayers

Content

When you shop for health coverage through the federal or state marketplace, you might qualify for financial help that lowers your monthly premium. The health insurance tax credit makes private insurance affordable for millions of Americans who fall within specific income ranges but don't have access to employer-sponsored plans or government programs like Medicaid.

Understanding how this credit works—and how to claim it correctly—can save you thousands of dollars each year. Many people leave money on the table because they don't realize they qualify, or they make simple mistakes during enrollment that cost them later at tax time.

What Is the Health Insurance Tax Credit?

The health insurance tax credit, officially called the Premium Tax Credit (PTC), is a federal subsidy that reduces what you pay for health insurance purchased through the Health Insurance Marketplace. Congress created this credit as part of the Affordable Care Act to bridge the gap between what families can afford and what marketplace plans actually cost.

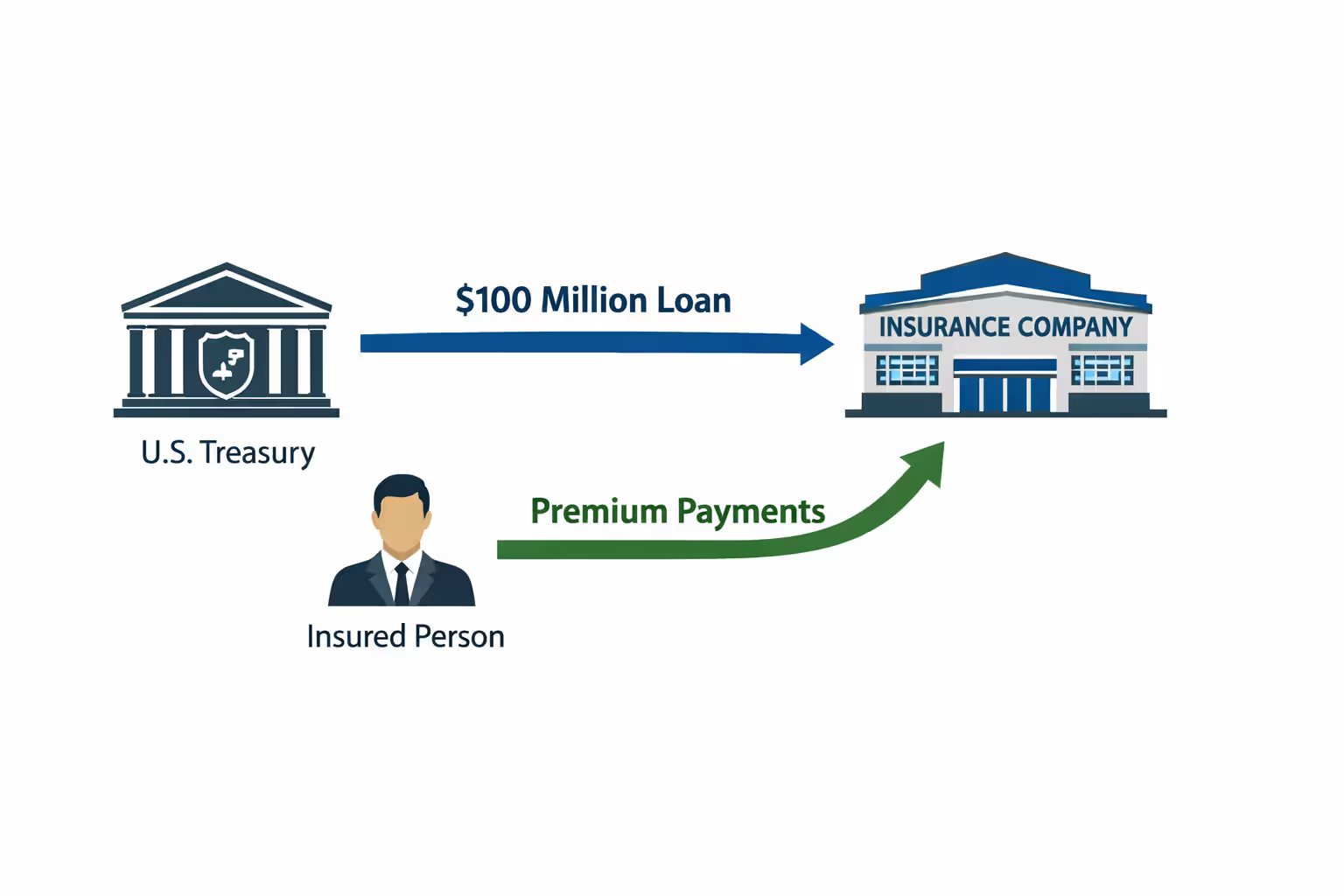

The credit works in two ways. You can receive it as an advance payment sent directly to your insurance company each month, which lowers your premium bill right away. This is called the Advance Premium Tax Credit (APTC). Alternatively, you can pay full price throughout the year and claim the entire credit when you file your federal tax return, receiving it as part of your refund or as a reduction in what you owe.

Most people choose the advance option because it provides immediate relief. If your monthly premium would normally be $650 but you qualify for a $400 credit, you'd only pay $250 each month when the government sends the rest directly to your insurer.

At tax time, the IRS reconciles what you received in advance against what you actually qualified for based on your final income. If your income came in lower than you estimated, you might get additional credit back. If you earned more than expected, you may need to repay some or all of the advance payments, though repayment caps protect most households from owing large amounts.

Author: Melissa Grant;

Source: blaverry.com

The health insurance tax credit explained simply: it's a sliding-scale subsidy that adjusts based on your income and the cost of the benchmark plan in your area. The lower your income relative to the federal poverty level, the larger your credit. The calculation also factors in your household size and local insurance costs, so two families with identical incomes might receive different credit amounts if they live in different states.

Who Qualifies for the Health Insurance Tax Credit

Health insurance tax credit eligibility depends on several factors working together. You must meet all the requirements simultaneously to receive the credit.

Income Limits and Federal Poverty Level Guidelines

Your household income must fall within a specific range relative to the federal poverty level (FPL) for your household size. As of 2026, the American Rescue Plan enhancements remain in effect, eliminating the previous 400% FPL cap. Now, anyone whose marketplace premium for the benchmark plan would exceed 8.5% of their household income qualifies for at least some credit, regardless of how much they earn.

The credit provides the most substantial help to households earning between 100% and 250% of FPL. At these income levels, you'll pay no more than 2% to 6% of your income toward the benchmark plan. As income rises, the percentage you're expected to contribute increases gradually.

Author: Melissa Grant;

Source: blaverry.com

Here's how income affects your credit for 2026:

| Household Size | 100% FPL | 200% FPL | 300% FPL | 400% FPL | Max Income Contribution |

| 1 person | $15,060 | $30,120 | $45,180 | $60,240 | 8.5% of income |

| 2 people | $20,440 | $40,880 | $61,320 | $81,760 | 8.5% of income |

| 3 people | $25,820 | $51,640 | $77,460 | $103,280 | 8.5% of income |

| 4 people | $31,200 | $62,400 | $93,600 | $124,800 | 8.5% of income |

| 5 people | $36,580 | $73,160 | $109,740 | $146,320 | 8.5% of income |

The household income used for these calculations is your Modified Adjusted Gross Income (MAGI), which includes wages, self-employment income, Social Security benefits, investment income, rental income, and certain other sources. It's your adjusted gross income plus any tax-exempt interest and excluded foreign income.

Household size counts everyone you claim on your tax return—yourself, your spouse if filing jointly, and all dependents. A couple with two children counts as a household of four, even if one child lives away at college.

Situations That Disqualify You

Several circumstances make you ineligible for the health insurance tax credit, even if your income falls within the qualifying range.

Access to affordable employer coverage disqualifies you. The IRS defines "affordable" as employer coverage where your share of the premium for self-only coverage costs less than 8.5% of your household income (for 2026). This affordability test applies only to the employee's premium for single coverage, not family coverage, though this creates hardships for families where adding dependents becomes unaffordable.

Eligibility for most other coverage types also disqualifies you. If you qualify for Medicaid, Medicare, CHIP, TRICARE, or veterans' health benefits, you cannot receive the premium tax credit, even if you choose not to enroll in those programs. The exception: being eligible for coverage under someone else's employer plan doesn't disqualify you unless that coverage meets the affordability and minimum value standards.

Immigration status matters. You must be a U.S. citizen or lawfully present immigrant to qualify. Undocumented immigrants cannot receive the credit, though some states offer similar subsidies through state-funded programs.

You must file a federal tax return to claim the credit. Those who file as "married filing separately" generally cannot claim it, with limited exceptions for domestic abuse survivors.

Incarcerated individuals cannot receive the credit while imprisoned, though they regain eligibility upon release.

How the Health Insurance Tax Credit Works

Understanding how does health insurance tax credit work requires following the money through two distinct phases: the advance payment during the coverage year and the reconciliation when you file taxes.

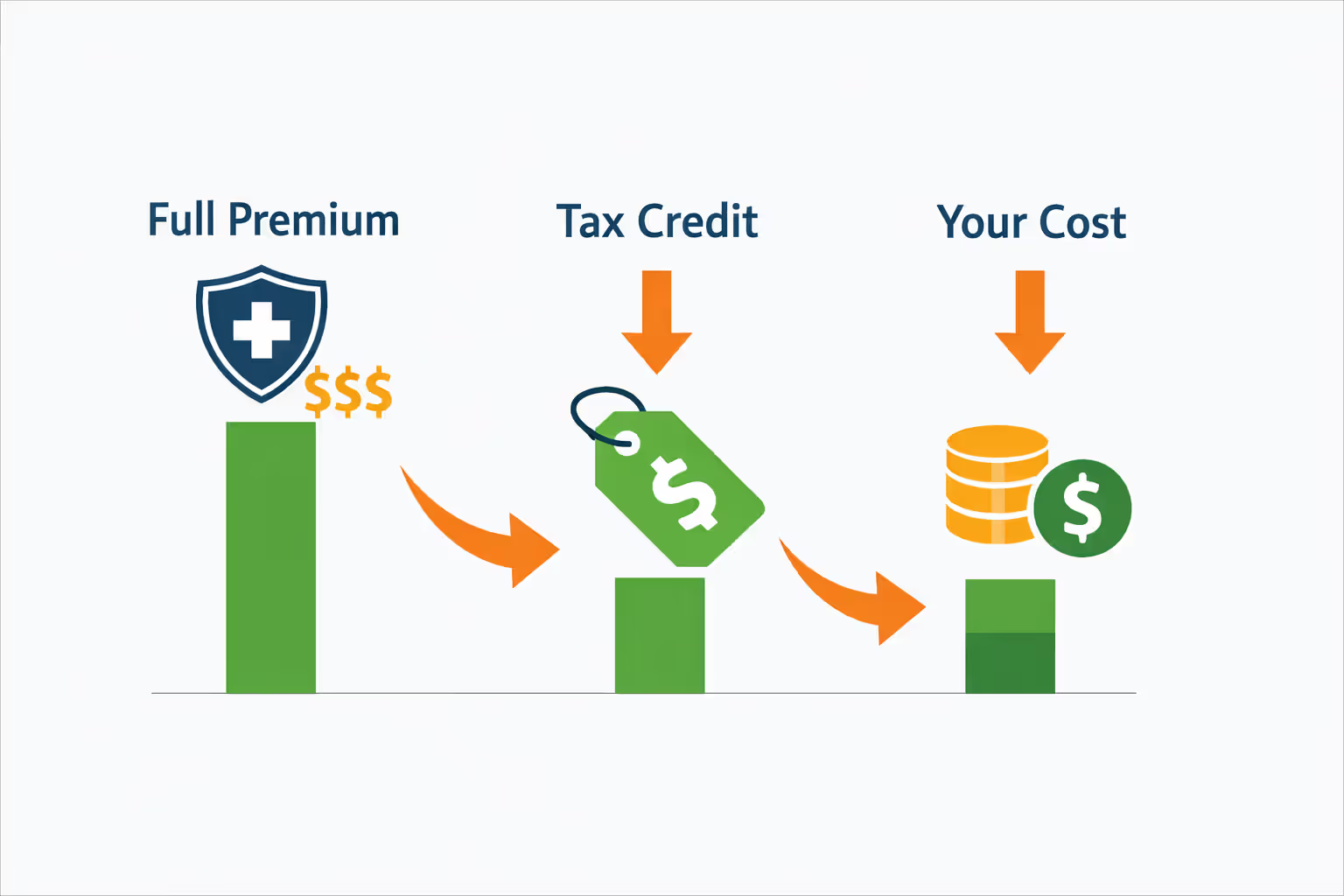

When you apply for marketplace coverage, you estimate your income for the upcoming year. The marketplace uses this estimate to calculate your expected credit amount based on the benchmark plan—the second-lowest-cost Silver plan available to your household in your county. This benchmark serves as the reference point regardless of which plan you actually select.

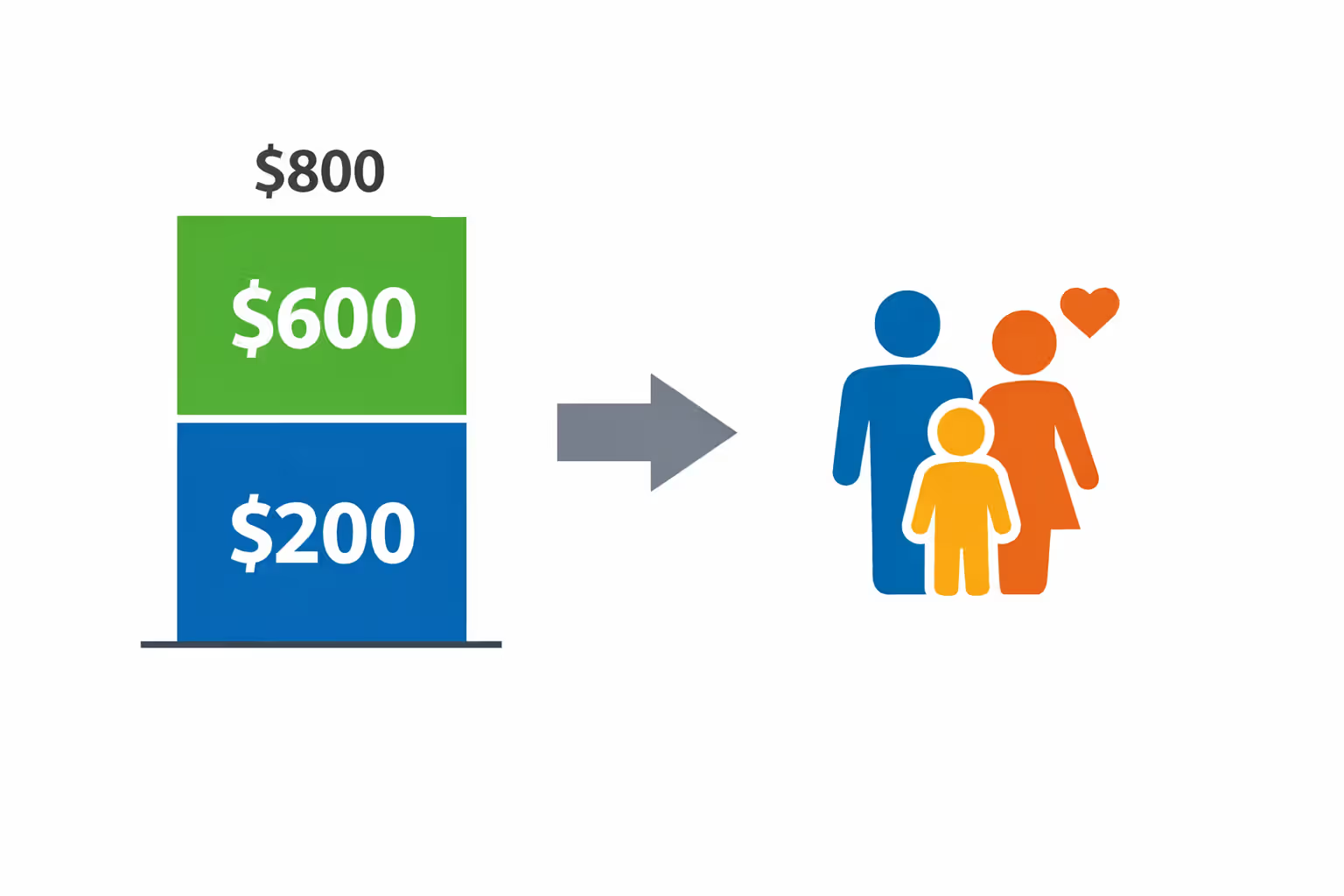

The credit amount equals the difference between the benchmark plan's full premium and what you're expected to contribute based on your income percentage. If the benchmark plan costs $800 monthly and your expected contribution is $200, your credit is $600 per month.

Author: Melissa Grant;

Source: blaverry.com

You then choose any marketplace plan—Bronze, Silver, Gold, or Platinum. If you select a plan cheaper than the benchmark, your credit might cover most or all of the premium. If you choose a more expensive plan, you'll pay the difference out of pocket. The credit amount stays the same regardless of which plan you pick; it's always based on the benchmark.

Most people authorize the government to send their credit directly to their insurance company each month. This advance payment immediately reduces what you owe. You never see this money yourself—it flows from the Treasury to your insurer automatically.

During the year, your actual income might differ from your estimate. You might get a raise, lose a job, start a business, or experience investment gains or losses. Your household size might change through birth, adoption, marriage, or divorce. These changes affect your credit eligibility, which is why the marketplace encourages you to report them promptly. Updating your information allows the marketplace to adjust your advance payments, preventing large repayment obligations or ensuring you receive the full credit you deserve.

When you file your federal tax return using Form 8962, the IRS compares your actual income and household circumstances against the advance payments you received. If you qualified for more credit than you received in advance—perhaps because your final income was lower than estimated—you claim the additional amount on your return, increasing your refund or reducing what you owe. If you received more in advance than you qualified for, you repay the excess, though repayment caps limit how much you must return based on your income level.

For 2026, repayment caps range from $350 for single filers earning under 200% FPL to $3,000 for those earning between 300% and 400% FPL. Above 400% FPL, no cap applies—you must repay the full excess amount.

How to Apply for the Health Insurance Tax Credit

Claiming the tax credit for health insurance starts with enrolling in a marketplace plan, not with filing your tax return. You cannot receive the credit for coverage purchased directly from an insurance company outside the marketplace, even if the plan is identical.

Visit HealthCare.gov or your state's marketplace during open enrollment, which for 2026 runs from November 1, 2025, through January 15, 2026, for coverage starting January 1. Some states extend their enrollment periods longer. Special enrollment periods allow sign-up outside these dates if you experience qualifying life events like losing other coverage, moving, getting married, or having a baby.

Create an account and start an application. You'll need Social Security numbers for everyone in your household, income information, and details about any current health coverage offers. The application asks about your expected household income for 2026. This requires some estimation, especially if you're self-employed or your income varies.

Estimate conservatively but realistically. Look at last year's tax return as a starting point, then adjust for known changes—a new job, a raise, reduced hours, or retirement. For self-employed individuals, consider seasonal fluctuations and whether you're growing or scaling back. When in doubt, estimate slightly higher rather than lower; receiving a larger credit at tax time is better than owing repayment.

The marketplace instantly determines whether you qualify for the credit and calculates the monthly amount. You'll see this reflected as you shop plans. Each plan displays two prices: the full premium and your cost after the advance credit is applied.

Choose your plan carefully. The credit makes Silver plans particularly attractive because they come with cost-sharing reductions if your income falls below 250% FPL. These reductions lower your deductibles, copays, and out-of-pocket maximums beyond what the premium credit provides, but they only apply to Silver plans.

Author: Melissa Grant;

Source: blaverry.com

During enrollment, you'll decide whether to apply your credit in advance or wait until tax time. Nearly everyone chooses advance payments for the immediate monthly savings. You can choose to apply only part of your credit in advance and claim the rest on your tax return if you want to be extra cautious about potential repayment.

After enrolling, your coverage starts on your effective date, and advance payments begin flowing to your insurer. Throughout the year, log into your marketplace account to report changes. Got a raise in March? Report it. Had a baby in July? Report it. Lost your job in October? Report it immediately—you might qualify for more credit or even become eligible for Medicaid.

The health insurance tax credit timeline extends beyond enrollment. You'll receive Form 1095-A from the marketplace by mid-February following the coverage year. This form shows your monthly premium amounts, advance credit payments, and benchmark plan costs. You need this form to complete Form 8962 when filing your federal tax return, which reconciles everything and determines whether you receive additional credit or owe repayment.

Documents and Information You Need

Gathering the health insurance tax credit documents needed before you start your application speeds up the process and improves accuracy.

For initial enrollment, collect recent pay stubs if you're employed, showing year-to-date earnings. Self-employed individuals should have their most recent tax return and current-year income records. If you receive Social Security, have your benefits statement. Gather information about any other income sources: unemployment benefits, pension payments, rental income, investment earnings, or alimony.

You'll need Social Security numbers for everyone in your household, including dependents. Immigration documents are required for non-citizens. If anyone in your household has an offer of employer coverage, get the details about the premium cost and what the plan covers—you might need the employer's Summary of Benefits and Coverage.

During the coverage year, keep records of any changes that affect your eligibility. Document marriage with a marriage certificate, new children with birth certificates, address changes with moving receipts, and income changes with pay stubs or termination letters.

When tax time arrives, you need Form 1095-A from the marketplace. This form is essential—you cannot accurately complete Form 8962 without it. If you don't receive it by mid-February, download it from your marketplace account or contact the marketplace helpline.

You'll also need your usual tax documents: W-2s from employers, 1099 forms for other income, records of deductions and credits, and documentation for any dependents you're claiming. Form 8962 requires specific information from your 1095-A, including the monthly premium amounts, second-lowest-cost Silver plan premiums, and advance payment amounts.

Keep copies of everything for at least three years. If the IRS questions your credit calculation, you'll need documentation to support your household composition, income figures, and eligibility determinations.

Author: Melissa Grant;

Source: blaverry.com

Common Mistakes and How to Avoid Them

Income estimation errors cause the majority of problems with health insurance tax credit reconciliation. Underestimating income by $10,000 might mean receiving $200 extra in monthly credits—$2,400 over the year—that you'll need to repay at tax time. While repayment caps limit the damage for lower-income households, they don't eliminate it, and higher earners face unlimited repayment obligations.

Build a buffer into your estimate. If you think you'll earn $48,000, estimate $50,000. If you're self-employed and had a great year last year, don't assume identical results—consider whether market conditions have changed. Factor in one-time income events like selling investments or taking retirement distributions.

Failing to report life changes during the year compounds estimation errors. You got divorced in March, reducing your household size and changing your income, but you didn't update the marketplace. You switched jobs in June with a $15,000 salary increase, but you didn't report it. Come tax time, the reconciliation reveals you received thousands more in credits than you qualified for.

The marketplace makes reporting changes easy through your online account. Set a reminder to review your information quarterly. Major changes—marriage, divorce, birth, job loss, significant raises—should be reported within 30 days.

Not reconciling at tax time is illegal and costly. Some people who receive advance credits simply don't file taxes, thinking they're avoiding repayment. The IRS will eventually catch up, and you'll lose eligibility for future advance credits until you file all missing returns and reconcile properly. You might also face penalties and interest on unpaid taxes.

Missing enrollment deadlines leaves you uninsured and ineligible for credits until the next enrollment period. Mark your calendar for November 1 when open enrollment begins. If you qualify for a special enrollment period due to a life change, you typically have 60 days from the event to enroll—don't wait until day 59.

Choosing the wrong plan relative to the benchmark sometimes happens when people don't understand how the credit works. Someone sees a Bronze plan for $50 per month after credits and a Gold plan for $300 per month after credits and assumes the Bronze plan is saving them money. But if the Gold plan offers significantly better coverage and they have health needs, paying extra might be worthwhile. The credit amount is the same either way—it's based on the benchmark, not your choice.

Forgetting about cost-sharing reductions leaves money on the table. If your income is below 250% FPL, Silver plans come with enhanced benefits that dramatically lower your out-of-pocket costs. A Silver plan might cost slightly more monthly than a Bronze plan, but the reduced deductibles and copays often make it cheaper overall if you use healthcare services.

The premium tax credit is one of the most valuable yet misunderstood tax benefits available to Americans. The biggest mistake I see is people not updating their income estimates when circumstances change. A new job or a spouse returning to work can shift you into a different credit bracket, and reporting these changes promptly prevents sticker shock at tax time

— Maria Gonzalez

Frequently Asked Questions About Health Insurance Tax Credits

The health insurance tax credit makes private coverage accessible to millions of Americans who would otherwise find marketplace premiums unaffordable. By understanding the eligibility rules, applying correctly, and staying on top of life changes throughout the year, you can maximize this benefit while avoiding repayment surprises at tax time.

Start by estimating your income carefully, building in a reasonable buffer for uncertainty. Enroll during the open enrollment period or within 60 days of a qualifying life event. Choose your plan strategically, considering both the premium after credits and the out-of-pocket costs you'll face when using care. If your income falls below 250% of the federal poverty level, Silver plans with cost-sharing reductions often provide the best overall value.

Throughout the coverage year, treat your marketplace account like you treat your bank account—check it periodically and update it when circumstances change. A new job, a lost job, marriage, divorce, a new baby, or a significant income shift all warrant immediate reporting. These updates keep your advance credits aligned with your actual eligibility, smoothing out the reconciliation process.

When tax season arrives, don't ignore Form 1095-A or skip Form 8962. Proper reconciliation protects your eligibility for future credits and ensures you receive every dollar you've earned. If you owe repayment, remember that caps limit your exposure for most income levels, and payment plans are available if needed.

The credit exists to help working families afford quality health coverage. Millions of Americans qualify but never apply, assuming they earn too much or that the process is too complicated. Take the time to check your eligibility—you might be surprised at how much assistance is available. With premiums rising faster than wages in many markets, the health insurance tax credit often makes the difference between having coverage and going uninsured.