Young family with a baby sitting at a kitchen table reviewing documents on a laptop while preparing for health insurance enrollment

Special Enrollment Period Health Insurance Guide

Content

Missed the annual enrollment window? Don't panic. Life throws curveballs—you lose your job, get married, have a baby, or move across state lines. When these major changes happen, you're not stuck waiting until next November to get coverage. That's where special enrollment periods come in, giving you a limited-time opportunity to sign up for health insurance outside the usual enrollment season. The catch? You need to know the rules, act fast, and have the right paperwork ready.

What Is a Special Enrollment Period for Health Insurance?

Think of a special enrollment period (SEP) as your insurance safety valve. While the standard enrollment season runs roughly November through mid-January annually, an SEP opens when specific life-changing events happen to you. You get a temporary window—not available to everyone, just people whose circumstances have shifted dramatically.

Why do these periods exist? Congress and state regulators recognized that forcing someone who loses coverage in April to wait seven months until November created dangerous gaps. Someone laid off in spring shouldn't face summer and fall completely uninsured, one accident or diagnosis away from bankruptcy.

When we talk about what is special enrollment period health insurance, we're really discussing two parallel systems. The federal HealthCare.gov marketplace covers most states, while fifteen states plus D.C. run their own exchanges. California calls theirs Covered California. New York operates NY State of Health. Colorado runs Connect for Health Colorado. These state marketplaces must meet federal baseline requirements but often add extra qualifying events or extend deadlines beyond what HealthCare.gov offers.

Author: Derek Whitmore;

Source: blaverry.com

The fundamental difference between regular and special enrollment? Everyone can sign up during open enrollment, no questions asked. SEPs require proof. You must show documentation that something significant happened. You can't wake up in August, decide you want insurance, and expect to enroll unless you've experienced one of the approved triggering events.

Federal and state exchanges diverge in interesting ways. While HealthCare.gov strictly enforces the standard qualifying events list, California offers continuous enrollment year-round for anyone earning under 150% of poverty level. Washington state allows monthly enrollment for those under 160% FPL. Check your state's specific rules—you might have more options than federal guidelines suggest.

Who Qualifies for Special Enrollment Period Health Insurance?

Special enrollment period health insurance eligibility hinges on life events that disrupt your coverage, change your household, or force you to relocate. Federal regulators recognize dozens of scenarios, though they cluster into several broad categories.

Life Events That Trigger Eligibility

Coverage loss tops the list of triggers. Lost your job and the insurance that came with it? You're in. Hours cut from full-time to part-time, eliminating your benefits? Qualifies. Turned 26 and aged out of your parents' plan last week? That counts too.

Even voluntary departures create eligibility. Quit your job on good terms? As long as you had employer coverage that's ending, you qualify. Retired early before Medicare kicks in at 65? You're eligible. Stopped paying premiums on your individual plan and got canceled? That technically works too, though some restrictions apply.

COBRA complicates this. When you lose employer coverage, you typically get offered COBRA continuation—expensive insurance that lets you keep your old plan temporarily. Declining COBRA doesn't disqualify you from an SEP. Many people decline COBRA precisely because they're enrolling in marketplace plans instead. But if you elect COBRA then drop it months later because it's too expensive, that COBRA termination creates a new SEP.

Household changes create immediate eligibility. Got married last month? You and your spouse can both enroll. Having a baby this week? You can add them and change plans if needed. Adopting a child or accepting foster placement? Same deal.

Divorce triggers SEPs too, particularly when one spouse carried the other on employer insurance. The newly divorced person losing coverage has 60 days to find new insurance. Even a spouse's death—tragic as it is—creates an enrollment opportunity if the deceased provided the survivor's coverage.

Author: Derek Whitmore;

Source: blaverry.com

Relocation works, but with nuances. Moving from Ohio to Texas clearly qualifies because plan options differ entirely between states. Moving from downtown Chicago to suburban Chicago? That might qualify if the new ZIP code has different insurers available. The key factor: does your new location offer different plans than your old one?

College students moving to campus usually qualify, especially if they're crossing county or state lines. Seasonal workers relocating for employment qualify. Someone released from prison qualifies. But here's where it gets tricky—moving temporarily to care for a sick relative doesn't qualify. Moving solely to access better hospitals or specialists doesn't count. The move must be a genuine residential relocation, not a temporary stay.

Immigration status changes unlock eligibility. Became a naturalized citizen last Tuesday? Gained lawful permanent resident status? Were granted asylum? All of these immigration milestones trigger a 60-day window to enroll.

Income shifts sometimes create SEPs, though this category's more limited. If your earnings drop and you become newly eligible for advance premium tax credits when you weren't before, some exchanges allow enrollment or plan changes. If you suddenly qualify for cost-sharing reductions due to income changes, similar opportunities may arise. These income-related SEPs vary significantly by state.

Marketplace or insurer errors occasionally create eligibility. Did your insurer mislead you about provider networks? Did a HealthCare.gov glitch prevent you from completing enrollment? Was your application incorrectly denied? Consumer protection rules may grant you a special enrollment opportunity, though you'll need to document the error thoroughly.

Special Enrollment Period Health Insurance Income Limits

Here's something people get confused about: most SEPs don't have income caps. Earning $200,000 annually doesn't disqualify you from enrolling during a qualifying event. Income limits control subsidy eligibility, not enrollment eligibility.

Currently, enhanced premium subsidies remain available thanks to inflation Reduction Act provisions extended through 2025. The old 400% federal poverty level cliff—where earning $1 too much meant losing all subsidies—has been eliminated temporarily. Someone earning $60,000 might still receive modest premium assistance if benchmark plans in their area are expensive enough.

Author: Derek Whitmore;

Source: blaverry.com

Certain SEPs do relate directly to income thresholds. Lost Medicaid because your earnings increased past eligibility limits? That Medicaid termination triggers a 60-day window to purchase marketplace coverage. In states that haven't expanded Medicaid, earning below 100% FPL might qualify you for a special enrollment opportunity to buy unsubsidized marketplace coverage—since you'd fall into the coverage gap.

How Does Special Enrollment Period Health Insurance Work?

Walking through enrollment during an SEP resembles the open enrollment process with one major addition: you'll need to prove why you qualify. Let's break this down into manageable steps.

First, pinpoint exactly when your qualifying event occurred. Your wedding date, baby's birthday, last day of coverage, move-in date at your new address—nail down the specific date. This determines your 60-day countdown. Get this wrong and you might miss your deadline or face documentation challenges later.

Second, head to the marketplace website. If you're in the 35 states using HealthCare.gov, start there. Live in California, New York, Massachusetts, Colorado, Connecticut, Idaho, Maine, Maryland, Minnesota, Nevada, New Jersey, New Mexico, Pennsylvania, Rhode Island, Vermont, Washington, or D.C.? Use your state exchange instead. Already have an account from previous years? Log in and update your information. First-timer? You'll create credentials and begin a fresh application.

Third, report your qualifying event during the application. The system will ask why you're enrolling outside the regular season. Select your specific trigger from the dropdown menu—lost job coverage, got married, had a baby, moved, whatever applies. Enter the exact date. Don't fudge this. The marketplace may verify details, and inaccuracies can torpedo your coverage.

Fourth, complete the full application. Report everyone in your household, even people not enrolling. Report your projected annual income from all sources. This takes anywhere from fifteen minutes if you're organized to an hour if you're gathering information as you go. The system uses these details to calculate whether you qualify for subsidies and how much assistance you'll receive.

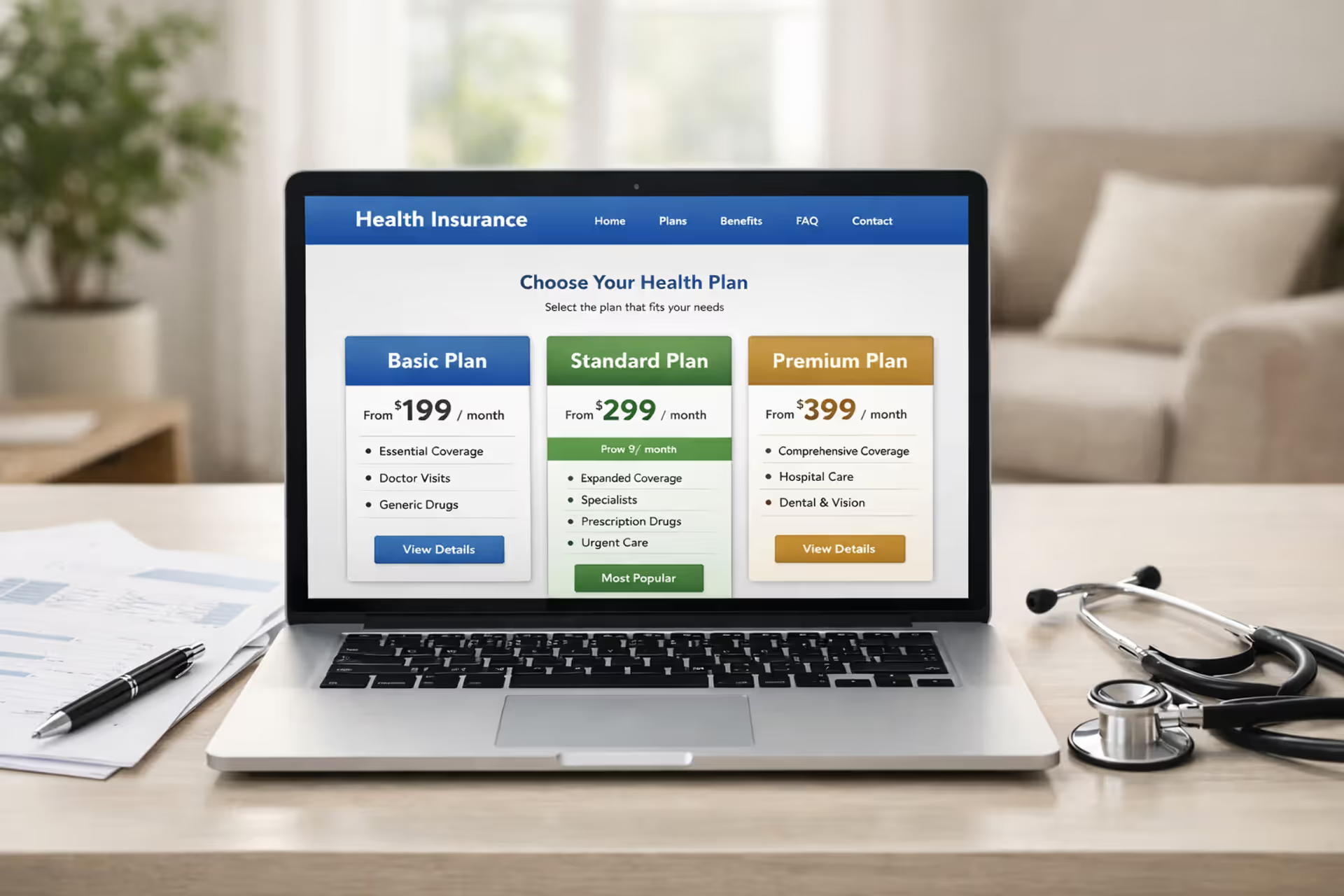

Fifth, review every plan available in your county. You'll see metal tiers—Bronze, Silver, Gold, Platinum—each with different premium and deductible tradeoffs. Bronze plans have the lowest premiums but highest deductibles. Platinum plans flip that equation. Silver plans unlock cost-sharing reductions if your income qualifies, potentially making them the best value despite higher premiums than Bronze.

Check provider directories obsessively before deciding. Does your dermatologist participate? What about your kids' pediatrician? Call doctor offices directly—online directories aren't always current. Look up whether your prescriptions are covered and at what tier. A plan that's $50 cheaper monthly but puts your insulin in a higher formulary tier could cost you thousands more annually.

Sixth, select a plan and finalize enrollment. Click through to complete the signup process. You'll receive confirmation, typically via email. Note your first premium amount and due date—coverage doesn't activate until you pay.

Seventh, submit documentation proving your qualifying event. Some marketplaces request this immediately during enrollment. Others give you 30 days post-enrollment to provide proof. Check your account regularly for document requests. Upload scans or clear photos through your marketplace account portal. Can't scan? Mail copies to the address specified in your notice. Never send originals—always keep those.

I watch people delay their applications constantly—they're comparing plans or hoping something better appears. That 60-day clock is absolute. Start your application within the first week after your qualifying event, even if you haven't decided on a plan yet. You can always change your selection before finalizing. Wait until day 59, and one technical glitch could leave you uninsured until next November

— Sarah Mitchell

Special Enrollment Period Health Insurance Timeline and Deadlines

Timing makes or breaks your SEP enrollment. The standard federal rule: 60 days from your qualifying event to submit your application and select a plan. Miss that deadline by even one day, and you're typically out of luck until the next open enrollment season.

That 60-day clock starts ticking on the qualifying event date itself—not when you receive a termination notice, not when you decide to look for coverage, not when you get around to starting an application. Coverage ended March 15th? Your deadline is May 14th. No extensions, no grace period, no do-overs.

When coverage actually begins depends on which qualifying event you experienced and when you complete enrollment:

Loss of coverage situations: Enroll by the last day of any month, and coverage typically starts the first day of the next month. Enrolled on April 28th after losing job coverage? Expect June 1st as your effective date. A handful of state exchanges allow same-month starts if you enroll by the 15th of the month—so April 12th enrollment might mean May 1st coverage begins.

Birth, adoption, or foster placement: Coverage backdates to the event date as long as you enroll within 60 days. Baby born June 3rd and you enroll June 25th? Coverage is retroactive to June 3rd, meaning any immediate NICU stays or pediatric care gets covered. This retroactive feature doesn't apply to most other qualifying events.

Marriage: Coverage generally begins the month after you enroll. Got married April 15th and enrolled April 30th? Expect June 1st coverage. Some circumstances allow retroactive coverage to the marriage date, but don't count on it—confirm with your specific marketplace.

Relocation: Similar to loss of coverage—enroll by month-end for next-month coverage. Some states offer mid-month deadlines for same-month effective dates.

State marketplace variations create a patchwork of different rules. California's year-round enrollment for households under 150% FPL means many Californians don't need SEPs at all. Massachusetts provides continuous enrollment through ConnectorCare for qualifying residents. New York extends some SEP timelines beyond 60 days. Washington and Colorado offer monthly enrollment periods for low-income residents.

Minnesota allows all American Indians and Alaska Natives to enroll year-round, SEP or not. Vermont offers a permanent open enrollment period for all residents regardless of income or circumstances—though you'll still need to report household changes as they occur.

Always verify specific deadlines with your marketplace. If you're in a state-based exchange, their rules supersede federal timelines.

Documents Needed to Enroll During a Special Enrollment Period

Gathering paperwork before you need it prevents frustrating delays. Special enrollment period health insurance documents needed vary based on your qualifying event, but marketplaces typically allow conditional enrollment, then give you 30 days to submit proof. Fail to provide acceptable documentation within that window, and they'll terminate your coverage retroactively.

If you're enrolling due to coverage loss: - Official termination notice from your insurance company or employer's HR department - COBRA election materials showing when coverage ended - Final paycheck stub indicating your last day of employment - Letter from Medicaid or CHIP stating your termination date and reason

Handwritten notes from supervisors don't cut it. The marketplace needs official letterhead, dates clearly stated, and authoritative signatures.

If marriage triggered your SEP: - State-issued marriage certificate or license (church certificates alone typically don't suffice) - Social Security numbers for both spouses - Documentation showing both individuals' prior coverage status

If you're adding a newborn, adopted child, or foster placement: - Hospital birth records (birth certificate comes later and that's fine initially) - Official adoption decree from family court - Foster care placement agreement signed by state child welfare agency

For relocation: - New lease agreement or mortgage statement with move-in date visible - Utility bill (electric, gas, water) in your name at the new address - Updated driver's license or state identification showing new address - USPS mail forwarding confirmation to the new address

One document usually isn't enough for moves. Marketplaces want to see multiple pieces of evidence proving you genuinely relocated rather than temporarily staying somewhere.

For citizenship or immigration status changes: - Certificate of Naturalization (N-550 or N-570) - Certificate of Citizenship - Permanent Resident Card (green card) - Immigration documentation showing approved asylum, refugee status, or other lawful presence

Universal documents for all SEP applicants: - Government-issued photo ID for the primary applicant - Social Security numbers for every household member enrolling - Recent pay stubs (last 2-3), W-2 forms from the prior year, or previous year's tax return for income verification - Details about any current or recently ended health coverage

Photo quality matters enormously. Blurry phone photos where the text is barely legible will get rejected. Use a scanner if possible. If photographing documents, use good lighting, avoid shadows, and make sure every word is crisp and readable. Poor image quality is the number one reason marketplaces reject documentation and request resubmission—eating into your 30-day window.

Common Mistakes to Avoid When Using a Special Enrollment Period

Author: Derek Whitmore;

Source: blaverry.com

Blowing past the 60-day deadline destroys more SEP opportunities than anything else. People assume they have plenty of time, get busy comparing every available plan, or procrastinate because choosing insurance feels overwhelming. Set a phone reminder for day 45 after your qualifying event. Better yet, start your application within the first week while the event is fresh and documentation is readily available.

Submitting inadequate documentation ranks second in application-killers. Your former employer's verbal confirmation that you lost coverage means nothing without paperwork. A screenshot of an informal email won't work. Marketplaces need official documentation—letterhead, signatures, dates, formal language. When in doubt, request official notices from whoever's providing your proof. HR departments, insurance companies, and government agencies can reissue formal letters if you explain you need them for marketplace enrollment.

Rushing through plan selection creates buyer's remorse lasting an entire year. Yes, you're under time pressure during an SEP. But enrolling in the first plan you see, only to discover later that none of your doctors participate or your medications cost three times what you expected, leaves you stuck. Block out two hours minimum to compare at least three plans. Create a spreadsheet if that helps. Check provider directories by calling offices directly. Look up prescription costs using the marketplace's formulary tool.

Presuming qualification without verification leads to denied applications and wasted time. Got a new job offering better insurance than your current marketplace plan? That's great—but switching to employer coverage isn't a qualifying event for marketplace enrollment (though losing employer coverage later would be). Want to drop your marketplace plan because you don't like it? Not a qualifying event. Make certain your specific situation matches an approved trigger before starting an application.

Forgetting about the first premium payment means your enrollment vaporizes. Selecting a plan completes step one. Actually activating that coverage requires payment. Most insurers want the first premium within 14 days of the effective date. Miss that payment and your coverage never begins, even though you technically "enrolled." The marketplace won't remind you—tracking premium deadlines is your responsibility.

Applying through the wrong marketplace creates coverage headaches. Your residence determines which marketplace to use, not your work location. Live in Illinois but work in Missouri? Use Illinois's marketplace. Attending college in North Carolina but your permanent address is New Jersey? Use New Jersey's exchange. File taxes in the wrong state and live in another? Your residential address controls marketplace choice.

Qualifying Events and Required Documentation

| Qualifying Event | Enrollment Window | Documentation Required | When Coverage Begins |

| Job-based coverage ends | 60 days after final day of coverage | HR termination letter, COBRA notice | First of following month after enrollment |

| Getting married | 60 days after wedding date | Marriage certificate, prior coverage proof | First of month after signing up |

| Baby born or child adopted | 60 days after birth/adoption | Hospital records, birth certificate, adoption papers | Retroactive to birth/adoption date |

| Permanent residential move | 60 days after establishing new residence | Lease, utility bills, updated ID showing new address | First of next month after enrollment |

| Medicaid or CHIP ends | 60 days after termination | State termination letter with end date | First of month after enrolling |

| Gaining citizenship | 60 days after status granted | Naturalization certificate, immigration documents | First of following month |

Frequently Asked Questions About Special Enrollment Periods

Life doesn't coordinate with insurance enrollment calendars. Special enrollment periods recognize that losing a job, getting married, having a baby, or moving across the country shouldn't leave you uninsured for months waiting for the next open enrollment window.

The system works—but only when you understand the rules and act decisively. That 60-day window offers breathing room, not an invitation to procrastinate. Documentation requirements aren't bureaucratic harassment; they prevent people from gaming the system by enrolling only after getting sick. Moving quickly while gathering proof efficiently separates people who successfully enroll from those who miss their chance.

Uncertainty about whether your situation qualifies? Contact a certified navigator or licensed insurance broker. These professionals offer free help and can clarify eligibility questions before you waste time on an application. The HealthCare.gov call center (1-800-318-2596) also answers questions, though hold times vary wildly depending on the day and season.

Insurance matters because medical bills destroy family finances faster than almost any other expense. A special enrollment period gives you an opportunity to restore protection after circumstances shift. Don't let confusion, delays, or incomplete information prevent you from using this safety net when you need it most.