Person standing at a crossroads choosing between a government building representing Medicaid and a laptop screen showing health insurance plan options representing the ACA Marketplace

Is Obamacare the Same as Medicaid

Content

Every year during open enrollment, millions of Americans face the same confusing question: "Am I signing up for Obamacare or Medicaid?" You've probably heard people say "I'm on Obamacare" when they actually mean Medicaid, or vice versa. This mix-up isn't just annoying—it can derail your entire enrollment if you don't know which program actually covers you.

Here's the thing: these aren't interchangeable terms, even though they're deeply connected. Getting this wrong might mean you miss critical deadlines, apply through the wrong channels, or lose out on coverage you're entitled to. Let's clear up what each one actually is and how they work together.

What Is Obamacare and How Does It Relate to Medicaid?

Most people call it Obamacare, but its official name is the Affordable Care Act—a massive healthcare law that President Obama signed back in March 2010. Now here's what trips people up: the ACA isn't actually an insurance plan you can enroll in. You can't call an insurance company and say "I'd like one Obamacare, please."

Instead, the ACA rewrote the rules for how Americans get health coverage. Picture it as renovating a house versus the house itself. The law created those online Health Insurance Marketplaces (you know, Healthcare.gov) where people shop for private coverage. It also dramatically changed who could get Medicaid.

Medicaid has been around since Lyndon Johnson signed it into law in 1965—decades before anyone heard of Obamacare. Back then, it was designed to help low-income kids, pregnant women, seniors, and disabled individuals get medical care. For most of its history, a healthy adult without kids couldn't get Medicaid coverage no matter how broke they were.

When the ACA passed, it fundamentally altered Medicaid's eligibility rulebook in participating states. Suddenly, states could cover pretty much any adult earning below a certain income threshold—no need to be pregnant, disabled, or raising children. The expansion opened the door to millions who'd been locked out before.

So when someone mentions they have "Obamacare," they might actually mean several different things. They could have Medicaid coverage through the expansion. They might have purchased a private plan through the Marketplace with government subsidies helping pay premiums. Or they bought a Marketplace plan paying full price themselves. All of these exist because of the ACA, but they're not all the same type of coverage.

Key Differences Between Obamacare and Medicaid

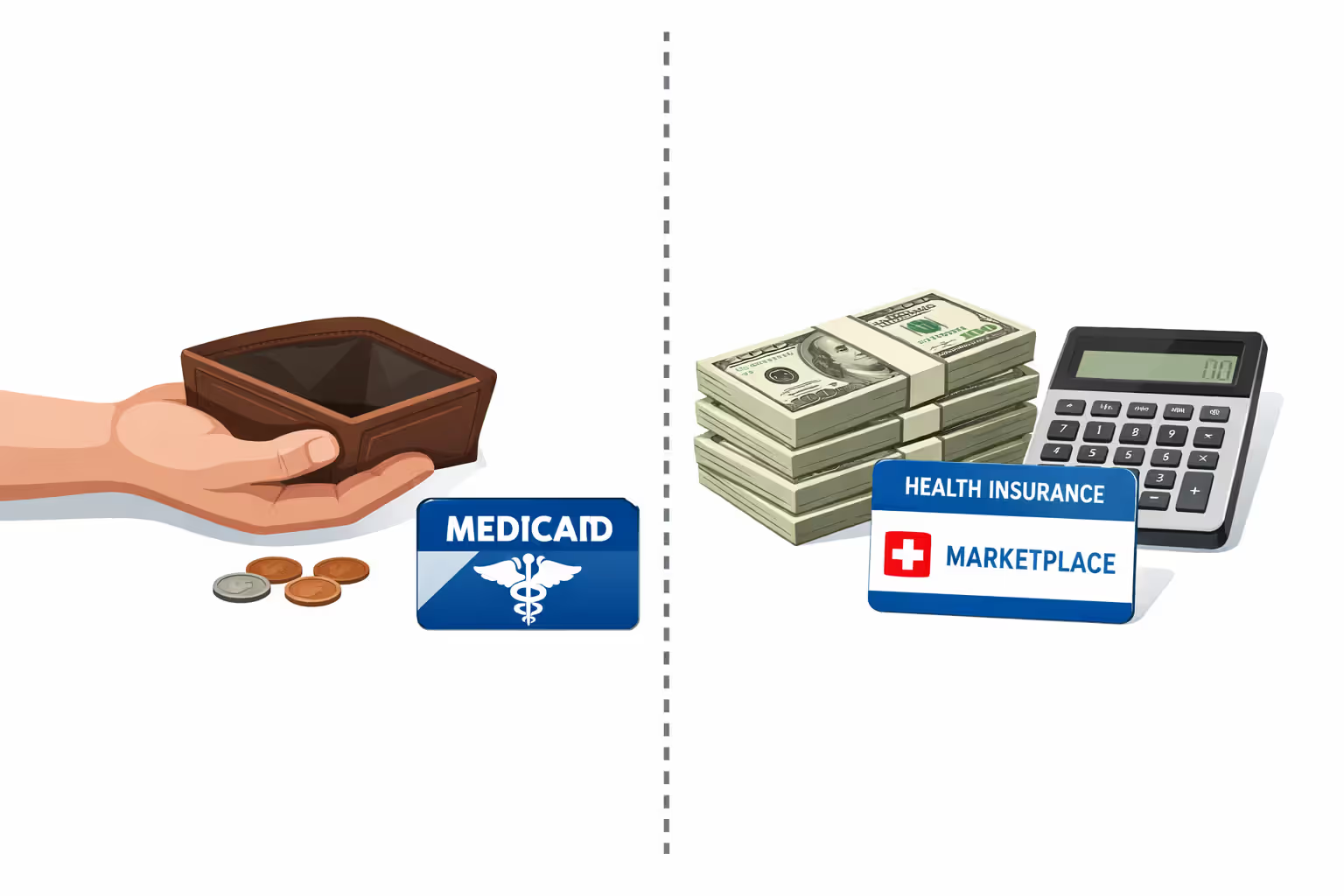

Medicaid runs as a joint federal-state insurance program. Your state and Washington D.C. split the costs—the federal government picks up at least 50% of traditional Medicaid expenses (and 90% for expansion populations). States administer their own Medicaid programs following federal minimum standards. You're not buying insurance; you're qualifying for a government benefit that pays your medical bills.

Marketplace plans work completely differently. You're purchasing private insurance from companies like Anthem, Cigna, or Oscar Health. These plans appear on Healthcare.gov or your state's exchange website. The government doesn't provide the insurance—it just runs the shopping website and potentially helps pay your premiums through tax credits.

Who qualifies creates the sharpest divide between programs. Medicaid in expansion states covers people earning up to 138% of the Federal Poverty Level—that's about $20,783 for one person in 2026. Below that threshold, you're directed to Medicaid. Above it, you shop the Marketplace (possibly with subsidies if your income stays under 400% FPL, around $60,240 for an individual).

The cost difference is dramatic. Medicaid members typically pay zero dollars in monthly premiums. Copays run extremely low—maybe $4 for a doctor visit or prescription. Some states charge nothing at all. Marketplace plans always require monthly premiums, even with subsidies. You'll face deductibles that could hit $3,000 or more before insurance really kicks in. A subsidized Marketplace enrollee earning $35,000 might still pay $200 monthly with a $2,500 deductible.

Author: Lauren Prescott;

Source: blaverry.com

Who Runs Each Program?

Every state operates its own Medicaid program, though they go by different names. New York calls theirs Medicaid. California rebranded as Medi-Cal. Tennessee uses TennCare. Kentucky has Medicaid but previously branded it as Kynect. Each state sets additional rules beyond federal requirements, decides provider payment rates, and processes applications through state agencies.

The Marketplace operates more like Amazon for health insurance. Healthcare.gov serves as the platform for 32 states, while 18 states built their own exchange websites (California's Covered California, New York's NY State of Health, etc.). But you're always buying from private insurance carriers. When you pick a plan, Aetna or whoever becomes your insurer—you're their customer, not a government program participant.

How You Enroll in Each

Medicaid doesn't care what month it is. You can apply in January, June, or October—whenever you need coverage. Lost your job in August? Apply for Medicaid in August. Baby due in December? Apply in December. State agencies must process applications within 45 days for most people, 90 days for disability determinations. Some states deliver decisions within a week or two.

Marketplace enrollment runs on a strict calendar. Open Enrollment typically starts November 1st and ends January 15th (though some state exchanges extend deadlines). Miss that window, and you're locked out until next year with narrow exceptions. You get a Special Enrollment Period if you lose other coverage, get married, have a baby, or move to a new state—but you've got only 60 days from that qualifying event to enroll.

How the ACA Expanded Medicaid Eligibility

Original Medicaid functioned as categorical. You couldn't just be poor—you had to be poor AND fit specific categories. Pregnant? Covered. Under 18? Covered. Over 65? Covered. Disabled? Covered. Healthy 35-year-old working part-time at a restaurant? Sorry, no coverage for you at any income level.

This created absurd situations. A single mom earning $15,000 could get Medicaid for her kids and maybe herself (depending on the state). Her childless brother earning the same $15,000 couldn't qualify anywhere. He made too little to afford Marketplace plans but didn't fit Medicaid's categories.

The ACA tried fixing this by making income the primary factor. Under expansion rules, any adult—single, married, with kids, without kids, healthy, sick—qualifies if their income falls below 138% of poverty. That's roughly $20,783 for a single person or $42,600 for a family of four in 2026.

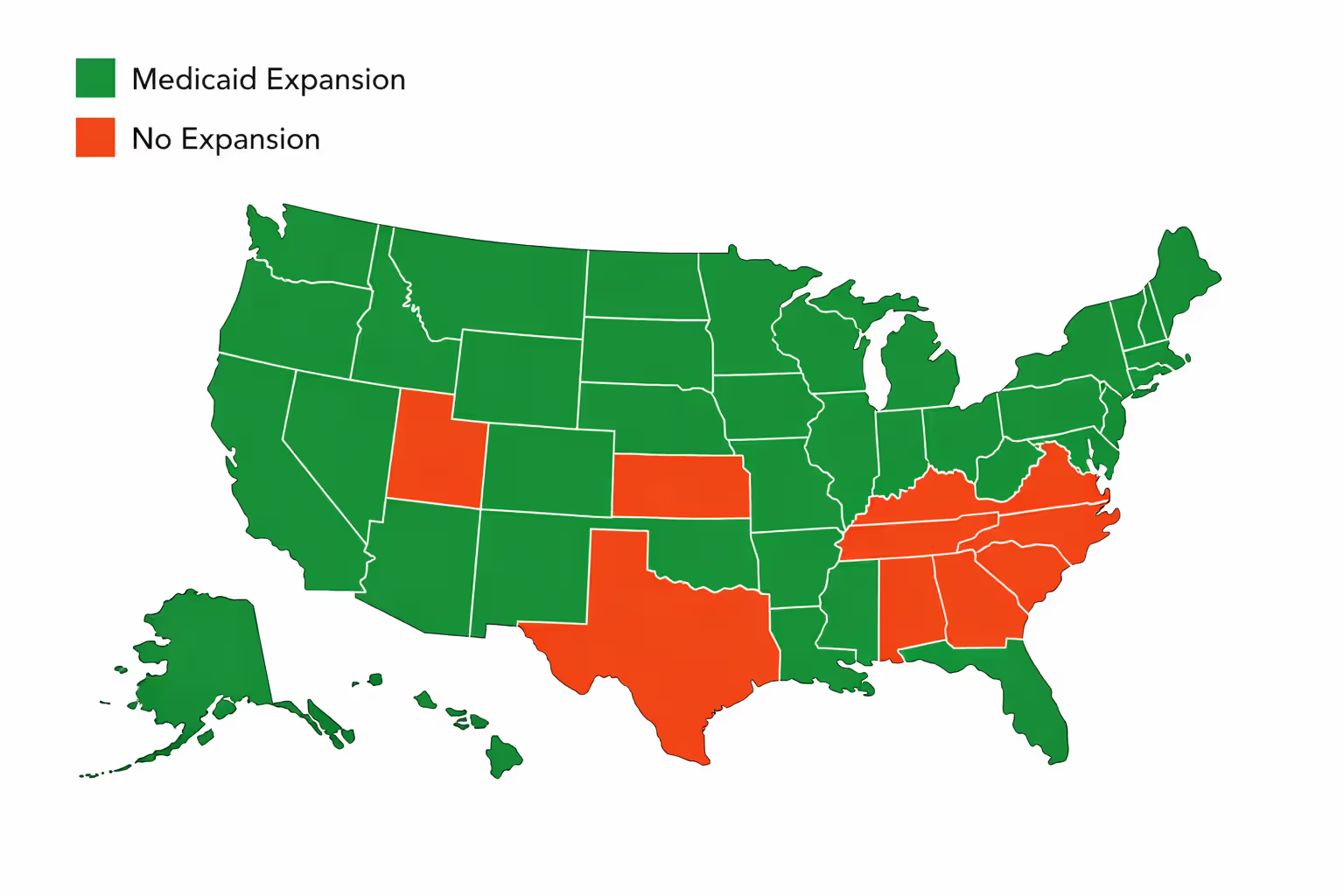

But here's where it gets messy. The Supreme Court ruled in 2012 that states could refuse expansion. As of 2026, ten states still haven't expanded: Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, Wisconsin, and Wyoming. These states kept their old restrictive rules.

In non-expansion states, that childless restaurant worker still can't get Medicaid at almost any income. Parents might need to earn under $5,000 annually to qualify—yes, that low. Alabama covers parents only if they make less than 18% of the poverty level (about $2,700 for an individual). Working parents earning $8,000 or $10,000 fall into a coverage gap: too much for Medicaid, too little for Marketplace subsidies.

The expansion transformed access for specific groups. Childless adults gained eligibility in the 40 states that expanded. Low-income parents with slightly higher earnings qualified for the first time. People with depression, anxiety, or addiction found coverage for mental health and substance abuse treatment. Near-retirees age 50-64 not yet eligible for Medicare finally got affordable coverage.

Author: Lauren Prescott;

Source: blaverry.com

Medicaid Income Limits and Eligibility Requirements Under the ACA

Medicaid calculates income using Modified Adjusted Gross Income—the same MAGI that determines Marketplace subsidies. Include your wages, self-employment profit, unemployment benefits, most Social Security payments, interest, dividends, and rental income. You can subtract certain deductions like student loan interest and IRA contributions that show up on your 1040 tax form.

Household size matters enormously. The Federal Poverty Level rises with each additional person. One person at 138% FPL can earn $20,783. Add a spouse and it jumps to $28,207. A family with two kids can earn $42,600. Your household includes yourself, your spouse if married, plus any dependents you'll claim on taxes—usually your kids under 19, or under 24 if they're full-time students you support.

State-by-state variations make this complicated. Connecticut covers adults up to 160% FPL for certain programs. District of Columbia extends pregnant women's Medicaid to 319% of poverty. Meanwhile, Texas covers parents only up to 17% FPL—that's $2,550 annually for one person. Missouri just expanded in 2021, so their rules are newer. Each state published different income charts.

Categorical eligibility still exists for certain groups. Pregnant women qualify at higher income levels—often 200% FPL or above. Kids can get Medicaid or CHIP coverage up to 250-300% FPL depending on state. Someone receiving Supplemental Security Income (SSI) automatically qualifies for Medicaid regardless of these income rules. Elderly and disabled populations may face asset tests (counting savings accounts and property), though expansion Medicaid doesn't look at assets for most adults.

People make predictable mistakes when calculating eligibility. They use gross pay instead of MAGI, forgetting about standard deductions. They don't count a college-age child they claim as a dependent. They leave out Social Security disability benefits, not realizing those count as income. A seasonal worker might calculate based only on three months of earnings rather than projecting the full year.

Can You Have Both Marketplace Insurance and Medicaid?

Short answer: No. Federal law prohibits carrying both simultaneously. You can't hedge your bets by keeping Medicaid while also buying a subsidized Marketplace plan. The programs were designed as separate tracks—one for people below 138% FPL, the other for people above that threshold.

The system automatically determines where you belong when you apply. Type your income and household size into Healthcare.gov, and the eligibility engine decides: Medicaid or Marketplace. If you're Medicaid-eligible, you can't access premium tax credits to subsidize a private plan. The system won't let you.

This creates headaches when income fluctuates month to month. Let's say you work construction—busy summer months paying $4,000, slow winter months paying $1,000. Summer income might push you above Medicaid limits while winter income drops you back down. Or you're a freelance graphic designer who lands one big $20,000 project that bumps annual income over the Medicaid threshold.

When income changes, you must report it within 30 days. If you're on Medicaid and income rises above 138% FPL, the state will disenroll you—but this triggers a Special Enrollment Period for Marketplace coverage. You've got 60 days to pick a plan. If you're on a Marketplace plan and income drops, you should report that too. You might newly qualify for Medicaid, allowing you to cancel the Marketplace plan and stop paying premiums.

Timing the transition requires attention. Medicaid coverage usually ends on the last day of the month when the state determines you're no longer eligible. Your Marketplace plan should start the first of the following month. Report income changes promptly to avoid gaps or overlaps.

Some people want to refuse Medicaid and buy Marketplace coverage instead. Maybe their doctor doesn't accept Medicaid. Maybe they prefer a broader provider network. Federal rules generally block this choice. Qualify for Medicaid, and that's your coverage option—you can't decline it to get subsidies for a private plan instead. Limited exceptions exist if you have access to employer coverage or Medicare, but not for simply preferring Marketplace over Medicaid.

How to Determine If You Qualify for Medicaid or Marketplace Coverage

Start with Healthcare.gov's free screening tool, accessible any time of year. It asks maybe a dozen questions: Where do you live? How many people in your household? What's your annual income? Do you have access to job-based insurance? Within five minutes, you'll see an estimate—Medicaid likely, subsidies likely, or full-price Marketplace.

Gather documents before diving into the full application. Grab recent pay stubs covering at least a month. Pull last year's tax return if you filed one. Self-employed folks need profit and loss statements. Have your Social Security numbers ready. You'll need proof of citizenship—a birth certificate, U.S. passport, or naturalization certificate work. Lawful immigrants need green cards or other immigration documents.

Author: Lauren Prescott;

Source: blaverry.com

The formal application starts at Healthcare.gov (or your state exchange). You'll answer detailed questions about household composition, income sources, and current coverage status. Behind the scenes, the system checks databases—IRS records, Social Security, immigration status. It screens for Medicaid first since that takes priority. Appear eligible, and your application gets forwarded to your state Medicaid office.

State agencies may request additional verification within a few weeks. They might want more pay stubs, bank statements, or a letter from your landlord confirming residency. Respond by the deadline on the notice—usually 10 days—or risk delays. Some states process applications incredibly fast; others take the full 45 days.

Common mistakes derail applications. People estimate annual income wrong—they multiply one month's paycheck by 12 when they only worked part of the year. They forget to include a working spouse's income. They claim a 19-year-old child who actually files their own taxes and isn't a dependent. Someone receiving unemployment lists only their old job's salary, forgetting that unemployment compensation counts as income.

If the determination seems wrong, appeal. Medicaid denials can be appealed through your state's hearing process—you've typically got 30 to 90 days. Marketplace eligibility disputes go through the federal appeals center. Submit documentation supporting your position: corrected income calculations, proof of household size, or documentation of special circumstances. Many people win appeals by simply providing information that was missing from the initial review.

Obamacare vs Medicaid: Key Differences at a Glance

| Feature | Medicaid | Marketplace (Obamacare) Plans |

| Program Type | Joint federal-state insurance program | Private coverage sold through government exchange |

| Who Qualifies | Adults with income up to 138% FPL in expansion states; stricter limits in other states | Anyone can purchase; subsidies available for 100-400% FPL |

| Income Limits | Approximately $20,783 (individual), $42,600 (family of four) in 2026 expansion states | No income ceiling; subsidy eligibility phases out around $60,240 (individual) |

| Cost | Zero or minimal premiums; copays often $4 or less | Monthly premiums required; deductibles range from $500-$9,000+ |

| Enrollment Period | Open year-round with no waiting period | November-January annually; Special Enrollment only after qualifying events |

| Who Administers | State Medicaid agencies following federal guidelines | Healthcare.gov or state exchanges; actual coverage from private insurers |

| Coverage Type | Comprehensive benefits with state flexibility within federal standards | Essential Health Benefits; specifics vary by metal tier (Bronze, Silver, Gold, Platinum) |

The biggest misconception I see working with applicants is thinking they can just choose Marketplace coverage if they don't like Medicaid. Someone will say, 'My doctor doesn't take Medicaid, so I'll buy a Silver plan instead.' That's not how eligibility works—if your income qualifies you for Medicaid, the system won't give you Marketplace subsidies. You're placed in the program your income determines, not the one you prefer

— Jennifer Martinez

Frequently Asked Questions About Obamacare and Medicaid

The relationship between the ACA and Medicaid confuses people because it's genuinely complicated. The Affordable Care Act isn't insurance you enroll in—it's the legal framework that expanded Medicaid and built the Marketplace system. These are separate coverage pathways that serve different populations.

Where you live and how much you earn determine which pathway opens for you. Earn under 138% of poverty in an expansion state? That's Medicaid. Earn more? You're shopping the Marketplace, possibly with significant subsidies. Live in a non-expansion state earning very little? You might fall into a coverage gap with no good options—too poor for Marketplace help, too "rich" for your state's Medicaid rules.

You can't choose between Medicaid and Marketplace based on personal preference. The system routes you according to income rules. But both programs deliver comprehensive coverage with protections for pre-existing conditions and essential health benefits—major improvements the ACA brought to American healthcare. Whether you end up with Medicaid or a Marketplace plan, you're accessing coverage that might not have existed or been affordable a decade and a half ago.