Person sitting at kitchen table reviewing health insurance documents and paperwork with laptop open nearby

COBRA Health Insurance Coverage Guide

Content

Picture this: You just walked out of your manager's office after getting laid off. Your brain's spinning through mortgage payments and job boards—then reality hits. What about health insurance? Here's the thing nobody warns you about: federal law actually requires your old employer to keep you on their plan. The catch? Now you're footing the entire bill yourself, sometimes triple what disappeared from your paychecks.

Back in 1985, Congress buried a healthcare provision inside the Consolidated Omnibus Budget Reconciliation Act—which created that clunky COBRA acronym we're stuck with. That provision made it illegal for most employers to immediately yank health coverage from departing workers. Sounds great until you see the price tag. Still, depending on your situation, paying those steep premiums beats the alternatives.

What Is COBRA Coverage?

Think of COBRA as a federal mandate forcing companies with 20+ employees to let you stick around on their group health plan after separation—assuming you're willing to pay what used to come out of company coffers. These rules cover private businesses, nonprofit organizations, and local government agencies running group health plans that meet the size threshold.

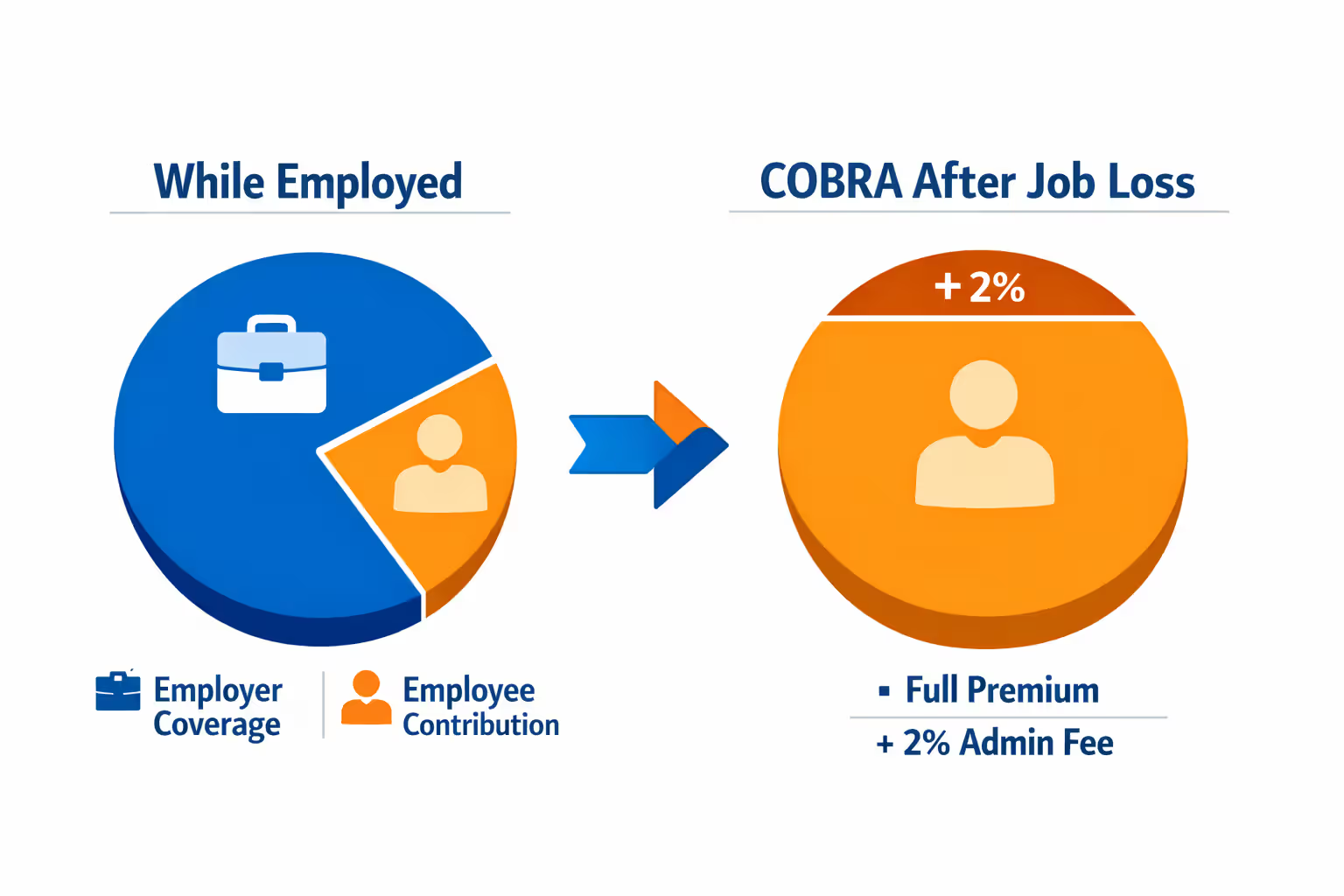

During your employment, your company likely shouldered 70%-85% of your total health insurance costs. You kicked in the rest through automatic paycheck deductions. Now imagine covering both pieces yourself while your former employer adds a 2% administrative charge on top. Let's say the company was paying $850 each month while $150 came from your pay. Your new monthly invoice? $1,020.

Everything else stays identical. Same insurance card. Same doctors. Same pharmacy benefits. That deductible you'd been chipping away at since January? It carries forward exactly where you left off—you're not wiping the slate clean. The only thing changing is who writes the checks.

Most people treat this as temporary. Maybe you've got promising interviews lined up and expect a new position within six weeks. Maybe you're 64 and can practically taste Medicare eligibility. Maybe you need breathing room to dig through Healthcare.gov options. Federal law doesn't force your old employer to contribute even a single dollar after you're gone. They just can't slam the door in your face.

Author: Derek Whitmore;

Source: blaverry.com

The Department of Labor handles enforcement. Companies that "accidentally forget" to inform departing employees about these continuation rights end up paying penalties. Many states run parallel programs—often called mini-COBRA—that protect workers at smaller companies (2-19 employees), though the specifics bounce around wildly depending on where you live.

Who Qualifies for COBRA Coverage?

Your eligibility depends on three things: how many people work at your company, whether you had coverage right before separation, and what caused you to lose that coverage. Flunk any one of these tests and your continuation options vanish.

Company size comes first. The business needs at least 20 employees working more than half the typical business days during the previous calendar year. Part-timers count proportionally based on hours. Federal government employees follow different rules through the Federal Employee Health Benefits program—COBRA doesn't touch them.

You had to actually be enrolled in the group plan the day before your qualifying event. Turned down coverage when you started the job? You can't suddenly invoke COBRA after getting fired to undo that old decision.

Qualifying Events That Trigger COBRA

What specifically ended your coverage determines how many months of continuation you'll get. For employees themselves:

Your job ends—for basically any reason: Termination, resignation, company restructuring that eliminated your position? All these count, as long as you weren't canned for gross misconduct. Your last official workday starts the COBRA timeline.

Your hours drop below the plan's participation threshold: Companies struggling financially sometimes slash full-time employees to part-time hours. When that reduction disqualifies you from staying on the plan, continuation rights kick in.

Spouses and kids have extra qualifying scenarios:

The covered employee dies: Family members who were enrolled keep their continuation eligibility.

Divorce or legal separation gets finalized: Ex-spouses lose access to their former partner's employer plan.

The covered employee becomes Medicare-eligible: When the working spouse hits Medicare eligibility (usually at 65), the younger spouse and any dependents may lose the group plan.

A dependent ages out of coverage: Most plans boot dependent children at age 26. Losing that dependent status triggers individual continuation rights for the child.

When You're Not Eligible

Getting fired for gross misconduct kills your COBRA rights, though regulations never spell out exactly what "gross misconduct" means. Employers usually interpret this strictly—think embezzling company funds, assaulting coworkers, or egregious safety violations. Ordinary lousy performance doesn't count.

When your company terminates the entire group health plan—shutting down the business or axing all employee benefits—there's nothing left to continue. You can't elect coverage that doesn't exist anymore.

Already enrolled in another group plan when you'd lose coverage? COBRA rights might not kick in, though timing gets complicated. Became Medicare-eligible before your election period started? That typically disqualifies you.

How Does COBRA Coverage Work?

Continuation involves tight deadlines and split responsibilities between your old employer, the plan administrator, and you. One blown deadline can permanently erase your options.

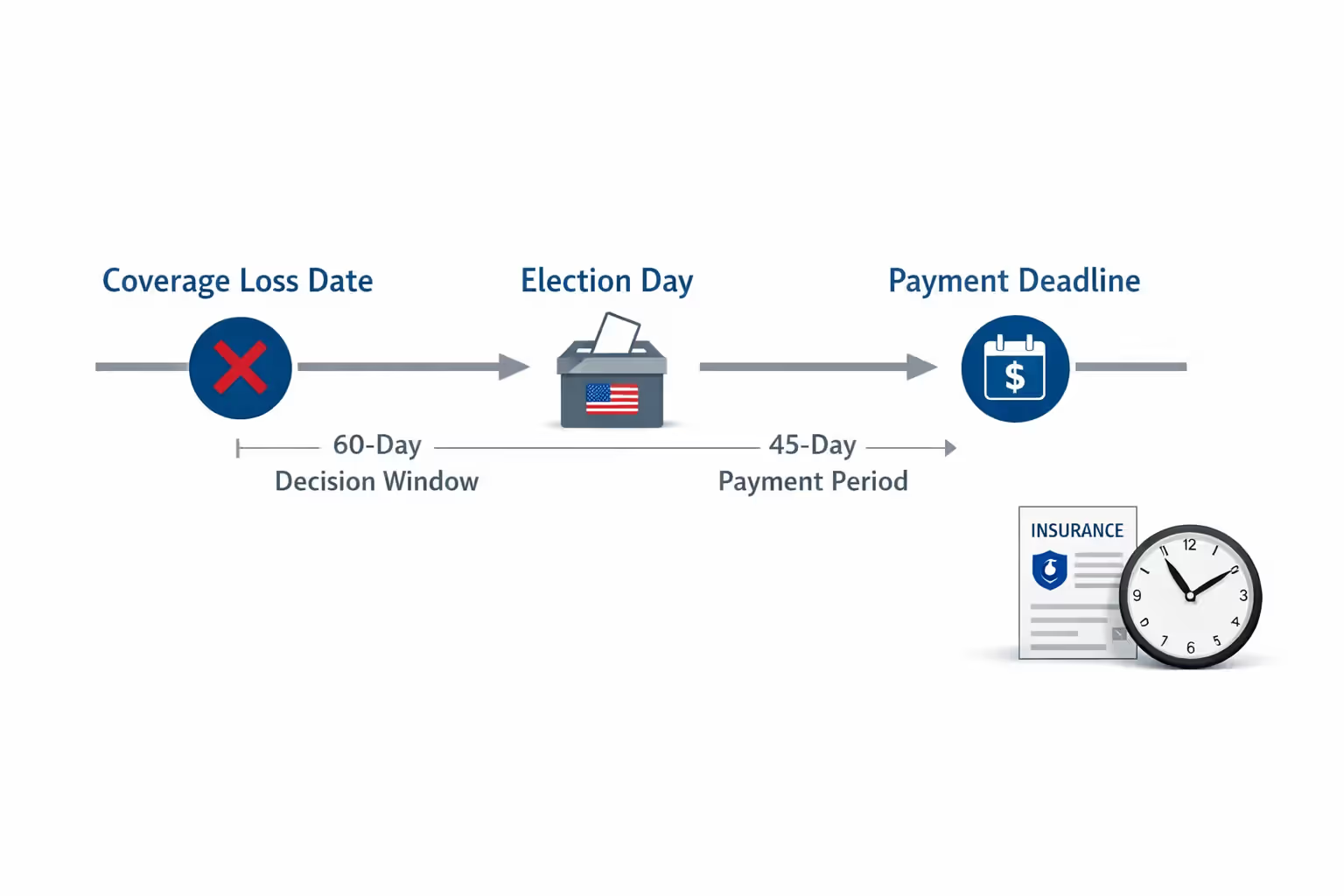

Notices from plan administrators: Administrators get 14 days after learning about qualifying events like terminations or hour cuts to mail election notices explaining your rights, premium amounts, and crucial deadlines. Employers know immediately about job separations. For divorce or kids aging out, you've got to notify administrators within 60 days yourself—they won't stumble across your personal life changes.

Your decision window: You get 60 days to decide, counting from whichever happens last: losing coverage or getting official notification. Your existing coverage keeps working during these 60 days. Some people wait strategically until day 60, check whether they've racked up medical bills, then choose accordingly. Stayed healthy? Skip COBRA. Got hospitalized on day 45? Elect retroactively.

Retroactive activation: Choosing COBRA rewinds coverage back to your loss date. Had emergency gallbladder surgery on day 30 of your decision window, then elected on day 55? That surgery's covered. Deductible progress you'd accumulated all year transfers forward—already paid $3,000 toward a $5,000 deductible in May before getting laid off? You'd only owe the remaining $2,000, not start over.

Author: Derek Whitmore;

Source: blaverry.com

What continues: Medical, dental, and vision plans all fall under COBRA protection. Health Flexible Spending Accounts might continue if they're showing positive balances. Health Savings Accounts don't need COBRA—you own that account forever regardless of employment.

Administrator responsibilities: Plan administrators must spell out exact premium figures, payment due dates, and coverage duration. They're required to warn you before terminating coverage for non-payment or hitting maximum duration.

COBRA Coverage Cost and Payment Rules

Continuation premiums equal the full plan cost plus administrative charges—way higher than what vanished from your paychecks. Employer-sponsored coverage in 2026 averages around $8,700 yearly for single employees and $24,000 for family plans. Now tack on 2%.

How premiums get calculated: Take the total plan cost, add 2%. A $1,000 monthly plan that used to cost you $200 (employer covered 80%) now runs $1,020 monthly. Family coverage averaging $2,000 monthly jumps to $2,040.

Initial payment deadline: You've got 45 days from electing to pay. This first payment needs to cover every month from your coverage loss through the payment date. Coverage ended March 1st? Elected April 20th? That initial check (due June 4th) covers March through June—potentially four months at once, topping $4,000.

Ongoing monthly payments: These come due the first day of each month, though you get a 30-day grace period. Payment landing by the grace period's final day keeps your coverage active. Miss that cutoff? Coverage terminates retroactively to your last fully-paid month's end. Emergency surgery mid-grace-period then your payment showed up late? You're stuck with that potentially six-figure hospital bill.

Payment methods accepted: Administrators must take checks and money orders. Electronic payments—while more common now—aren't mandatory. Always keep payment proof. Ship checks via certified mail with return receipt. Screenshot every electronic confirmation. Payment disputes? You'll need to prove you paid on time.

Zero subsidy availability: Health Insurance Marketplace plans offer premium tax credits that slash monthly costs for households earning 100%-400% of federal poverty levels. COBRA? Never qualifies no matter what you earn. Congress temporarily subsidized COBRA during 2021 pandemic relief. That ended and hasn't come back.

COBRA Deadlines and Coverage Period

Timeline complexity trips up tons of people. Understanding every deadline prevents permanently losing your options.

Sixty-day election period: This is your decision window. Lots of people mistakenly think they need to decide immediately. You can intentionally wait the full 60 days, checking your health needs and exploring alternatives. Some strategically decline unless major medical expenses pop up during the window, then elect retroactively only if necessary.

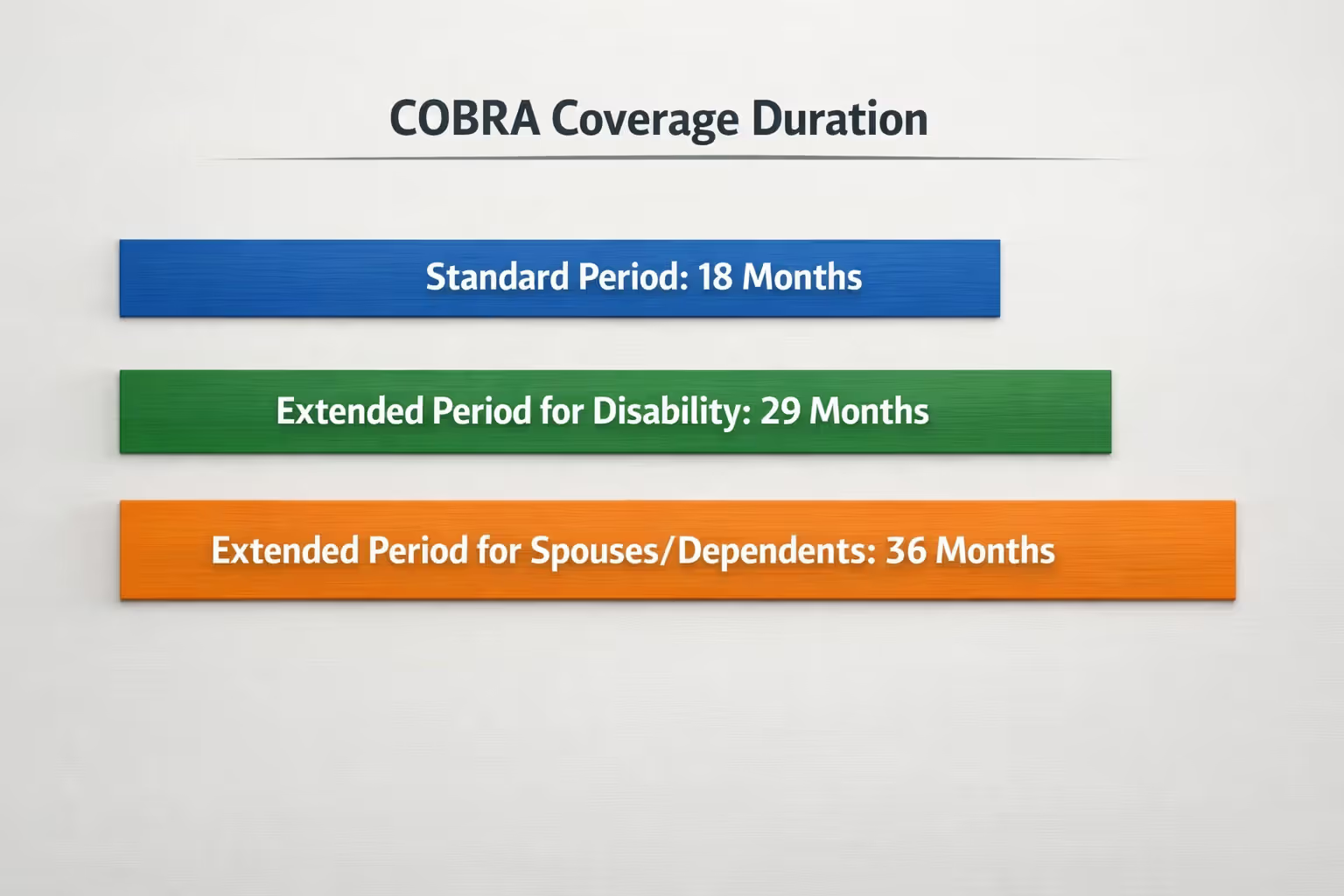

Standard 18-month duration: Employees losing coverage from termination or reduced hours typically get 18 months continuation. This clock starts when your group coverage ended, not when you elected or sent initial payment.

Author: Derek Whitmore;

Source: blaverry.com

Extended 36-month duration: Spouses and dependents losing coverage through divorce, separation, employee death, or the employee's Medicare entitlement can continue 36 months.

Disability extension possibility: When Social Security Administration determines you or covered family members disabled within your first 60 COBRA days, you might stretch the 18-month period to 29 months. You must notify plan administrators within 60 days of getting that disability determination and before your initial 18 months expires. Premiums may jump to 150% of full cost during months 19-29.

Second qualifying events: Imagine you're on 18-month continuation after a layoff, then your divorce finalizes during month 10. Your spouse can extend continuation to 36 months total from your original job loss.

Early termination triggers: Coverage ends before hitting maximum duration when you stop paying premiums, gain coverage under a new group health plan (some exceptions apply for pre-existing condition situations), become Medicare-entitled, or your former employer eliminates the group plan entirely for all current employees.

COBRA Coverage vs Marketplace Insurance

Choosing between continuation and Healthcare.gov plans requires comparing real costs, coverage differences, and your specific circumstances. Neither option wins automatically—the right call depends on your health status, income, and how quickly you expect new employment.

| Feature | COBRA | Marketplace/ACA Plans |

| Monthly premium | Full cost plus 2% admin fee; usually $700-$2,000+ individuals, $2,000-$2,500+ families | Varies significantly; income-based subsidies available; ranges $0 to $1,500+ after tax credits |

| Coverage start date | Retroactive to your loss date | Usually the month after enrollment; requires special enrollment period |

| Subsidy eligibility | Never qualifies for premium tax credits or cost-sharing reductions | Tax credits available for incomes 100%-400% of federal poverty level |

| Plan choices | Locked into your previous employer's single plan | Choose from multiple carriers at Bronze, Silver, Gold, Platinum tiers |

| Ability to switch plans | Impossible; you're stuck | Can pick a different plan during special enrollment |

| Duration limits | 18-36 months maximum depending on qualifying event | Year-round coverage; annual open enrollment to switch; no maximum duration |

COBRA makes sense when: You're halfway through the calendar year having already paid $4,000 toward a $5,000 deductible. Switching plans wipes that progress clean. You're undergoing cancer treatment with specialists in your current network—changing plans disrupts established care relationships. You expect new employer coverage within 2-3 months. Your income exceeds Marketplace subsidy thresholds, making COBRA and ACA plan costs roughly comparable.

Marketplace plans win when: It's early January—you've only contributed $500 toward your deductible, so switching costs less. Your income qualifies you for tax credits, potentially cutting premiums by $200-$400 monthly. You need coverage exceeding 18 months. Your former employer's plan featured narrow networks or high cost-sharing. You're self-employed long-term or facing extended unemployment.

Running subsidy calculations: For 2026, someone earning $40,000 annually might receive $300-$400 monthly tax credits. A Silver Marketplace plan costing $450 monthly drops to $100-$150 after subsidies versus $700+ for COBRA with similar or better coverage.

I've counseled hundreds of terminated employees who assumed COBRA was their only option. That's almost never true. Unless you've already knocked out your annual deductible or need continuity with highly specialized providers, Marketplace plans with tax credits cost dramatically less—sometimes one-fifth of COBRA premiums. Last month I helped a client paying $650 monthly for COBRA who switched to a $75 monthly Marketplace plan with lower out-of-pocket maximums

— Jennifer Martinez

Common COBRA Mistakes to Avoid

Missing the election deadline: That 60-day window is absolute. Let it expire and continuation rights disappear forever—even if you're hospitalized the next day. Set smartphone reminders for day 50. Waiting until day 59 creates risk if you miscalculate the start date or mail delivery delays the notice.

Skipping comparison shopping: Never assume continuation represents your best bet. Visit Healthcare.gov within days of losing coverage to compare costs and verify subsidy eligibility. Job loss triggers special enrollment, so you're not stuck waiting for November's open enrollment period.

Ignoring the 45-day initial payment rule: Electing COBRA doesn't activate anything—payment does. Elect on day 60 of your decision window? You immediately owe two to three months of retroactive premiums within 45 days.

Not keeping payment documentation: Plan administrators sometimes claim they never got your check. Always keep proof: certified mail receipts for checks, bank records showing cleared payments, or screenshots of electronic confirmations. You'll be the one who has to prove timely payment if there's a dispute.

Failing to self-report qualifying events: Divorce, legal separation, or dependent turning 26? Plan administrators won't magically discover these. You must notify them within 60 days of personal life events. Miss that deadline, lose rights completely.

Assuming continuation covers all benefits: COBRA continues health plans—medical, dental, vision. Your life insurance, disability coverage, 401(k) matching, and employee assistance programs typically end with employment. Read election notices carefully to understand what continues versus what stops.

Treating grace periods casually: That 30-day grace period for monthly payments seems generous until you realize coverage terminates retroactively at the grace period's end without payment. Schedule surgery mid-grace-period, then payment arrives late? You're personally liable for potentially tens of thousands in surgical bills.

Author: Derek Whitmore;

Source: blaverry.com

Ignoring coverage end dates: Eighteen months arrives shockingly fast. By month 16 of continuation, start researching Marketplace alternatives or Medicare eligibility if you're approaching 65. Waiting until month 18 provides zero buffer for application processing delays, potentially creating uninsured gaps.

Frequently Asked Questions

COBRA functions as critical protection when employer-sponsored health insurance suddenly disappears, despite being expensive and temporary. The law guarantees identical coverage continuation, which proves most valuable when you're mid-treatment, you've already satisfied your deductible, or you need brief bridges to new employer benefits.

Before electing continuation, comparison shop Marketplace plans during your special enrollment period. Premium tax credits can slash monthly costs dramatically for qualifying incomes. Calculate break-even scenarios: when you've paid $4,000 toward your deductible in March and lose your job, spending $700 monthly for continuation through December might beat starting fresh with a $5,000 deductible Marketplace plan costing $300 monthly after subsidies.

Track every deadline obsessively—the 60-day election window, 45-day initial payment requirement, and 30-day grace periods for monthly premiums. Set multiple calendar reminders and maintain documentation of all notices and payments. Consider your coverage needs realistically: healthy individuals with no ongoing treatments usually find better value in Marketplace coverage. Those with scheduled surgeries or chronic conditions requiring specific specialists might justify continuation's higher cost for treatment continuity.

Review options immediately after losing coverage. Delaying weeks to compare plans or verify subsidy eligibility restricts your choices unnecessarily. COBRA's retroactive coverage during election periods combined with Marketplace special enrollment creates flexibility—use it strategically to make the most cost-effective decision for your situation.