Top view of a desk with a laptop showing health insurance plan selection interface, calculator, stethoscope, dollar bills, and an insurance card

Marketplace Health Plans Guide for Enrollment

Content

Health insurance shopping ranks somewhere between doing taxes and assembling furniture without instructions on most people's list of enjoyable activities. But if you don't have coverage through your job—or your employer's plan costs more than your monthly grocery bill—the Health Insurance Marketplace could save you serious money while protecting you from medical debt.

Since the ACA launched these exchanges back in 2014, over 20 million people have used them to buy coverage. The marketplace isn't a one-size-fits-all government program. Think of it more like a carefully regulated shopping mall where private insurance companies compete for customers, and if your income falls within certain ranges, the government chips in to help cover your premiums.

Let's walk through everything you need to know, from checking if you qualify to actually picking a plan that won't leave you drowning in deductibles.

What Are Marketplace Health Plans

Private insurance companies sell their policies through two types of government-run websites: the federal HealthCare.gov platform (used by most states) or individual state-operated exchanges like Covered California or NY State of Health. The ACA built these online marketplaces to solve a problem—before 2014, buying individual insurance meant navigating hundreds of wildly different policies with confusing fine print and surprise gaps in coverage.

Now everything follows strict rules. All marketplace policies must include the same core set of ten protections: doctor visits, emergency room care, hospital stays, prescriptions, lab tests, mental health treatment, addiction services, pregnancy and newborn care, pediatric services, and rehab. You won't find a cheap plan that covers broken bones but not prescription antibiotics.

The standardization makes comparison shopping actually possible. Plans fall into four metal categories based on cost-splitting:

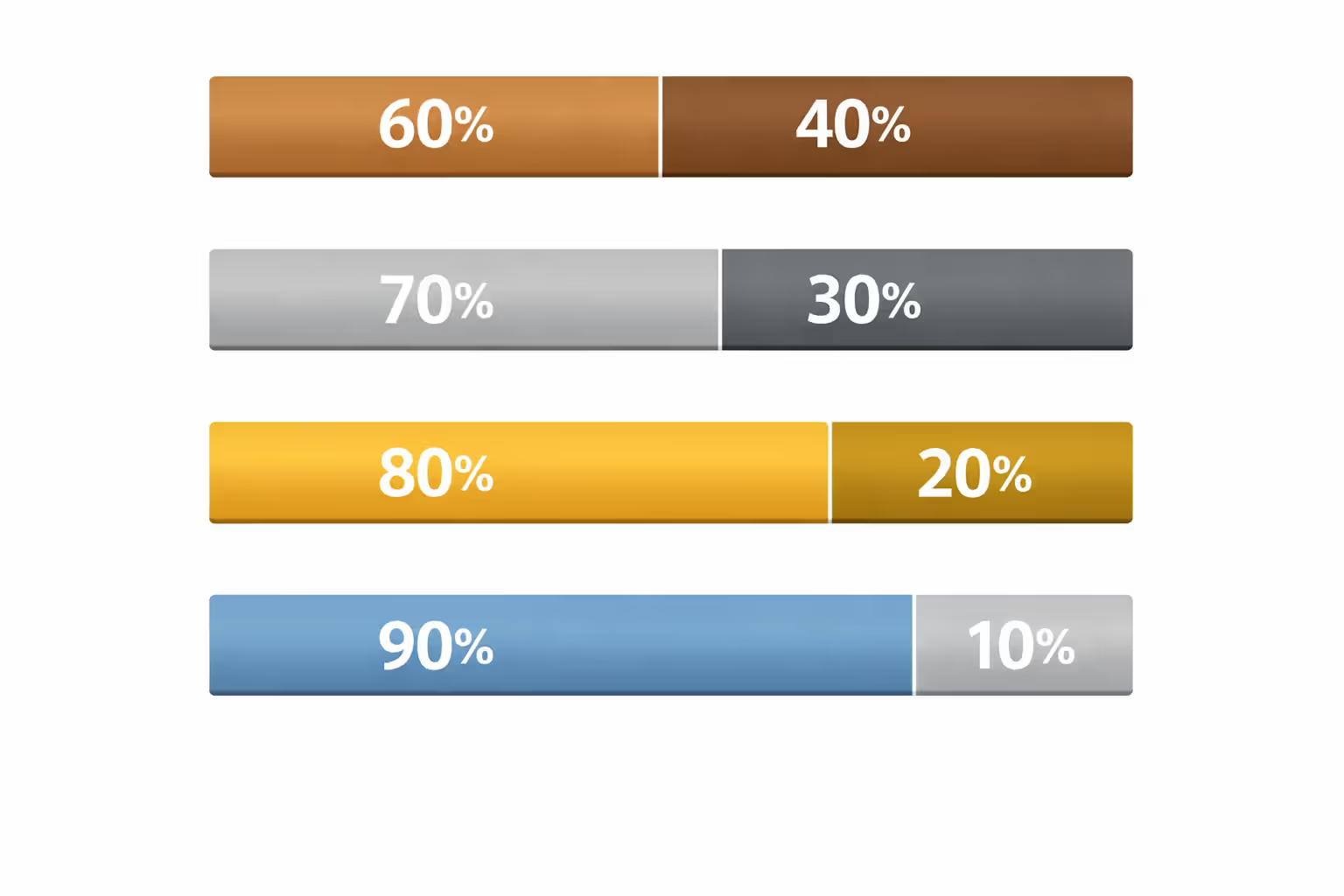

Bronze tier means lowest monthly bills but highest costs when you're sick. You'll pay roughly 60% of your medical expenses through deductibles and copays while insurance handles 40%. Great if you're 28, run marathons, and mainly need catastrophic protection.

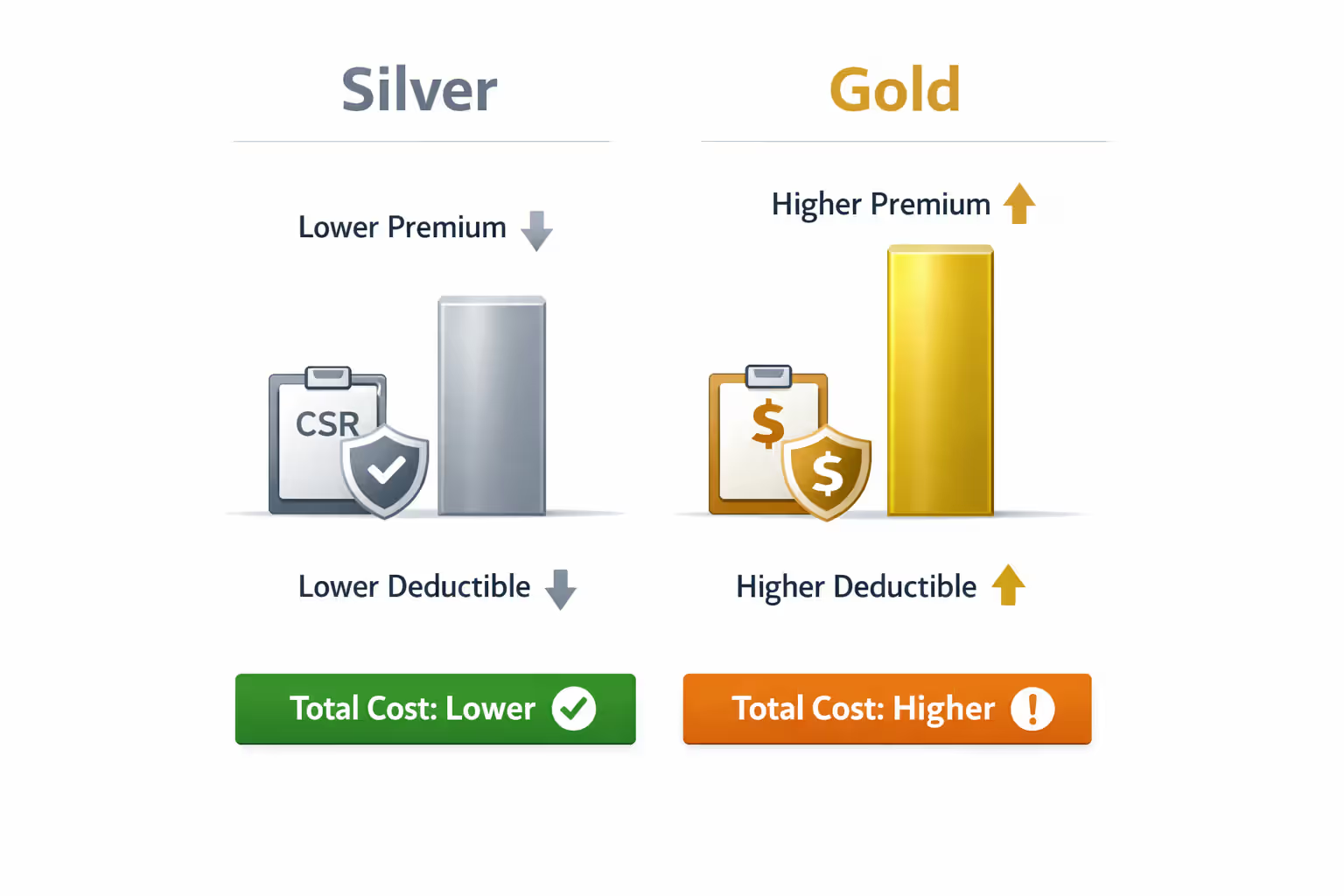

Silver tier splits costs about 70-30 between the insurer and you. Here's the kicker most people miss: Silver is the only tier where low-income enrollees get cost-sharing reductions—basically free upgrades that slash your deductibles and out-of-pocket maximums. A standard Silver plan might have a $6,000 deductible, but with cost-sharing reductions it drops to $2,000 or even lower.

Gold tier flips the script to 80-20 cost-sharing. You pay more every month but face smaller bills at the doctor's office or pharmacy. Makes sense for families managing diabetes, asthma, or other ongoing conditions.

Platinum tier delivers 90-10 coverage with the heftiest premiums but rock-bottom deductibles, sometimes under $1,000. If you're planning surgery, having a baby, or starting expensive treatments, Platinum prevents financial surprises.

Author: Lauren Prescott;

Source: blaverry.com

The same insurance giants offering employer plans—Blue Cross Blue Shield, Aetna, Cigna, Kaiser, UnitedHealthcare, plus regional carriers—sell marketplace policies. Your state determines how many compete for your business. Wyoming residents might see two options while New Yorkers could choose from a dozen.

Who Qualifies for Marketplace Health Plans

Basic eligibility boils down to legal status and residency. You need to be a U.S. citizen or have lawful immigration status—permanent residents with green cards qualify, along with refugees, people granted asylum, and holders of various work-authorized visas. Undocumented residents can't purchase marketplace plans even if they're willing to pay full freight without subsidies.

You must live in the United States and apply for coverage in your home state. Snowbirds who split time between Minnesota and Arizona need plans based on where they file taxes and maintain legal residence, not where they spend January through March.

Employment status matters less than you might think. Having a job doesn't automatically disqualify you. Millions of marketplace enrollees work full-time for employers that either don't offer insurance or charge premiums exceeding 9.02% of the worker's household income for basic self-only coverage. That affordability threshold determines subsidy eligibility—if your employer wants $500 monthly from someone earning $60,000 yearly, that's 10% of income, making you eligible for marketplace subsidies instead.

You can't double-dip into government programs. People already covered by Medicare, Medicaid, CHIP, or military TRICARE won't qualify for marketplace subsidies since they already have public coverage. Currently incarcerated individuals can't enroll, though release from jail or prison creates a special enrollment window.

Income Limits and Subsidy Thresholds

Financial assistance comes in two flavors that often confuse people. Premium tax credits reduce your monthly bill. Cost-sharing reductions (only available with Silver plans) shrink your deductibles and copays when you actually use healthcare.

Premium credits historically maxed out at 400% of the federal poverty level, but recent changes temporarily eliminated that ceiling. Now even households earning $125,000 might qualify if premiums in their area would otherwise exceed 8.5% of income. For 2026, poverty guidelines start at $15,060 for individuals and $31,200 for a family of four (higher in Alaska and Hawaii).

Let's make this concrete. A single 40-year-old earning $25,000 annually (about 166% of poverty level) would qualify for substantial premium reductions—likely paying $100-150 monthly for a Silver plan that would cost $450 without subsidies. A couple with two kids earning $70,000 (224% FPL) would also see meaningful assistance, though their subsidy would be smaller.

Cost-sharing reductions create a more limited eligibility window: 100% to 250% of poverty level, and only if you select Silver. These reductions transform a standard Silver plan into something resembling Gold or even Platinum coverage. Someone at 175% FPL might see their deductible drop from $6,500 to $2,500, with lower copays across the board. This is why Silver plans often beat Gold for people earning under $40,000 as individuals or $80,000 as families—the cost-sharing reductions provide better actual coverage despite the lower metal tier.

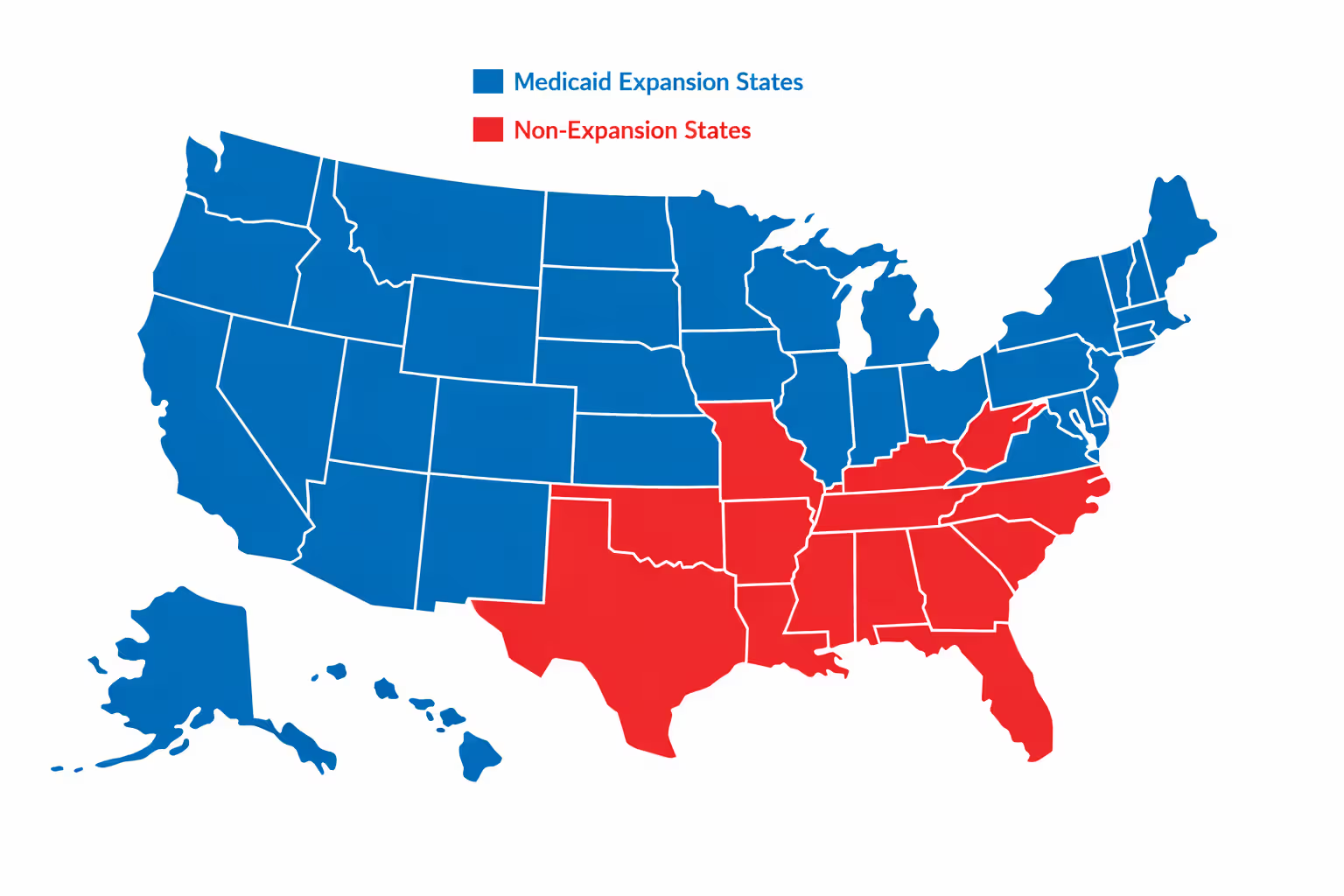

Medicaid expansion creates a dividing line between states. The 40 states (plus DC) that expanded Medicaid cover adults up to 138% FPL through that program instead of marketplace plans. The 10 holdout states leave people earning under 100% FPL in a coverage gap—too poor for marketplace subsidies but earning too much for their state's restrictive Medicaid programs unless they're pregnant, disabled, or meet other narrow criteria.

Author: Lauren Prescott;

Source: blaverry.com

How Marketplace Health Plans Work

Monthly premium payments work like any insurance—you pay or you lose coverage. Most people receiving subsidies choose "advance premium tax credits" where the government pays insurers directly each month, reducing your bill to the subsidized amount. You could instead pay full price and claim the entire credit when filing taxes, but that ties up thousands of dollars you probably need for rent.

Standard insurance mechanics kick in when you need care. Deductibles come first—the amount you pay before insurance starts covering most services. Bronze plans might stick you with $7,500 deductibles, meaning you're paying the full negotiated rate (lower than "retail" prices but still substantial) for doctor visits, tests, and medications until you've spent that much in the calendar year.

One huge exception: preventive care is free regardless of your deductible. Annual physicals, cancer screenings (mammograms, colonoscopies), childhood immunizations, blood pressure checks, cholesterol tests, and depression screenings cost you nothing. This rule exists because catching problems early costs insurers less than treating advanced disease.

After meeting your deductible, coinsurance takes over. Instead of paying full cost, you might pay 40% of the bill while insurance covers 60% (Bronze), or 20% versus 80% (Gold). This continues until you hit your out-of-pocket maximum—the legal cap on your annual spending, set at $9,100 for individuals in 2026. Once you reach that ceiling, insurance pays 100% for covered services through December 31.

Provider networks function as the invisible fence around your coverage. Most marketplace plans use HMO or PPO structures limiting where you can receive care. Visit an out-of-network doctor and you might pay the entire bill yourself, or face deductibles and coinsurance calculated from higher rates. Before enrolling, search the plan's provider directory for your current doctors—especially specialists like cardiologists, rheumatologists, or therapists you see regularly. Networks change, so call offices directly to confirm they're accepting new patients under that specific plan.

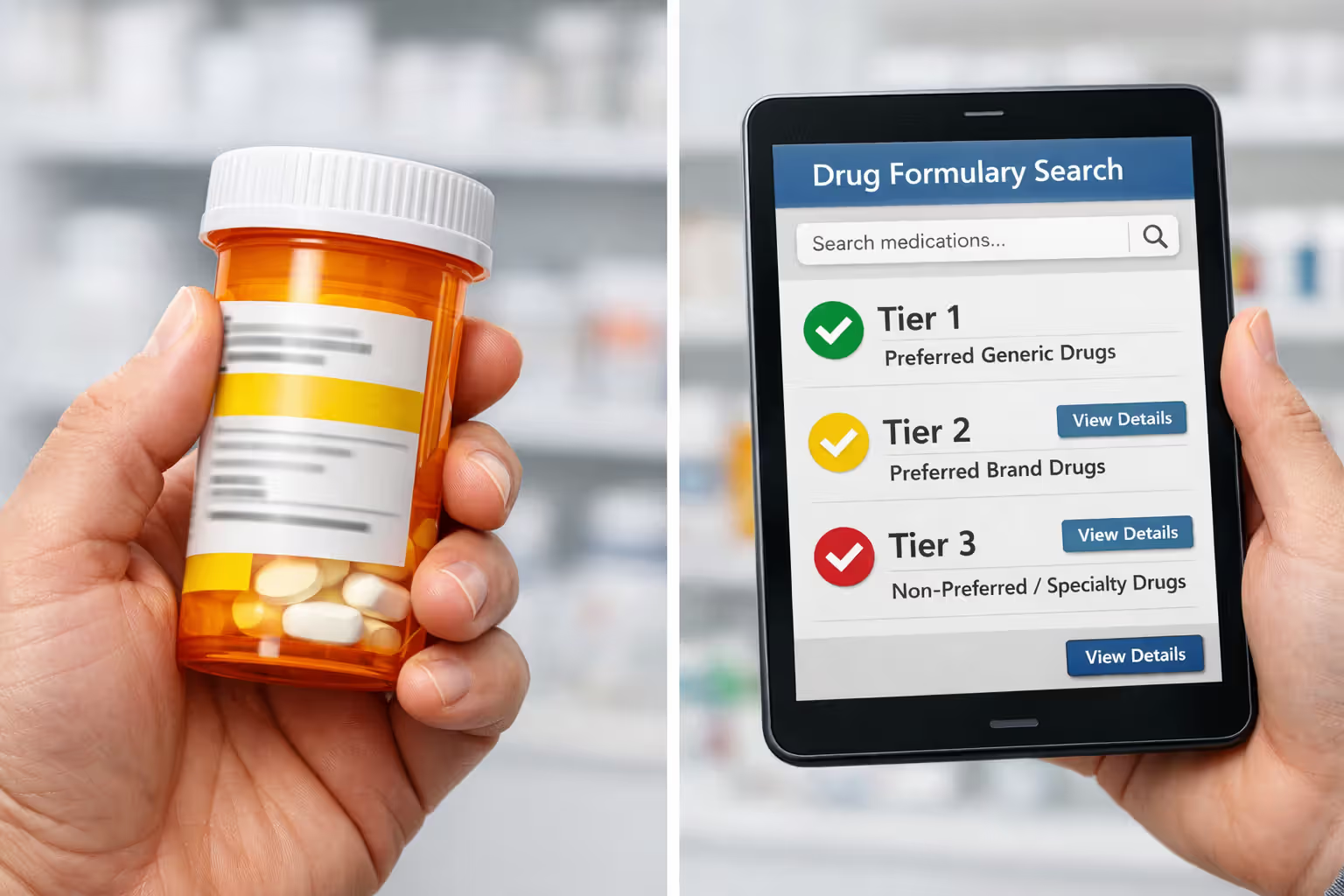

Prescription coverage varies dramatically despite all plans including it. Formularies—lists of covered drugs arranged in cost tiers—determine your pharmacy bills. One plan might place your blood pressure medication in tier 1 with $10 copays while another puts it in tier 3 at $75. Brand-name drugs often require "step therapy" (trying cheaper generics first) or prior authorization where your doctor must prove medical necessity before insurance approves coverage. Check formularies for every medication you take before enrolling.

Author: Lauren Prescott;

Source: blaverry.com

Cost-sharing reductions automatically apply when you're eligible—no separate application needed. Select a Silver plan while earning 100-250% FPL and the insurer builds reduced deductibles and copays into your coverage. You'll see the specific amounts (like "$2,500 deductible" instead of the standard "$6,500") in your plan documents. This makes Silver the sweet spot for many lower-income enrollees despite Gold's higher metal tier.

Documents and Information You Need to Apply

Applications move faster when you gather paperwork beforehand rather than scrambling mid-process. Start with Social Security numbers for everyone applying—required for identity verification and subsidy calculations. Even household members not seeking coverage (like a spouse with employer insurance) need their SSNs listed since household size affects subsidy amounts.

Income documentation proves your subsidy eligibility. Employees should collect recent pay stubs showing year-to-date earnings plus last year's W-2 forms. Self-employed individuals need their most recent tax return including Schedule C (business profit/loss) and Schedule SE (self-employment tax). Your application estimates current-year income, and if it differs significantly from last year—you switched jobs, got a raise, retired, started freelancing—the marketplace may request additional proof like offer letters or client contracts.

Current coverage details matter for determining whether you should switch to marketplace plans. If you're leaving employer insurance, bring the coverage end date and potentially a termination letter from HR. People offered COBRA continuation should have details about monthly costs and how long coverage lasts—information needed to compare whether COBRA or marketplace plans offer better value.

Immigration paperwork applies to non-citizens. Green card holders need their permanent resident card number and expiration date. Work permit holders should have their Employment Authorization Document (I-766). Refugees and asylees need their I-94 or approval notices. The system electronically verifies status when possible, but you might need to upload document photos if automatic verification fails.

Household composition determines both subsidy calculations and who must be included in your application. The marketplace uses your tax filing status to define "household"—not who lives at your address. Married couples filing jointly must include both spouses. Dependent children you'll claim on taxes count toward household size regardless of their age. Your roommate who files separately? Not part of your household for marketplace purposes, even if you split rent.

Special enrollment periods outside the annual open enrollment window require proof of your qualifying event. Job loss needs a coverage termination letter from your employer. Marriage needs a certificate. New babies need birth certificates. Moving to a different coverage area needs documentation like a lease, mortgage statement, or utility bill showing your new address and move date.

Marketplace Enrollment Timeline and Deadlines

Annual open enrollment gives everyone a chance to buy coverage or switch plans. For 2026 coverage, the enrollment window opens November 1, 2025, and closes January 15, 2026. When your coverage actually starts depends on your enrollment date. Sign up by December 15 and coverage begins January 1, giving you seamless protection. Enroll between December 16 and January 15, and you'll start February 1 with a coverage gap unless you have qualifying coverage bridging that month.

Missing this window doesn't condemn you to a year without insurance—but you'll need a qualifying life event to trigger a special enrollment period. You get 60 days from the qualifying event to enroll. These triggers include:

Losing existing coverage counts whether through layoffs, quitting, reduction in hours making you ineligible, aging out of a parent's plan at 26, divorce ending spousal coverage, or Medicaid termination. COBRA exhaustion qualifies. Voluntarily dropping coverage because you didn't feel like paying doesn't count.

Marriage and divorce both open enrollment windows. Gaining or losing dependents through birth, adoption, foster care placement, or court orders qualifies. Having a baby on March 15 gives you until May 14 to add the child to a plan or switch to family coverage.

Moving to a new coverage area means relocating to a ZIP code with different available plans—changing states certainly qualifies, but so does moving across town if your new address falls under different insurer service areas. Moving to college or temporarily relocating for work often doesn't qualify because you're not establishing a new permanent residence. Moving from a friend's couch where you were crashing to your own apartment at the same address doesn't count since you haven't changed locations.

Author: Lauren Prescott;

Source: blaverry.com

Income changes that make you newly eligible for subsidies or cause you to lose Medicaid can trigger special enrollment. Gaining citizenship or lawful immigration status qualifies. Leaving incarceration creates a window. Errors on your previous application that kept you from enrolling when you should have qualified can be corrected.

State marketplaces sometimes offer longer open enrollment or additional special enrollment opportunities beyond federal rules. California has extended its open enrollment into January in recent years. Massachusetts offers other unique windows. If your state operates its own exchange rather than using HealthCare.gov, double-check their specific calendar and qualifying events.

Coverage effective dates during special enrollment typically begin the first of the month after you enroll—but only if you complete enrollment by the 15th of the current month. Lose job coverage on March 10 and enroll March 20? Coverage starts April 1. Enroll March 8? You might get coverage starting March 1 depending on your state's rules.

That 60-day special enrollment clock is strict. Job-based coverage ends February 1, you procrastinate, and suddenly it's April 15? Too late—you've blown your window and must wait for the next open enrollment in November unless another qualifying event occurs.

Comparing Metal Tiers: Annual Costs and Coverage

| Metal Category | Typical Monthly Premium | Common Deductible | Out-of-Pocket Max | Insurer Covers | Works Best For |

| Bronze | $350–$450 | $6,500–$8,000 | $9,100 | ~60% of costs | Healthy people under 40 wanting catastrophic protection; minimal doctor visits; high risk tolerance |

| Silver | $450–$600 | $4,500–$6,500 | $9,100 | ~70% of costs | Most enrollees; mandatory if you want cost-sharing reductions; balanced monthly costs and coverage |

| Gold | $550–$750 | $1,500–$3,000 | $9,100 | ~80% of costs | Chronic conditions; regular prescriptions; planned procedures; frequent medical care |

| Platinum | $650–$900 | $500–$1,500 | $6,000 | ~90% of costs | Very high healthcare needs; multiple specialists; expensive ongoing treatment; want predictable spending |

Premium and deductible amounts vary widely based on age, location, tobacco use, and local insurer competition. These figures represent national averages for 40-year-old non-smokers in 2026.

How to Choose the Right Marketplace Plan

Picking the right metal tier requires honest assessment of your health needs and risk tolerance. The premium is just your entry fee—the real cost includes deductibles, copays, and coinsurance you'll actually pay when seeking care.

Start by projecting your healthcare usage. Healthy 30-somethings who went to the doctor twice in the past three years, take no regular medications, and need coverage mainly for accidents or unexpected illness? Bronze makes financial sense. You're gambling that you won't need much care and willing to pay steeply if that bet loses.

Anyone managing chronic conditions should run the math carefully. Someone with rheumatoid arthritis seeing a specialist four times yearly, getting quarterly lab work, and taking a $200 monthly biologic medication will spend thousands even with insurance. A Gold plan's $600 premium might cost $200 more monthly than Bronze ($2,400 annually), but if Gold's lower deductible and coinsurance save you $4,000 on medical bills, you're $1,600 ahead.

Silver plans with cost-sharing reductions deserve special scrutiny if your income lands between 100-250% FPL. A subsidized Silver premium might be $150 with a $2,000 deductible thanks to cost-sharing reductions. Compare that to Gold at $250 monthly with a $3,000 deductible. The Silver costs less per month ($150 vs $250 = $100 monthly savings = $1,200 annually) and has a $1,000 lower deductible. Silver wins by $2,200 annually despite the lower metal tier.

Author: Lauren Prescott;

Source: blaverry.com

Calculate total potential costs by multiplying monthly premiums by 12, then adding realistic out-of-pocket spending. If you know you'll hit your deductible, add that full amount. If you're uncertain, estimate based on planned care. Someone scheduling knee surgery should add their deductible plus likely coinsurance. Families expecting a baby should calculate the full out-of-pocket maximum since prenatal care, delivery, and newborn care often reach that cap.

Network adequacy requires detective work. Enter your doctors' names into each plan's provider search tool. Finding your primary care doctor listed is great, but what about the endocrinologist managing your thyroid? The physical therapist treating your back? The hospital where your preferred surgeon operates? Plans might include your primary doctor but none of your specialists, forcing you to switch providers or pay out-of-network rates that don't count toward your deductible.

Call doctors' offices—don't just trust online directories that lag behind actual network changes. Ask specifically: "Are you accepting new patients with

from for 2026?" Networks shrink and expand constantly, and directory websites might show doctors who left the network months ago.Formulary checking prevents prescription sticker shock. Every plan's website includes a drug search tool. Enter each medication you take and note the tier placement. Tier 1 (generics) usually cost $10-20. Tier 2 (preferred brands) run $50-100. Tier 3 (non-preferred brands) can hit $150-300. Specialty tiers for biologics and expensive medications might cost 30-50% of the drug price up to hundreds monthly. Some drugs require prior authorization or step therapy regardless of cost, adding hassle even if you can afford them.

Common mistakes include: - Choosing Bronze when Silver would cost less overall thanks to cost-sharing reductions - Focusing only on premium amounts while ignoring deductibles and copays - Assuming all plans cover your current doctors without verification - Failing to check prescription formularies until after enrollment - Not reporting mid-year income changes, creating subsidy repayment problems at tax time

Expert Perspective on Marketplace Coverage

I see people choose Bronze plans to save $100 monthly, then panic when their hospital bill comes to $50,000 and they owe $7,000 before insurance pays a dime. For most families earning 150-250% of poverty level, Silver plans with cost-sharing reductions beat every other option—sometimes providing better protection than Gold at lower total cost. But you'd never know that from just comparing premiums. Do the math with your actual expected medical use, not best-case scenarios where nothing goes wrong

— Jennifer Martinez

Frequently Asked Questions About Marketplace Health Plans

Shopping for marketplace health plans forces you to balance affordability against financial protection while navigating subsidy thresholds, provider networks, prescription formularies, and four metal tiers with different cost-sharing structures. The complexity is real, but the standardization of benefits means you're comparing genuinely similar products rather than decoding fine print hiding coverage exclusions.

Begin with honest health projection rather than wishful thinking. Calculate total potential annual costs—premiums multiplied by 12, plus realistic out-of-pocket spending based on your actual medical needs. Factor in subsidies carefully, paying particular attention to Silver tier cost-sharing reductions if your income falls between 100-250% FPL. Those reductions often make Silver the best value despite lower metal tier designation.

Confirm network participation for all your current providers before committing to any plan. Search provider directories for your doctors, then call offices directly to verify they're accepting new patients under that specific insurance. Check prescription formularies for every medication you take, noting tier placement and any restrictions like prior authorization requirements.

Remember that marketplace enrollment operates on strict timelines. Missing open enrollment means waiting until next year unless you experience qualifying life events like job loss, marriage, birth, or relocation. Gather your documentation early—Social Security numbers, income verification, current coverage details, and immigration papers if applicable. Report income changes promptly to avoid subsidy problems at tax time.

The marketplace has connected more than 20 million Americans to private insurance coverage who otherwise couldn't access or afford it. Understanding eligibility rules, navigating metal tier tradeoffs, and choosing appropriate coverage levels transforms the system from overwhelming bureaucracy into a manageable path toward protecting your health and your finances.