Top-down view of a desk with health insurance documents, laptop, calculator, pen, glasses, and coffee mug in warm autumn lighting

What Is Open Enrollment for Health Insurance

Content

Every fall, millions of Americans face a decision that affects their wallet and wellbeing for the next twelve months: choosing health insurance during open enrollment. You've probably received those emails from HR or seen HealthCare.gov commercials reminding you the clock is ticking. But here's what makes this different from buying almost anything else—you can't just decide to get coverage on a random Tuesday in March when you're feeling worried about that persistent cough.

Health insurance operates on a strict schedule. There's a specific window each year, usually lasting a few weeks to a couple months, when you're allowed to sign up, switch carriers, or adjust your plan. Miss it, and you're stuck until next year (barring major life changes like losing your job or having a baby).

Why such rigid rules? Insurance companies need to prevent what they call adverse selection. Imagine if you could buy car insurance the moment after you crashed—that's essentially what would happen if people could purchase health coverage only when they got sick. The whole system would collapse because nobody would pay premiums while healthy. Designated enrollment periods force everyone into the pool together, spreading risk and keeping costs manageable.

Understanding Open Enrollment Basics

Think of open enrollment as your annual permission slip to change health insurance. It's a limited stretch of time—different for different types of coverage—when you can sign up fresh, jump to a new plan, or tweak what you already have. No explanations needed, no proof required that your life circumstances changed.

This matters for several types of insurance: the coverage you get through work, plans you buy yourself through government Marketplaces, Medicare for seniors, and various state programs. They each run on their own timeline, though there's some coordination to avoid total chaos.

The Affordable Care Act in 2014 really cemented this system for individual insurance. Before that law, you were mostly at the mercy of whatever rules each insurance company felt like following. One might let you sign up in July, another only in October, and a third might reject you entirely because of a pre-existing condition. Now there's structure—federal and state Marketplaces open simultaneously, giving everyone predictable access.

What can you actually do during this window? Pretty much anything except travel back in time. Switch from Blue Cross to Aetna. Add your spouse or new baby. Drop coverage because you're moving to a spouse's plan. Change from a high-deductible plan to one with better upfront coverage. Or drop insurance entirely, though that's rarely wise.

Outside this window, insurance companies operate under a "sorry, come back next year" policy. There are exceptions—Special Enrollment Periods that we'll get to later—but the default is that you're locked into your choices for twelve months.

Here's why this matters beyond just bureaucracy: your life changes. Maybe you got diagnosed with diabetes and need better prescription coverage. Perhaps your favorite doctor switched hospital systems and isn't in your network anymore. Your income might have dropped, making you eligible for subsidies you didn't qualify for last year. Treating open enrollment like an annual physical for your insurance—not just auto-renewing and hoping for the best—can save you serious money and headaches.

When Open Enrollment Happens

The calendar for health insurance enrollment looks different depending on where you're getting coverage. Let's break down each category so you're not caught off guard.

Marketplace coverage through HealthCare.gov: For people buying their own insurance through the federal exchange, the 2026 enrollment window opens November 1, 2025 and closes January 15, 2026. That's roughly ten and a half weeks. The wrinkle here is when your actual coverage kicks in. Sign up by mid-December (specifically the 15th), and you're covered starting New Year's Day. Wait until late December or early January to enroll, and your coverage won't activate until February 1. Those first few weeks of January, you're technically uninsured.

The timeline has expanded considerably from earlier years. Back in 2017 and 2018, the window was half as long—just six weeks in some states. Consumer advocates fought for extensions because people were missing deadlines, and the longer period gives you time to actually compare plans instead of panic-selecting the first option you see.

State-run exchanges: Thirteen states plus DC run their own Marketplaces, and they set their own rules. California routinely keeps enrollment open until the end of January. New York has experimented with year-round enrollment for certain programs. Colorado, Massachusetts, and others pick dates that roughly align with federal timelines but might extend a week or two beyond. If you live in one of these states, check your specific exchange website rather than assuming federal dates apply.

Medicare: The Medicare enrollment calendar follows a completely different rhythm. Open enrollment runs from mid-October through early December—specifically October 15 to December 7 for 2025 coverage starting in 2026. That's less than eight weeks, notably shorter than Marketplace timelines. Changes you make take effect on January 1.

There's also a Medicare Advantage disenrollment window from January 1 through March 31, which lets people bail on Advantage plans and return to original Medicare if they're unhappy. And if you're turning 65, you get a seven-month Initial Enrollment Period centered around your birthday month—three months before, your birthday month itself, and three months after.

Workplace insurance: This is the wild west of timelines because your employer decides when to run enrollment. Most companies pick October or November to align roughly with calendar-year coverage starting January 1. But I've seen employers run it in August, September, even December for January coverage.

If your company operates on a fiscal year that doesn't match the calendar—say July 1 to June 30—they might run open enrollment in May or June. Small businesses sometimes run it whenever they feel like renegotiating with their insurance broker. Point is: watch for communications from HR because you can't assume any particular dates.

Author: Lauren Prescott;

Source: blaverry.com

How the Enrollment Process Works

Enrolling isn't complicated, but it does require some methodical steps. Rushing through it leads to expensive mistakes.

Start with a coverage audit. Pull out last year's explanation of benefits statements—those confusing documents your insurer mails after every medical visit. Add up what you actually spent: premiums (your monthly payments), your deductible (what you paid before insurance kicked in), copays, coinsurance, prescriptions. Did you hit your deductible? Come close? Not even reach halfway? This baseline tells you whether you need robust coverage or can risk a high-deductible plan.

Check if your doctors are still in-network. Networks shift every year as insurers renegotiate contracts. Your dermatologist might have accepted your plan in 2025 but dropped it for 2026. Call their office directly and ask—don't trust online directories, which lag behind real-world changes by months.

Gather your paperwork next. You'll need Social Security numbers for everyone you're covering. If anyone isn't a U.S. citizen, have their immigration documents ready. Pull your most recent pay stubs or last year's tax return to verify income—this determines subsidy eligibility for Marketplace plans. If you're switching from another insurer, have your current policy information handy with coverage end dates.

Author: Lauren Prescott;

Source: blaverry.com

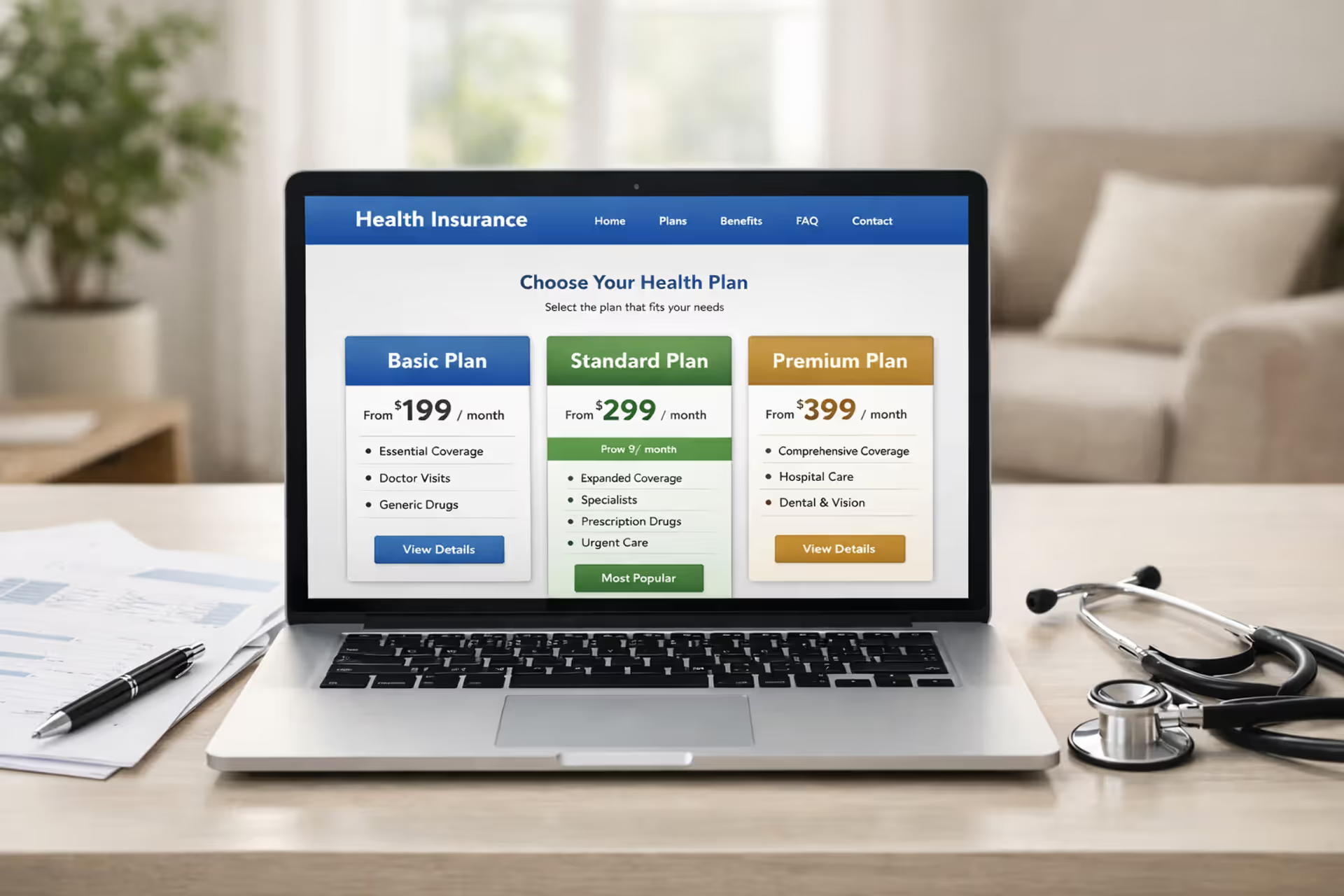

Now compare options. For Marketplace plans, log into HealthCare.gov (or your state exchange) and enter household details. The system shows available plans with their monthly premiums, deductibles, maximum out-of-pocket limits, and which doctors/hospitals participate. Sort by different factors—lowest premium, lowest deductible, best coverage for your specific prescriptions.

Employer plans typically display through your benefits portal at work. You'll see options labeled something like "Gold PPO," "Silver HMO," "Bronze HDHP"—essentially low/medium/high coverage levels. Some employers offer just two choices, others have six or seven.

Medicare folks use the Plan Finder at Medicare.gov, which lets you enter your prescriptions and preferred pharmacies to see which Part D and Medicare Advantage plans cost least for your specific situation.

Run the math beyond premiums. This is where most people mess up. You see "$150/month" versus "$350/month" and immediately pick the cheaper one. But that $150 plan might have a $7,500 deductible while the $350 plan has a $1,500 deductible. If you have planned surgery next year, the expensive-premium plan actually saves you $2,400 overall ($200/month more in premiums = $2,400 annually, but you save $6,000 on the deductible difference).

Factor in regular costs. If you take three prescriptions monthly and visit a specialist quarterly, calculate those expenses under each plan. A plan with $5 generic copays beats one with $25 copays by $720/year if you take three generics—potentially offsetting premium differences.

Submit your application carefully. Marketplace applications take 25-40 minutes for most people. You're answering questions about income, household size, current coverage, tobacco use, and more. Double-check birth dates and Social Security numbers—transposed digits cause weeks of processing delays.

Employer enrollment happens through your company's system, often requiring active selection even if you're keeping the exact same plan. Some companies auto-enroll you in the default option if you ignore it; others cancel your coverage entirely if you don't respond.

Medicare changes can happen online at Medicare.gov, by calling 1-800-MEDICARE, or through paper forms if you're old-school.

Confirm everything and pay up. You'll get confirmation within days for most enrollments. For Marketplace plans, coverage only becomes real after you pay your first premium—they'll send a bill or provide payment instructions. Employer plans usually deduct from your first paycheck. Medicare sends written confirmation that you should file with important documents.

Who Qualifies for Open Enrollment

Not everyone can buy every type of insurance. Eligibility rules differ significantly depending on what kind of coverage you're pursuing.

Marketplace plans through HealthCare.gov or state exchanges: You need to be a U.S. citizen or lawfully present immigrant living in the United States. You can't be incarcerated (though people about to be released can enroll for post-release coverage). You must reside in the state where you're purchasing insurance.

Here's what doesn't matter for basic eligibility: your income level, health status, or pre-existing conditions. Cancer survivors, diabetics, people with heart disease—everyone gets access during open enrollment. However, income affects whether you qualify for financial help. The subsidy formulas use Modified Adjusted Gross Income and compare it to federal poverty levels.

For 2026, individuals making up to 400% of poverty level definitely qualify for premium tax credits. Recent legislation extended subsidies beyond that ceiling, preventing the "subsidy cliff" where earning one dollar too much meant losing thousands in help. Additionally, those earning 250% of poverty or less get cost-sharing reductions that lower deductibles and copays—but only on Silver-tier plans.

If you're eligible for Medicare, you generally can't buy Marketplace coverage, though there are narrow exceptions for people under 65 with Medicare due to disability who want additional coverage.

Employer-sponsored plans: Your company writes the rules within legal boundaries. Most require 30 hours per week to qualify as full-time under ACA definitions. New employees usually face waiting periods—legally these can't exceed 90 days, but many companies offer immediate or 30-day eligibility.

For dependents, you can typically cover your legal spouse and children up to age 26. That age 26 rule is firm and doesn't depend on whether your kid is in school, married, living at home, or financially independent. Some employers extend coverage to stepchildren while they're in your household, domestic partners in states recognizing those relationships, or even adult children with disabilities beyond age 26.

Here's a tricky situation: what if your spouse has insurance through their job? Some employers won't let you add a spouse with "other available coverage" to your plan, or they charge a significant premium surcharge—sometimes $100-$200 monthly—to discourage it. Check your specific employer's rules in the benefits guide.

Medicare: You're eligible at 65 if you or your spouse worked and paid Medicare taxes for at least 40 quarters (ten years). This gets you premium-free Part A (hospital insurance). Part B (outpatient/doctor coverage) requires monthly premiums but is available to anyone who qualifies for Part A.

People under 65 can access Medicare after receiving Social Security Disability Insurance for 24 months, or if they have End-Stage Renal Disease requiring dialysis or a kidney transplant, or if they have ALS (Lou Gehrig's disease, which has no waiting period).

Your first opportunity to enroll begins three months before the month you turn 65 and extends three months after—a seven-month window total. If you miss it, you'll pay late enrollment penalties permanently: 10% added to your Part B premium for each 12-month period you were eligible but didn't enroll. For someone paying $175 monthly for Part B, waiting two years means an extra $35/month penalty forever.

Medicaid: Income requirements vary dramatically by state. The 33 states (plus DC) that expanded Medicaid cover adults earning up to 138% of federal poverty—about $20,783 for an individual or $35,632 for a family of three in 2026. Non-expansion states mostly limit Medicaid to pregnant women, children, disabled individuals, and extremely low-income parents—sometimes requiring income below 40% of poverty.

Unlike other insurance types, Medicaid has no open enrollment restriction. You can apply any day of the year if you meet eligibility requirements. Approval typically happens within 45 days, though expedited processing exists for pregnant women and emergency situations.

Special Enrollment Periods and Exceptions

Life events don't wait for convenient scheduling. Special Enrollment Periods create escape hatches from the annual enrollment calendar when your circumstances change dramatically.

Losing existing coverage is the most common trigger. You lose your job and the employer coverage that came with it—you've got 60 days from your last day of coverage to enroll elsewhere. Same thing if you age off a parent's plan at 26, get divorced and lose spousal coverage, or experience Medicaid closure because your income increased.

Important distinction: the loss has to be involuntary or due to circumstances beyond your control. If you simply stop paying premiums and get canceled, that doesn't qualify. If you voluntarily quit your job, that does trigger special enrollment (even though quitting was your choice, losing the insurance wasn't).

Author: Lauren Prescott;

Source: blaverry.com

Getting married opens a 60-day window starting from your wedding date. You can add your new spouse to your existing plan, join their coverage, or apply together for a new Marketplace plan. This applies to legal marriages recognized by your state.

Domestic partnerships are trickier—they trigger special enrollment only in states that grant them the same legal standing as marriage for insurance purposes. In most states, moving in together or having a commitment ceremony without legal marriage doesn't qualify.

Having or adopting a baby gives you 60 days to add your child to coverage or switch to a family plan. This includes foster care placement, though the rules vary slightly by state. Some people use this opportunity strategically—if you're on a high-deductible individual plan and have a baby, you might switch to a low-deductible family plan to cover all those pediatric visits and vaccinations.

Moving to a new area qualifies only if you're relocating permanently to a ZIP code or county with different health plan availability. This means you can't trigger special enrollment by moving across town within the same city. College students moving to dorms don't qualify because it's temporary—they maintain permanent residence at their family home.

Military deployments and returns do trigger special enrollment with specific rules under TRICARE. Active duty members have more flexibility than civilian populations for obvious reasons.

Gaining citizenship or lawful immigration status provides a one-time enrollment opportunity. If you were undocumented and gain DACA status, become a legal permanent resident, or achieve citizenship, you get 60 days from the status change date to enroll in Marketplace coverage.

Income changes sometimes qualify, particularly if you become newly eligible for premium tax credits, lose subsidy eligibility, or become Medicaid-eligible. The rules here get complex and depend on whether the income change crosses specific thresholds. A 10% raise typically doesn't trigger anything, but losing your job and halving your income definitely does.

Errors by the Marketplace or insurers can create special enrollment rights. If the website enrolled you in the wrong plan due to technical glitches, or a representative gave you incorrect information that led to bad choices, you may get a correction window. You'll need documentation proving the error wasn't your fault.

Documentation requirements are strict across all Special Enrollment Periods. Plan to provide proof: marriage certificates, birth certificates, hospital discharge papers, letters from previous insurers confirming coverage termination dates, employer separation notices, or immigration papers. Marketplaces verify these documents carefully because, frankly, people sometimes lie to game the system. The verification usually takes a few days to two weeks.

Common Open Enrollment Mistakes to Avoid

Expert Perspective:

Most people treat health insurance enrollment like renewing a magazine subscription—something you click through quickly and forget.But this is probably your second-biggest household expense after rent or mortgage. I've seen families spending $8,000-$15,000 annually on premiums and medical costs who never bother comparing alternatives. Investing even two or three hours during open enrollment to genuinely evaluate options—not just hitting 'renew'—routinely saves clients $2,000 to $4,000 per year. The system punishes passive behavior and rewards people who engage actively with the details

— Jennifer Martinez

Even experienced enrollees make careless errors that cost hundreds or thousands of dollars. Here's what to watch for.

Missing deadlines causes the most regret. November feels far from January—you've got time, you tell yourself. Then Thanksgiving hits, followed by December holiday madness, and suddenly it's January 16 and you're locked out. I've talked to people who missed coverage for an entire year because they thought they had until "the end of January" when their specific deadline was mid-December.

Set phone calendar alerts for three dates: the first week enrollment opens (to start gathering documents), two weeks before the deadline (to begin serious comparison), and three days before the deadline (last chance panic alarm). If you're comparing employer plans, note that workplace deadlines usually fall before Marketplace deadlines—often by several weeks.

Auto-renewal without reviewing changes wastes money consistently. Your insurer automatically continues your current plan if you ignore open enrollment. Sounds convenient, right? Except premiums might jump from $325 to $415 monthly. Your deductible could increase from $2,500 to $3,500. Your preferred hospital might have left the network. The medication you take daily might have moved to a higher cost tier requiring prior authorization.

I know someone who auto-renewed for three years while her premium crept from $280 to $490 monthly—a $2,520 annual increase—because she couldn't be bothered to spend 45 minutes comparing options. Another plan would have saved her $1,800 yearly with better coverage.

Choosing based on premiums alone is tempting but shortsighted. You see two plans: one costs $175/month with a $6,500 deductible, another costs $375/month with a $1,500 deductible. The cheap one saves you $200 monthly, right? That's $2,400 annually!

But if you have even moderate medical needs—say, quarterly specialist visits, one ER trip, regular prescriptions—you'll blow through that $6,500 deductible and pay far more out-of-pocket than the $5,000 difference in deductibles eats into your premium savings. Suddenly the "expensive" plan actually saved you money.

Calculate total potential costs using realistic medical usage estimates. Don't assume you'll never get sick, but also don't plan for worst-case scenarios if you're generally healthy.

Author: Lauren Prescott;

Source: blaverry.com

Ignoring subsidy eligibility updates leaves free money on the table. Your income from last year determines this year's subsidies. If you got a raise and didn't report it, you might owe money back at tax time when the IRS reconciles everything. If you took a pay cut or lost income sources, you're missing subsidies you've earned.

Run the Marketplace subsidy calculator even if you didn't qualify last year. It takes 90 seconds and might reveal you're now eligible for $200+ monthly in premium assistance.

Forgetting to add new dependents happens surprisingly often with newborns. Parents assume the hospital handles insurance enrollment, or they think their baby is automatically covered for some grace period. Not true. You must actively add the child to your plan within 60 days of birth. Miss that window because you're sleep-deprived and dealing with diapers, and your baby goes uninsured until next year's open enrollment.

Skipping provider network verification creates access nightmares. Online provider directories list doctors who may have left the network months ago. Insurance company websites often show outdated information. The only reliable verification is calling the doctor's office directly and asking if they're accepting your specific plan for new appointments in the coming year.

I've seen people switch to "better" plans only to discover their rheumatologist, oncologist, or longtime primary care doctor doesn't participate. Then they're stuck for twelve months either paying out-of-network rates (often 40-50% coverage instead of 80%) or finding new doctors.

Overlooking prescription cost changes affects anyone taking regular medications. Formularies—the list of covered drugs and their cost tiers—shift annually. Your cholesterol medication that cost $15 monthly might jump to $60 because it moved from Tier 2 to Tier 3. Your insulin might require prior authorization where it didn't before, creating delays when you need refills.

Use the plan comparison tools that let you enter specific prescriptions. Most Marketplace and Medicare plan finders have drug comparison features. Spending five minutes checking your meds can prevent $500+ in surprise costs.

Open Enrollment Timeline by Coverage Type

| Coverage Category | Enrollment Dates | When Coverage Begins | Important Details |

| Federal Marketplace (HealthCare.gov) | Nov 1, 2025 through Jan 15, 2026 | Jan 1 or Feb 1, 2026 based on selection date | Applications completed by Dec 15 activate on New Year's Day; later applications start Feb 1. State exchanges may offer extended deadlines. Life event exceptions available year-round. |

| Medicare (Original + Advantage) | Oct 15 through Dec 7, 2025 | Jan 1, 2026 | Additional disenrollment option Jan 1 through Mar 31 for Advantage members switching back to Original Medicare. New eligibles turning 65 get a 7-month window spanning 3 months before birthday month through 3 months after. |

| Employer/Workplace Plans | Company-specific, usually Oct-Nov | Typically Jan 1 of new year | Exact dates vary by employer. Some organizations using fiscal years rather than calendar years may schedule enrollment in different months. New hire enrollment follows separate 30-90 day windows. |

| Medicaid | Any time throughout the year | Usually the 1st of the month following approval | No restricted enrollment period. Eligibility determined by income, household size, and state residency. Some states process applications within 24-48 hours for urgent situations. |

Frequently Asked Questions About Open Enrollment

Open enrollment gives you one concentrated opportunity each year to match your health insurance with your actual needs and financial reality. Success requires you to show up actively rather than passively accepting whatever automatically renews.

Start by marking your calendar right now with relevant dates for your coverage type. Block out two to three hours in early November for gathering paperwork and reviewing your current plan's performance. If you're shopping Marketplace plans, verify whether income fluctuations affect your subsidy amounts—a $5,000 income change can mean $100-$200+ monthly in additional subsidies or unexpected bills. For workplace coverage, actually attend those HR information sessions instead of deleting the calendar invites. Medicare beneficiaries should carefully read the Annual Notice of Change letter from current plans and invest time in the Plan Finder tools on Medicare.gov.

The financial stakes justify your time investment. Selecting an inappropriate plan can drain thousands through unnecessary premiums or inadequate coverage when you need medical care. Missing enrollment entirely might strand you without insurance for twelve months. But dedicating a few focused hours during the enrollment window protects both your health and your bank account, ensuring appropriate coverage activates before you need it.

Remember that health insurance isn't a commodity where one-size-fits-all makes sense. Your coworker's perfect plan might be completely wrong for your situation. Your unique combination of health conditions, preferred doctors, regular prescriptions, and financial constraints determines which option delivers genuine value rather than just looking cheap on paper. Take ownership of these decisions, ask questions whenever you're uncertain, and use the free resources available to make selections that serve your specific circumstances rather than just checking a box and hoping for the best.