Person holding smartphone browsing health insurance marketplace website with plan options on screen, documents and glasses on table in cozy home setting

Is Obamacare Still Available in 2026

Content

The short answer? Absolutely. Despite what you might've heard in political debates, the Affordable Care Act isn't going anywhere. In fact, more Americans enrolled during the last signup period than ever before—21.3 million people chose marketplace plans. That's not a program on life support; that's a program hitting its stride.

Since President Obama signed the legislation in 2010, the ACA has weathered Supreme Court battles, congressional repeal attempts, and constant political pressure. Yet here we are in 2026, and the marketplaces are processing applications, insurers are competing for customers, and subsidies are helping families afford premiums that would otherwise break their budgets.

What's changed? Plenty. The financial assistance got better—no more subsidy cliff at 400% of poverty level. Enrollment windows expanded in some states. The application process got simpler. If you're self-employed, stuck in a job without benefits, or retired before Medicare kicks in, these marketplaces offer real solutions.

What Is Obamacare and How Does It Work Today

Think of the Affordable Care Act as a regulated shopping platform for health insurance. Instead of calling dozens of insurance companies or working with multiple agents, you log into HealthCare.gov (or your state's version) and see every available plan side-by-side.

The federal government runs the marketplace for 33 states. The other 18 states built their own systems—California's Covered California, New York's State of Health, Maryland Health Connection, and so on. Either way, the basic concept stays the same: standardized plan tiers that let you compare apples to apples.

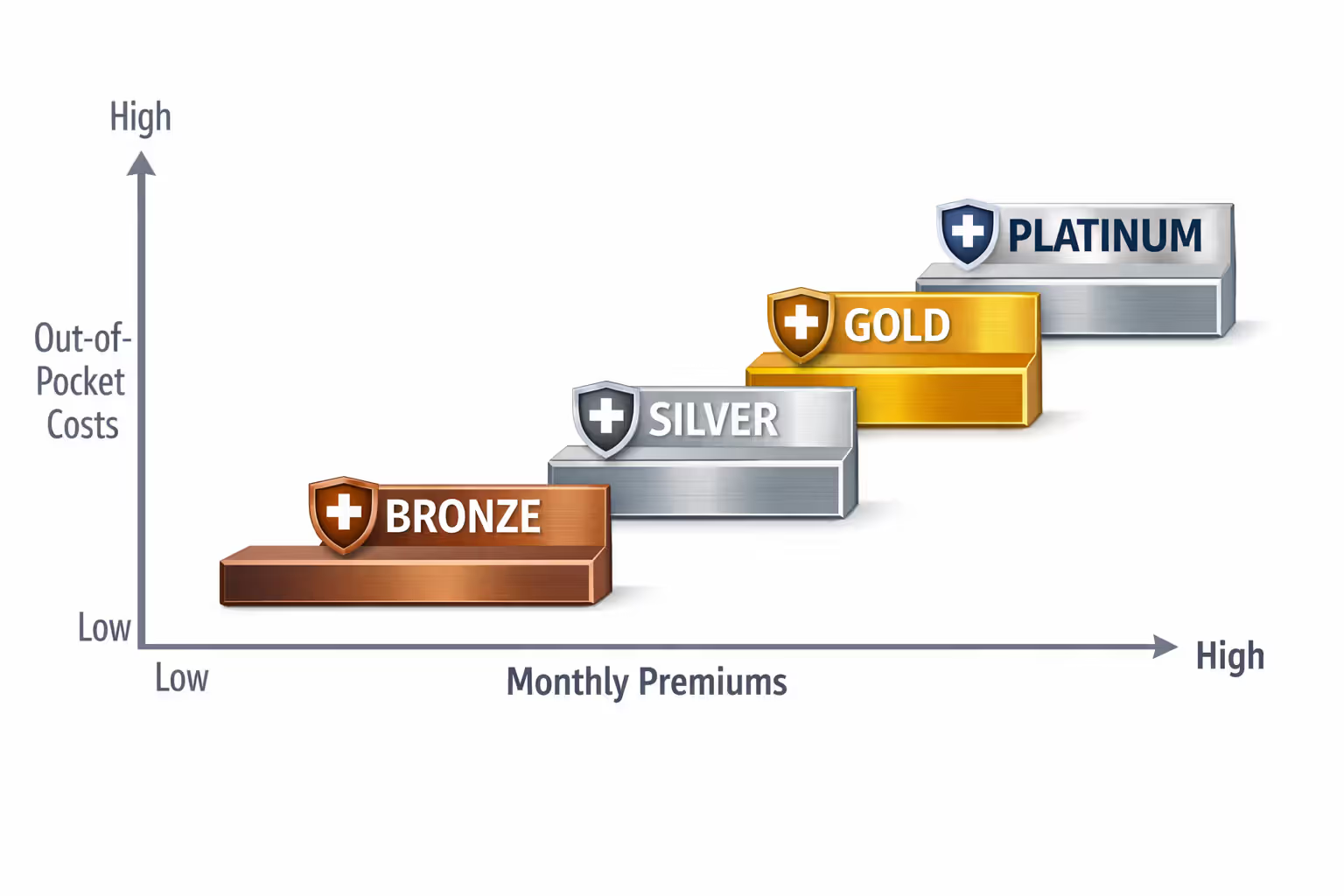

Plans come in metal tiers. Bronze plans charge the lowest monthly premiums but make you pay more when you actually use healthcare. Silver plans sit in the middle and unlock special cost-sharing discounts for lower-income households. Gold and Platinum plans cost more upfront but cover a bigger chunk of your medical bills. Every plan, regardless of tier, must include:

- Doctor visits and outpatient care

- Emergency room services

- Hospital stays and surgeries

- Pregnancy care and childbirth services

- Mental health treatment and addiction counseling

- Prescription medications

- Physical therapy and rehabilitation

- Lab work and diagnostic tests

- Preventive care at no cost to you

- Kids' dental and vision coverage

Here's what makes the system work: insurance companies can't reject you because you have diabetes, survived cancer, or take medications for depression. They can't charge you extra for pre-existing conditions. They can't drop your coverage when you get sick. Age affects pricing, but health status doesn't.

Author: Melissa Grant;

Source: blaverry.com

The subsidy structure changed dramatically in 2021. Before, if you earned one dollar over 400% of the federal poverty level, your financial help vanished completely. Now? You can earn well above that threshold and still qualify for subsidies if premiums would eat up more than 8.5% of your income. This adjustment brought affordable coverage to middle-class families who'd been priced out.

The marketplace operates on a schedule. You can't just show up whenever you feel like getting insurance. Open enrollment runs for about 75 days starting November 1st. Outside that window, you need a qualifying life event—lost your job, got married, had a baby, moved states—to unlock a special 60-day enrollment period.

Obamacare Eligibility Requirements

You need to check three basic boxes: live in the United States legally, lack access to other qualifying coverage, and fall within income ranges that make marketplace plans your best option.

Citizenship matters. U.S. citizens qualify automatically. Lawful permanent residents (green card holders) qualify. Refugees and asylees qualify. Various visa holders qualify. Undocumented immigrants can't buy marketplace coverage even if they want to pay full price without subsidies—though their U.S.-citizen children can enroll.

You can't be locked up when you apply. You can't already have Medicare (though the month you turn 65 and lose marketplace coverage counts as a qualifying event for Medicare). If your employer offers health insurance that meets federal standards for affordability and coverage quality, you won't get subsidies—but here's the catch. "Affordable" only looks at what YOU pay for your own coverage, not what it costs to add your spouse and kids. If family coverage through work costs a fortune, your family members might qualify for subsidized marketplace plans while you stick with employer insurance.

Income Limits and Subsidy Qualifications

Financial assistance kicks in when your household brings home between 100% and roughly 400% of the federal poverty level, with help extending higher if local plan costs are steep. The poverty level changes every year, so these ranges shift annually.

For 2026, a single person earning $15,060 to about $60,000 typically qualifies for some level of premium reduction. A family of four making between $31,200 and $120,000 usually gets help, though exact cutoffs depend on insurance prices in your county.

Cost-sharing reductions represent a separate benefit available only below 250% of poverty. These hidden discounts reduce your deductibles, copays, and coinsurance—but only if you pick a Silver plan. An enhanced Silver plan with cost-sharing reductions often covers more of your bills than a Gold plan, despite lower premiums.

Here's what poverty-level percentages translate to in actual dollars:

| Family Size | 100% Poverty | 250% Poverty | 400% Poverty | Monthly Subsidy (Estimate) |

| 1 person | $15,060 | $37,650 | $60,240 | $50-$400 |

| 2 people | $20,440 | $51,100 | $81,760 | $100-$600 |

| 3 people | $25,820 | $64,550 | $103,280 | $150-$800 |

| 4 people | $31,200 | $78,000 | $124,800 | $200-$1,000 |

| 5 people | $36,580 | $91,450 | $146,320 | $250-$1,200 |

Your actual subsidy depends on three factors: local insurance costs, your age (older people get bigger subsidies because age-rated premiums run higher), and household income. These estimates give you ballpark figures, not precise amounts.

Who Qualifies for Coverage

Freelancers and gig workers qualify. Uber drivers, graphic designers, consultants—anyone earning 1099 income can enroll. Early retirees who left work at 62 but don't get Medicare until 65 fit perfectly. Part-time employees whose employers don't offer benefits? Absolutely qualified. Small business employees? If your company doesn't provide health insurance, the marketplace fills that gap.

Students represent another major group. If you're not on your parents' plan (you can stay there until 26) and your college doesn't require insurance or offers expensive coverage, marketplace plans might cost less and cover more.

The employment affordability test creates weird situations. Your employer might offer you insurance for $150/month that qualifies as "affordable" under federal rules. But adding your spouse costs another $400 and each kid adds $250. That family coverage totals $1,050/month—definitely not affordable. Your spouse and children might qualify for subsidized marketplace coverage even though you're stuck with employer insurance.

Lawfully present immigrants face a five-year waiting period for Medicaid in most states, but they can buy marketplace coverage immediately. This creates a coverage gap where someone earning 80% of the poverty level can't get Medicaid yet qualifies for heavily subsidized marketplace plans.

Author: Melissa Grant;

Source: blaverry.com

Documents Needed to Apply for Obamacare

Start gathering paperwork before you begin your application. Having documents ready prevents delays and reduces errors that could mess up your subsidy calculation.

Income documentation varies wildly based on how you earn money. If you receive a regular paycheck, grab your two most recent pay stubs showing year-to-date earnings. Self-employed? You'll need a profit-and-loss statement, your business accounting ledger, or last year's Schedule C from your tax return. Social Security recipients need their benefits letter showing monthly payment amounts. Unemployment insurance? Print your benefits determination notice.

Here's what trips people up: if your income changed significantly from last year, old tax returns don't help much. Lost your job in August? Your W-2 from last year shows income you're not earning anymore. The marketplace wants to know your current situation, not ancient history. Document your present circumstances—recent pay stubs, current business income, termination letters, new job offer letters.

Identity verification requires Social Security numbers for anyone applying for coverage. Your kids need them. Your spouse needs one. But—and this matters—household members you're NOT enrolling don't need to provide Social Security numbers. If you're a U.S. citizen married to an undocumented immigrant, you can enroll yourself and your kids without providing your spouse's Social Security information.

Household information includes everyone you'll claim on your tax return, whether they're applying for coverage or not. This affects your household size for subsidy calculations. Married couples filing separately face special rules—you'll usually need to include your spouse's income in the calculation even though you file separately. Exceptions exist for domestic violence situations or spousal abandonment, but you'll need documentation proving those circumstances.

Special enrollment applicants need extra proof. Getting married? Submit your marriage certificate. Had a baby? Birth certificate required. Lost your employer coverage? You need a termination letter from your previous insurer showing the coverage end date. Moved to a new state? Utility bills, lease agreements, or driver's license with new address work.

Obamacare Enrollment Timeline and Deadlines

Open enrollment starts November 1st and runs through January 15th in most states—that's your 75-day window to get covered. Plans purchased by December 15th start January 1st. Buy between December 16th and January 15th, and coverage begins February 1st.

Miss that window? You're stuck until next year unless you qualify for special enrollment. These 60-day windows open when specific life changes upend your insurance situation.

What triggers special enrollment? Losing previous coverage (employer insurance ends, COBRA expires, aged off parents' plan). Marriage or divorce—both change your household and create new coverage options. Having a baby or adopting a child. Moving to a new coverage area (different county or state, not just across town in the same city). Gaining citizenship or lawful immigration status. Getting released from incarceration.

Not every life change counts. Turning 30 doesn't trigger special enrollment. Getting a raise doesn't. Breaking up with a boyfriend or girlfriend doesn't (marriage and divorce count, but not informal relationships). Your car getting totaled doesn't. Deciding you don't like your current plan doesn't.

State marketplaces sometimes offer longer enrollment windows. California's open enrollment extends into late January. New Jersey and Colorado give consumers extra weeks. Some states recognize additional qualifying events beyond federal requirements. Massachusetts lets certain income groups enroll year-round.

Timing matters for special enrollment. You typically have 60 days before or after the qualifying event to enroll. Lost your coverage? You can actually backdate marketplace coverage to the day after your old plan ended, eliminating gaps. Got married? Coverage starts the first day of the following month. Had a baby? Same deal—first of the next month.

Documentation deadlines are strict. The marketplace gives you 30-60 days to upload proof of your qualifying event. Miss that deadline and they'll cancel your coverage retroactively, sticking you with full-price bills for any medical care you received.

Author: Melissa Grant;

Source: blaverry.com

How to Apply for Obamacare Coverage

Head to HealthCare.gov if you live in one of the 33 states using the federal platform. Residents of the other 18 states need their state's marketplace website—Google "

health insurance marketplace" to find it.Create an account with an email address and password. Start a new application. You'll answer questions about everyone in your household, your income sources, whether anyone has coverage offers from employers, citizenship status, and current insurance situation.

The system crunches your numbers and spits out an estimated subsidy amount. Then it shows you every available plan in your county, with premiums adjusted for your tax credit. You can filter by premium cost, deductible amount, whether specific doctors participate, or whether particular hospitals are in-network.

Comparing plans requires looking beyond the monthly premium. A Bronze plan might charge $75/month with an $8,000 deductible. A Silver plan costs $180/month but carries a $2,000 deductible. Which one's cheaper? Depends on whether you actually use healthcare. Need regular medications, physical therapy, or specialist visits? That Silver plan saves you thousands. Healthy and just want catastrophic protection? Bronze might work.

Check your prescriptions against each plan's formulary. Insurance companies negotiate different prices with drug manufacturers, so the exact same medication might cost $10 on one plan and $150 on another. Log into the marketplace tool that checks drug coverage—you enter your medications and it shows costs under each plan.

Verify your doctors participate before selecting a plan. Online provider directories are notoriously inaccurate. Call your doctor's office directly and ask: "Do you accept

for 2026?" Get a name and date from whoever answers. Provider networks change yearly, so your doctor participating in 2025 doesn't guarantee 2026 participation.Federal marketplace applications get processed through HealthCare.gov serving residents of Alabama, Alaska, Arizona, Arkansas, Delaware, Florida, Georgia, Hawaii, Illinois, Indiana, Iowa, Kansas, Louisiana, Maine, Michigan, Mississippi, Missouri, Montana, Nebraska, New Hampshire, North Carolina, North Dakota, Ohio, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, West Virginia, Wisconsin, and Wyoming.

State-run marketplaces operate in California, Colorado, Connecticut, Idaho, Kentucky, Maryland, Massachusetts, Minnesota, Nevada, New Jersey, New Mexico, New York, Oregon, Pennsylvania, Rhode Island, Vermont, Washington, and the District of Columbia.

Getting help costs nothing. Certified navigators work in communities nationwide providing free, in-person enrollment assistance. They can't steer you toward particular plans, but they'll explain options and help complete applications. Insurance brokers also help for free—insurance companies pay them commissions, not consumers. The marketplace call center (1-800-318-2596) offers phone support in over 150 languages.

Don't assume you must finish the application in one session. You can save your progress, close the browser, and come back tomorrow. The system holds your information for 60 days. This matters when you're tracking down documents or need time to compare plans carefully.

Common Obamacare Mistakes to Avoid

Missing deadlines causes more coverage gaps than any other error. Set phone reminders for December 15th if you want January 1st coverage. Open enrollment ends January 15th—waiting until January 20th means no coverage until special enrollment or next year's open enrollment.

Auto-renewal sounds convenient but creates problems. Your current plan might increase premiums 30% while a competitor's similar plan stays cheap. Your doctors might leave the network. Better plans might become available. Letting coverage auto-renew without shopping means potentially overpaying or losing access to your providers.

Income estimation errors haunt people at tax time. Overestimate income? You'll pay higher premiums all year, then get a refund when filing taxes. Underestimate income? You'll receive excess subsidies and owe repayment in April. Base your estimate on realistic projections. Self-employed with unpredictable income? Estimate conservatively and report changes quarterly to adjust your subsidy.

Plan selection based purely on premium costs backfires when you need healthcare. That $50/month Bronze plan with an $8,000 deductible costs far more than a $180/month Silver plan with a $1,500 deductible if you actually visit doctors or fill prescriptions. Run the math: multiply monthly premium by 12, add your likely deductible and copay costs, then compare total annual spending across plans.

Medication coverage trips up chronic disease patients. Each plan maintains a formulary listing covered drugs and their tier pricing. Your diabetes medication might be Tier 1 ($10 copay) on one plan and Tier 4 ($150 copay) on another. Don't assume all plans cover all drugs equally.

Network confusion leads to surprise bills and denied claims. HMO plans require you to stay in-network for everything except emergencies—use an out-of-network doctor and you'll pay full price. PPO plans cover out-of-network care but charge higher deductibles and coinsurance. EPO plans fall somewhere between. Before selecting a plan, confirm your specialists participate and check which hospitals are in-network. Going to an in-network hospital doesn't guarantee all doctors treating you are in-network—anesthesiologists, radiologists, and consulting physicians might be out-of-network even in network facilities.

Failing to report household changes costs money. Income jumps 40% after a promotion? Report it within 30 days to reduce your subsidy and avoid owing thousands at tax time. Income drops after a layoff? Report immediately to increase your subsidy and lower current premiums. Adding a baby to your household changes your poverty level calculation—report the birth to adjust subsidies appropriately.

The marketplace has proven remarkably resilient and keeps providing essential coverage to working families, self-employed individuals, and early retirees.Enhanced subsidies have made quality coverage affordable for many middle-income families who previously couldn't swing marketplace premiums

— Jennifer Martinez

FAQ About Obamacare Availability

The Affordable Care Act isn't going away. Political debates rage, but the program's infrastructure is solid, enrollment keeps growing, and subsidies make coverage affordable for more families than ever before. Whether you're self-employed, between jobs, or working for a company that doesn't offer benefits, marketplace plans provide legitimate coverage options.

Success with marketplace coverage depends on understanding eligibility rules, gathering the right documents, respecting enrollment deadlines, and comparing plans beyond just monthly premiums. Look at deductibles, check whether your doctors participate, verify your medications are covered, and calculate your likely total annual costs across different metal tiers.

If you're exploring marketplace coverage for the first time or reconsidering options during the next open enrollment, don't let misconceptions about the program's status or eligibility requirements stop you from checking available plans. Visit HealthCare.gov or your state marketplace to see actual prices and subsidy amounts in your area. You might discover coverage that's more affordable than you expected and better than what you currently have.