Person canceling health insurance plan on laptop with documents and calculator on desk

How to Cancel Marketplace Insurance

Content

Getting out of your Marketplace health plan takes more work than you'd expect. You can't just stop paying and walk away. There's paperwork to file, deadlines to hit, and money issues to sort out—especially if you've been getting help paying your premiums. Maybe you just landed a job with benefits, or you're moving across state lines, or your family situation changed. Whatever's pushing you to cancel, doing it wrong could leave you scrambling to pay medical bills or facing a surprise tax bill next April.

When You Can Cancel Your Marketplace Health Plan

Here's the thing: you can't bail on your Marketplace plan whenever the mood strikes. The government built in specific windows when changes are allowed.

The main opportunity comes during the yearly open enrollment window, which kicks off on November 1st and wraps up around mid-January (January 15th in most years). During these weeks, you've got free rein—dump your current coverage, pick a different plan, or go without insurance entirely. Nobody asks why. If you make your move before mid-December, your coverage typically stops on December 31st. Cancel in early January, and you're usually covered through January 31st.

Outside that window? You need what the government calls a qualifying life event, or QLE for short. Think major life disruptions: tying the knot, splitting up, welcoming a baby, saying goodbye to your existing coverage, relocating to a new zip code, or picking up insurance through work. The feds recognize these situations as legitimate reasons to shake up your coverage mid-year.

Here's where timing gets critical. Qualifying events give you a 60-day window to act. Get married March 20th? You've got until roughly May 19th to report it and request changes. Miss that window, and you're riding out your current plan until the next November, whether you like it or not.

One trap catches people constantly: thinking that ignoring premium bills counts as canceling. It doesn't. Your insurer will eventually cut you off, sure—but not before creating a mess. You'll rack up debt during a grace period, complicate your tax filing, and potentially blacklist yourself from future Marketplace enrollment.

Steps to Cancel Marketplace Insurance

The cancellation mechanics depend on where you signed up. The federal HealthCare.gov system works differently than state-run exchanges like Covered California or NY State of Health. Either way, you've got to pull the trigger yourself—nothing happens automatically just because you landed new coverage.

Canceling Through HealthCare.gov

Pull up HealthCare.gov and sign in with whatever username and password you created during enrollment. Hunt down the section labeled "My Applications & Coverage"—your active plan lives there. You'll spot options like "End coverage" or "Report a life change" next to your plan details.

If something major happened (new job, new baby, new address), click "Report a life change" first. The site walks you through questions about what changed and when. It'll ask for your new coverage start date if you're switching to employer insurance, or specifics about your wedding date, moving day, or whatever triggered the change. Your answers here determine when your Marketplace coverage actually stops and how your tax credits get calculated.

For the actual cancellation step, have some information ready: when your new coverage kicks in, why you're leaving, and paperwork proving it (like a benefits letter from your new employer showing coverage details, or your new lease agreement). The system spits out a confirmation number once you submit—screenshot that sucker. An email confirmation should land in your inbox within a day or so.

Your end date isn't random. Say your employer coverage starts May 1st. Your Marketplace plan would typically end April 30th. Submit your cancellation at least two weeks before your target end date—processing isn't instant, and you don't want overlap or gaps.

Canceling Through Your State Exchange

Fourteen states plus DC run their own insurance websites instead of using the federal system. Living in California, New York, Massachusetts, Colorado, or another state-exchange territory? You'll work through their platform, not HealthCare.gov.

The basic flow matches the federal site: log in, report what changed, upload your proof, confirm your end date. But the details vary by state. California's Covered California often wants to see documentation of your new coverage before approving anything. New York's system lets you call and cancel over the phone, which actually moves faster if you've got your paperwork lined up.

State exchanges generally answer their phones better than the federal system, especially during busy seasons. Stuck on something? A 20-minute call to your state exchange usually beats an hour wrestling with HealthCare.gov's phone maze.

Author: Derek Whitmore;

Source: blaverry.com

What Happens After You Cancel

Your insurance doesn't evaporate the second you hit "submit." The timeline and money pieces need attention, or you'll get hit with surprises.

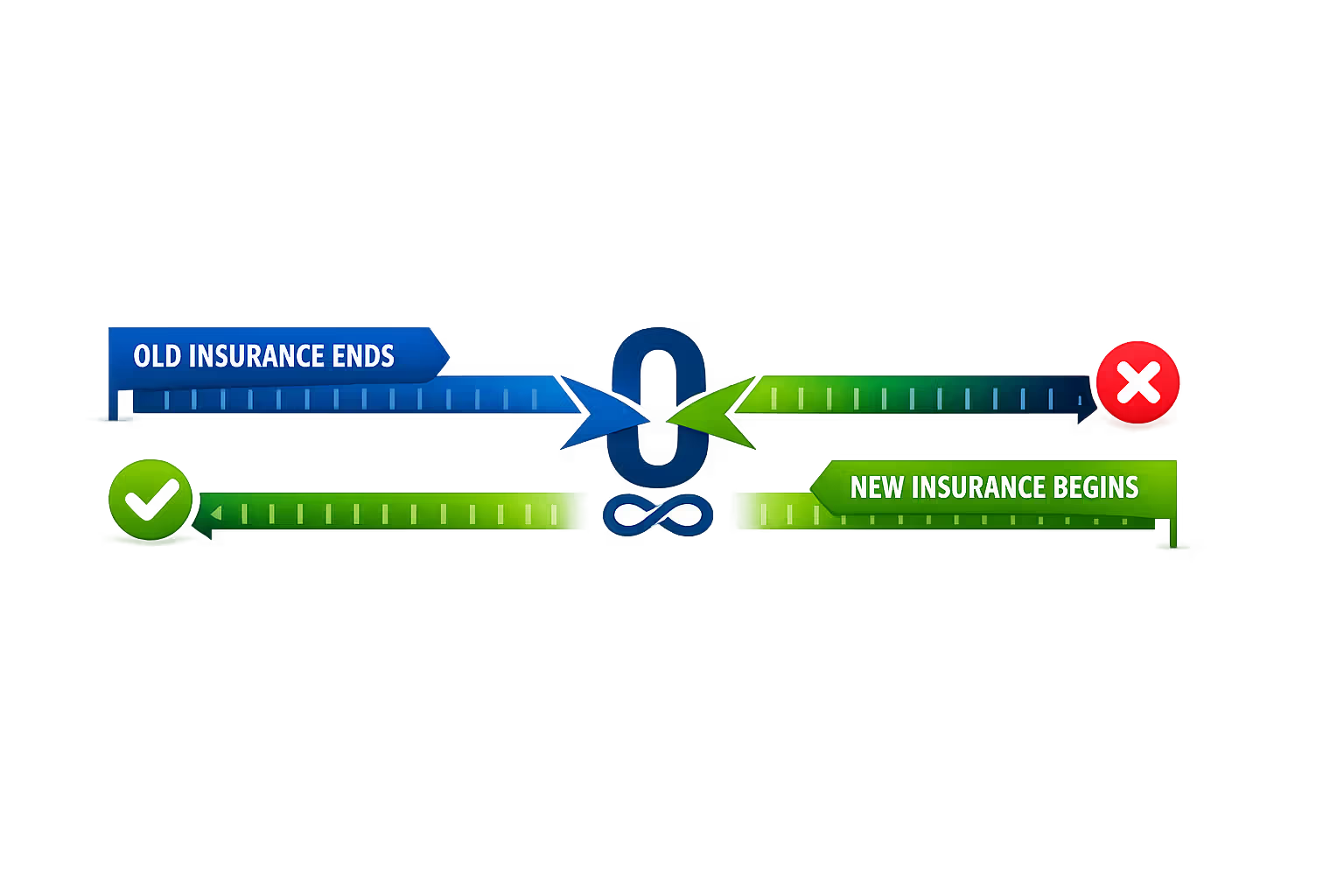

Coverage hangs around until one of these dates hits: the last day of the month when your qualifying event happened, the day right before your new insurance starts, or month-end if you're canceling during open enrollment without a replacement plan lined up. Until that date arrives, you're still insured—and still on the hook for premiums.

Premium payments get messy here. Already paid for the month your coverage ends mid-month? Most insurers keep it. You paid for 30 days, you get 30 days, even if your employer insurance kicks in on the 15th. Flip side: haven't paid for the month you're ending coverage? You still owe it. Skip that final payment, and you're looking at collections calls and roadblocks if you ever need Marketplace coverage again.

Tax credit reconciliation is where people get burned financially. Been getting advance premium tax credits—those monthly discounts that lowered your payments? The IRS double-checks whether you actually qualified for the full amount based on what you really earned all year. Canceling in July doesn't erase that reckoning. You settle up when filing taxes, period.

Income limits matter here: if your earnings jumped significantly before you canceled (maybe that new job pays way better), you could owe back some or all of those subsidies come tax time. Smart move? Report income changes to the Marketplace before canceling. They'll adjust your subsidy going forward, softening the tax-season blow. The Marketplace uses something called modified adjusted gross income—that's your wages, self-employment money, Social Security benefits, investment earnings, all rolled together.

Author: Derek Whitmore;

Source: blaverry.com

COBRA doesn't enter the picture with Marketplace plans—that's strictly for employer coverage. But if you're canceling without immediate replacement coverage, you're going bare. Even one day uninsured can mess with future subsidy eligibility and leaves you financially naked if you need emergency care.

Requirements and Eligibility for Canceling Mid-Year

Not every life change unlocks mid-year cancellation. The Marketplace recognizes specific events that create real coverage needs or make your current plan a bad fit.

| Life Change | Coverage End Date | Proof You'll Need | Report By |

| Started employer coverage | Previous day before work insurance begins | Benefits letter or offer paperwork showing start date and coverage details | Within 60 days of new coverage starting |

| Relocated to different state or county | Final day of moving month | New lease, recent utility bill, updated driver's license | Within 60 days of relocation |

| Marriage | Month-end when wedding occurred | Official marriage certificate | Within 60 days of ceremony |

| Birth or adoption | Baby's arrival or placement day | Birth certificate, adoption decree | Within 60 days of event |

| Previous coverage ended | Same day old insurance stopped | COBRA paperwork or termination notice from former carrier | Within 60 days of losing coverage |

| Medicaid approval | Eligibility determination date | State Medicaid approval documentation | Within 60 days of qualifying |

That 60-day reporting deadline isn't flexible. Wedding on March 15th means you've got until May 14th to report and request cancellation. Blow past that date, and you're locked in until December 31st.

Proof matters. A casual text from your new boss saying "benefits start next month" won't fly—you need official paperwork. Scan and upload documents instead of mailing them; it processes faster and you've got digital proof you submitted everything.

Income limits don't directly block cancellation, but they determine whether you're writing a check to the IRS later. Got subsidies based on estimating $35,000 in earnings but actually pulled in $55,000? You're paying some credits back at tax time.

Common Mistakes When Canceling Marketplace Coverage

The process looks straightforward until you make one of these errors that blow up your coverage or finances.

Canceling before new coverage starts leaves you dangerously exposed. People get excited about accepting a job with benefits and immediately dump their Marketplace plan. Bad move. That employer coverage might not activate for 30, 60, even 90 days. You're uninsured that whole time. Wait for a confirmed start date on your new insurance, then time your Marketplace exit for the day before.

Skipping the income update before canceling sets up tax-time pain. Income jumped because of that new job? Update your Marketplace application before pulling the plug. The system recalculates your subsidy eligibility and adjusts credits for the months you were enrolled. Skip this step, and you're looking at massive repayment when filing your return.

Forgetting that final month's premium payment trashes your Marketplace account. Even though you're leaving, that unpaid bill goes to collections and blocks your account. Need Marketplace coverage again someday? You'll clear that debt before enrolling.

Assuming automatic cancellation when new coverage begins costs people serious money. Your Marketplace plan keeps running until you explicitly kill it, even after employer coverage starts. You'll pay premiums for both simultaneously, and the Marketplace plan stays primary (creating nightmare claim situations) until you formally end it.

Not grabbing written cancellation confirmation leaves you vulnerable if processing fails. Always download or screenshot the confirmation page, save the email. If cancellation doesn't process and bills show up months later, that confirmation proves you followed proper procedure.

Author: Derek Whitmore;

Source: blaverry.com

Alternatives to Canceling Your Marketplace Plan

Before pulling the plug, consider whether tweaking your existing coverage serves you better.

Plan-switching during open enrollment lets you adjust coverage level without the full cancel-and-reenroll dance. Current plan too pricey? Drop to a bronze tier with cheaper premiums. Developed health issues needing better coverage? Upgrading to gold or platinum might cost less than out-of-pocket spending with your current bronze plan.

Income updates to adjust subsidies work when your money situation shifts but you want to keep Marketplace coverage. Income took a hit? Report it, subsidy increases, monthly premium drops. Beats canceling and risking a coverage gap.

Medicaid transitions happen automatically in expansion states when income falls below the threshold (138% of federal poverty level in states that expanded). The Marketplace flags your Medicaid eligibility and handles the transfer. Your Marketplace plan ends when Medicaid starts, zero gap.

Employer coverage coordination doesn't always mean dumping your Marketplace plan immediately. Some folks keep Marketplace coverage for spouses or kids while moving themselves to employer insurance. You can modify your application to remove yourself while maintaining dependent coverage, often cheaper than adding family to your work plan.

Worried about cost? Check whether you qualify for cost-sharing reductions (CSRs) you're not currently getting. These subsidies slash deductibles and out-of-pocket maximums but only work on silver plans. Switching from bronze to silver during open enrollment might deliver better effective coverage for similar net cost.

Expert Insight:

I watch people make the same mistake constantly—canceling Marketplace coverage before new insurance actually activates.They're thrilled about new job benefits and rush to cancel, missing that employer coverage won't begin for another 30 days. That gap becomes financially catastrophic if emergency care hits, plus it tangles subsidy reconciliation at tax time. Always overlap coverage by at least one day—end Marketplace coverage the day before new insurance starts, never sooner

— Jennifer Martinez

Frequently Asked Questions About Canceling Marketplace Insurance

Canceling Marketplace insurance demands more planning than most expect. The mechanics aren't complicated, but timing rules, documentation needs, and tax implications require careful attention. Missed deadlines or skipped steps can strand you uninsured, owing money, or stuck in an unsuitable plan.

First step: confirm you've got a qualifying life event if canceling mid-year. Gather documentation before starting the online process—having your new coverage start date, qualifying event proof, and final premium payment confirmation streamlines cancellation. Report income changes to the Marketplace before canceling for an accurate picture of your tax credit situation.

Critical point: never let coverage lapse. The gap between plans should be zero days. Time your Marketplace cancellation to end the day before new coverage begins, confirm both dates in writing. Your future self will appreciate avoiding the coverage gap that transforms a routine doctor visit into financial disaster.

The Marketplace system provides accessible health coverage, and the cancellation process—despite rules and requirements—offers flexibility for adapting insurance as life changes. Understanding these procedures puts you in control of coverage transitions rather than leaving you vulnerable to automatic processes and unexpected bills.