Small business owner at desk with laptop showing expense charts, employees working in background in a modern office

Employer Reimbursement for Health Insurance Premiums Guide

Content

Here's a problem thousands of small business owners wrestle with: your competitors offer health benefits, but traditional group insurance feels impossibly expensive. Premium renewals arrive like bad news—12% increase this year, take it or leave it. And the paperwork? It's enough to make you question whether you should've hired an HR team yesterday.

There's another path forward. Instead of buying a group plan, you can help employees pay for individual coverage they pick themselves. You set aside a fixed monthly amount. They shop for insurance that actually works for their family. You reimburse them through payroll, following IRS rules that make the money tax-free for everyone involved.

Employees get real choice. You get predictable costs. Everyone avoids the headaches of group insurance administration.

What Is Employer Reimbursement for Health Insurance Premiums?

Picture this: rather than selecting a group health plan that half your team dislikes, you establish a monthly budget per employee. They go shopping for individual insurance—through Healthcare.gov, a private broker, directly from carriers—and pick coverage matching their doctors, prescriptions, and budget. Once they buy a policy and show you proof, you reimburse them up to your set limit.

The IRS recognizes two main structures for doing this properly: QSEHRA (Qualified Small Employer HRA) and ICHRA (Individual Coverage HRA). Both let you provide tax-advantaged reimbursements, but they follow different rules.

QSEHRA works for companies under 50 full-time employees that aren't offering a group plan. The government caps how much you can contribute—in 2026, that's $6,350 yearly for single coverage and $12,800 for family coverage. You can adjust amounts based on whether someone has individual or family insurance, but you can't play favorites within each category. Everyone with single coverage gets the same deal.

ICHRA arrived in 2020 and threw out the rulebook in useful ways. No employee-count restrictions. No federal caps on contributions. Want to offer $2,000 monthly? Go ahead. Have 500 employees? You're eligible. You can create different allowance levels for distinct employee groups—full-timers versus part-timers, different locations, hourly versus salaried staff—as long as everyone in each group gets equal treatment.

Some employers skip the formal arrangements and just add "health insurance money" to paychecks. Bad idea. Those payments are taxable income, and worse, they may violate ACA rules against informal reimbursement plans. You could face penalties of $100 daily per affected employee. The IRS doesn't joke around here.

How Does Employer Reimbursement for Health Insurance Premiums Work?

The mechanics are simpler than you'd think, though details matter for compliance.

You start by establishing your arrangement—deciding monthly amounts, documenting your plan terms, and notifying employees. That notice must arrive at least 90 days before your plan year kicks off, or before a new hire starts work, whichever comes first. Miss that deadline and you're already in compliance trouble.

Employees then shop. They're not limited to your pre-selected options like with group insurance. Marketplace plans, off-exchange policies, coverage through a spouse's employer if they pay premiums—anything meeting "minimum essential coverage" standards qualifies. They complete enrollment and start paying their carrier directly.

Here's where substantiation comes in. Your employee submits documentation—typically an insurance card showing active coverage plus a billing statement or bank record proving they paid. You review these materials (or your third-party administrator does) to confirm everything meets requirements.

Once approved, reimbursement processes through your regular payroll. Most employers handle this monthly, though some align with their existing payroll schedule. The payment appears on the employee's W-2, but when structured correctly, it's excluded from taxable wages.

Author: Melissa Grant;

Source: blaverry.com

Types of Employer Reimbursement Arrangements

QSEHRA makes sense for businesses with 2-49 employees looking for straightforward, budget-controlled benefits. The 2026 caps—$6,350 individual, $12,800 family—adjust annually for inflation. You can't run QSEHRA alongside a group plan; it's one or the other.

One manufacturing company with 23 employees tried QSEHRA at $300 monthly in 2023. Participation was weak—only 35% of employees bothered, because individual plans in their area averaged $475. They bumped the allowance to $400 and saw participation jump to 82%. The lesson? Low-ball your contribution and employees treat it like a hassle, not a benefit.

ICHRA suits employers wanting flexibility without federal limits. A tech startup might designate $800 monthly for full-time developers and $400 for part-time support staff. A retailer with stores in multiple states could offer $900 in high-cost areas like Boston and $600 where insurance runs cheaper. You can even offer ICHRA to some employee groups while maintaining a group plan for others, provided the groups are distinct.

Excepted benefit HRAs handle limited expenses—dental, vision, or short-term insurance premiums. The 2026 cap is $2,150 annually. This arrangement supplements rather than replaces major medical coverage and requires that you already offer a group plan.

Tax Treatment for Employers and Employees

Get the structure right and everyone wins at tax time. Employees receiving QSEHRA or ICHRA reimbursements pay zero federal income tax, Social Security tax, or Medicare tax on those funds—as long as they maintain minimum essential coverage throughout the year.

You deduct reimbursements as ordinary business expenses, identical to how you'd deduct group insurance premiums. No payroll taxes hit these reimbursements either, which means real savings compared to simply raising salaries by the same amount.

There's one major catch: premium tax credits through the Marketplace. Say an employee qualifies for $450 monthly in tax credits. You offer $350 through ICHRA. The Marketplace will reduce their credit to roughly $100 because your contribution counts toward their coverage affordability. Some employees—especially lower earners with large subsidies—might actually fare better by declining your reimbursement arrangement and keeping their full tax credit.

This requires careful calculation. An employee making $35,000 might receive $550 monthly in Marketplace subsidies. If your $400 ICHRA allowance drops their subsidy to $150, they've lost ground financially. They can opt out of ICHRA to preserve the bigger subsidy, but they must actively decline—and that decision locks them out of ICHRA for the entire plan year.

What we're seeing is a fundamental rethinking of small-business benefits. Companies that felt priced out of offering health coverage now have a structured way to contribute meaningfully while controlling costs in ways group insurance never allowed

— Rebecca Hahn

Who Is Eligible for Employer Reimbursement?

Eligibility rules differ significantly between QSEHRA and ICHRA, though both share one requirement: participants must maintain minimum essential coverage. You can't just collect reimbursement money without buying insurance.

For QSEHRA, eligibility is straightforward. Any employee who's worked for you at least 90 days qualifies. You can exclude certain groups: workers under age 25, part-time and seasonal workers, union members with collectively bargained coverage, and some nonresident aliens. But once someone meets your participation criteria, you must offer identical allowances to all employees in that category.

A landscaping company with 30 employees might exclude seasonal workers who only work six months yearly. The remaining 22 full-time, year-round employees must all receive the same QSEHRA allowance. You can't offer your office manager $500 and your crew leaders $350—that's discrimination.

ICHRA introduces employee classes, dramatically expanding your options. You can establish separate allowances for:

- Full-time employees (30+ hours weekly) versus part-time workers

- Seasonal employees working less than full year

- Workers in different rating areas (the geographic regions insurance companies use for pricing)

- Salaried versus hourly staff

- Employees covered under collective bargaining agreements

- New hires during their waiting period (up to 90 days)

- Employees in different business divisions or locations

Each class gets uniform treatment—you can't arbitrarily favor individuals within a class. But between classes? You've got flexibility.

A software company with offices in San Francisco, Austin, and Miami structures ICHRA this way: $850 monthly for San Francisco full-timers, $650 for Austin full-timers, $600 for Miami full-timers, and $400 for part-time employees regardless of location. This acknowledges both cost-of-living differences and full-time versus part-time status. Perfectly legal.

Author: Melissa Grant;

Source: blaverry.com

Independent contractors and business owners typically can't participate. The IRS views HRAs as employee benefits, so 1099 contractors don't qualify. S-corporation owners holding 2% or more ownership face similar restrictions—the tax code treats them differently for benefits purposes.

How Much Does Employer Reimbursement Cost?

Your costs depend entirely on what you choose to contribute, how many employees participate, and whether you pay for third-party administration. Unlike group insurance where carriers dictate premiums, you control spending precisely.

QSEHRA maximums for 2026: - Individual coverage: $6,350 annually ($529 monthly) - Family coverage: $12,800 annually ($1,067 monthly)

You don't have to hit these ceilings. Many employers start at $300-400 monthly to test the waters before committing to larger amounts. The beauty here? Absolute budget predictability. Decide on $450 monthly for 18 employees and your maximum annual cost is $97,200, regardless of claims experience, medical inflation, or premium increases in the individual market.

ICHRA eliminates federal contribution caps entirely. You could theoretically offer $3,000 monthly per employee if your budget allows. Real-world employers typically benchmark against what they'd spend on group coverage—often setting allowances at 60-80% of comparable group plan costs.

Here's the comparison between QSEHRA and ICHRA:

| Feature | QSEHRA (2026) | ICHRA (2026) |

| Annual maximum (individual) | $6,350 | Unlimited |

| Annual maximum (family) | $12,800 | Unlimited |

| Company size requirement | Under 50 full-time employees | Any size company |

| Can you offer a group plan too? | No—it's one or the other | Yes—to different classes |

| How much can you vary allowances? | Only by family status | Extensive—by job type, location, more |

Administration adds to your costs. Third-party platforms handling compliance, substantiation, and employee support typically charge $5-15 per employee monthly. Some small employers self-administer QSEHRA to avoid these fees, though you're taking on compliance risk and eating up internal time.

Contribution strategy impacts perceived value significantly. An accounting firm initially offered $225 monthly QSEHRA, trying to be conservative. Employees in their mid-forties were paying $500-600 for decent individual coverage, meaning they still had significant out-of-pocket costs. Participation plateaued at 47%. After increasing to $475 monthly, participation climbed to 89% and employee satisfaction scores jumped notably. Employees viewed the benefit as genuinely helpful rather than a token gesture.

Coverage Periods and Important Deadlines

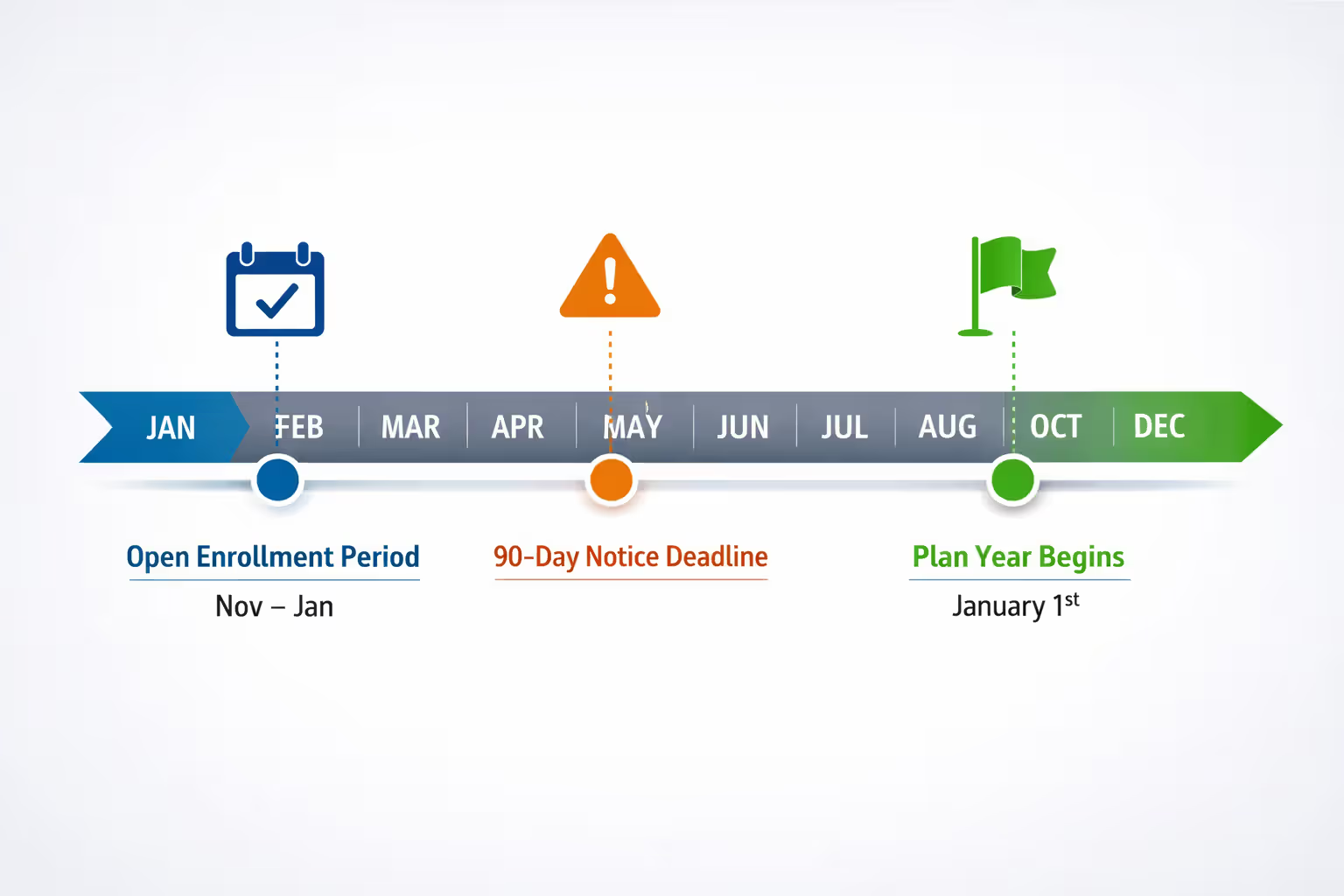

Reimbursement arrangements run on plan years—usually the calendar year, though any 12-month period works. You're required to provide written notice at least 90 days before the plan year starts, detailing allowance amounts, substantiation requirements, and how your arrangement affects Marketplace tax credits.

New hires get notice within 90 days of eligibility or before their start date—whichever comes first. This isn't a suggestion; it's a legal requirement. Skip it and you risk compliance issues plus potential delays in when employees can start receiving reimbursements.

Individual insurance enrollment windows don't always cooperate with your plan year timing. The Marketplace runs its main open enrollment from November 1 through January 15, with coverage starting January 1. Employees missing this window need a qualifying life event—marriage, childbirth, loss of other coverage—to enroll mid-year.

Smart timing matters. A company launching ICHRA on July 1 creates immediate complications: employees with April policy renewals must wait three months to participate, while those with July renewals can jump in immediately. January 1 launches sync perfectly with Marketplace enrollment and avoid this problem.

Author: Melissa Grant;

Source: blaverry.com

Claim deadlines vary by your plan design. Most employers require substantiation within 90 days of the expense, though some allow longer timeframes. Employees who procrastinate risk missing deadlines and forfeiting that month's reimbursement.

You need to specify acceptable documentation clearly. An insurance card proves coverage exists but doesn't prove payment. A billing statement showing the premium amount works. A bank statement highlighting the payment to the insurance carrier works. A screenshot of an online payment confirmation might work if you explicitly approve that format. Specify exactly what you'll accept upfront to avoid disputes later.

Unused allowances typically disappear unless your plan specifically allows rollover. An employee with $600 monthly allowance who only spends $475 on premiums forfeits the remaining $125 at month-end unless you've designed your plan to reimburse other qualified medical expenses like copays, prescriptions, or dental bills.

Employer Reimbursement vs Marketplace Health Insurance

This isn't an either-or choice—they work together. Employer reimbursement provides funding while Marketplace insurance (or other individual coverage) provides actual health benefits. The real comparison is employer-funded individual coverage versus traditional group plans.

How group insurance operates: The employer pools employees under one master policy, negotiates with carriers, manages enrollment, and typically covers 50-80% of premiums. Employees choose from a handful of plan options the employer pre-selected. Change jobs mid-year? You're changing insurance mid-year, which means new deductibles, possibly new doctors, and definitely new member ID cards.

Employer reimbursement flips this model. Employees browse dozens or hundreds of plan options and select coverage matching their specific needs. The employer provides a fixed monthly allowance regardless of which plan the employee picks. Change jobs? Your insurance stays with you because you own the policy directly.

Cost structures work differently. Group plans hit you with unpredictable renewal increases—frequently 8-15% annually, sometimes more. You're budgeting $850 per employee and suddenly facing $975 next year with 60 days' notice. Reimbursement arrangements let you increase contributions only when you decide to. Lock in $700 monthly and that's your cost for the entire plan year, regardless of individual market premium fluctuations.

For employees, the math varies widely by age and health status. A healthy 28-year-old might find a $325 monthly Marketplace plan that, combined with a $450 ICHRA allowance, leaves them pocketing $125 monthly. A 58-year-old managing diabetes might face $850 for adequate individual coverage, making that same $450 allowance less impressive.

Flexibility cuts both ways. Group plans lock employees into the employer's chosen networks and carriers. Love your current pulmonologist? Too bad if they're out-of-network under the new group plan your boss selected. Individual coverage purchased with reimbursement funds stays with you through job changes, creating true portability that group insurance can't match.

The downside: individual insurance in the non-Marketplace space sometimes uses medical underwriting, and even Marketplace plans vary premiums substantially by age. A 60-year-old pays roughly three times what a 21-year-old pays for identical coverage. Older employees often prefer group coverage's age-adjusted premiums, where everyone pays closer to the same amount.

| Factor | Employer Reimbursement (QSEHRA/ICHRA) | Marketplace Plans (Without Employer Contribution) |

| How it works | Employer provides monthly allowance; employee purchases individual policy | Employee purchases coverage independently; may qualify for income-based subsidies |

| Who selects the plan | Employee chooses from all available options in their area | Employee chooses from Marketplace-certified plans |

| Cost structure | Fixed employer contribution plus whatever employee pays | Employee covers full premium minus any tax credit |

| Tax benefits | Reimbursement is tax-free if employee maintains coverage | Premium tax credits reduce monthly costs |

| Coverage portability | Stays with employee through job changes | Stays with employee—no employer connection |

| Best fit for | Employees wanting choice plus employer funding | Self-employed individuals or those between jobs |

Premium tax credit coordination creates the biggest complexity. Marketplace subsidies phase out as household income rises. An employee earning $48,000 might qualify for a $225 monthly tax credit. If you offer a $425 ICHRA allowance, that tax credit drops to nearly zero. They're still better off by $200 monthly, but the benefit isn't as large as $425 plus $225.

Employees must report their ICHRA allowance when applying for Marketplace coverage. Fail to do this and they'll receive excess tax credits all year, then face a surprise repayment bill—sometimes several thousand dollars—when filing their tax return. The Marketplace doesn't automatically know about ICHRA offers; employees must disclose them.

Common Mistakes to Avoid with Employer Reimbursement

Running informal stipends instead of compliant HRAs. Some employers add "health insurance stipends" to paychecks without establishing proper QSEHRA or ICHRA documentation. This creates taxable income for employees and potentially violates ACA market reforms prohibiting employer payment plans that reimburse individual insurance outside compliant structures. The penalty: $100 per day per affected employee—$36,500 annually per person. For a 20-employee company, that's over $700,000 yearly in potential penalties.

Weak substantiation procedures. Accepting employees' verbal assurance that they have coverage, without reviewing actual documentation, fails IRS requirements. During audits, you lose tax deductions and employees face back taxes plus interest on previously excluded reimbursements. Establish clear procedures: employees submit insurance cards and billing statements, someone reviews them carefully, and records stay on file for seven years minimum.

Missing the 90-day notice requirement. This deadline isn't flexible. Employers who notify employees in mid-December about a January 1 QSEHRA start violate the rule. Consequences include potential penalties and employees lacking adequate time to shop for coverage during open enrollment.

Violating employee class rules in ICHRA. Offering $550 to some full-time employees and $750 to others within the same class, without a permissible reason like geographic location, breaks nondiscrimination rules. The IRS can disqualify your entire arrangement, making all reimbursements taxable retroactively. An architecture firm made this error by offering higher allowances to senior staff—which isn't a permissible class distinction. Their fix required creating separate classes for different office locations, then applying geographic-based allowances consistently.

Poor communication about Marketplace subsidies. Employees need crystal-clear guidance on how reimbursement affects their tax credits. A retail company's employee declined a $475 ICHRA because she thought her $350 Marketplace tax credit was better value. Nobody explained that the ICHRA would have saved her $125 monthly even after losing the credit. She left money on the table all year due to confusion.

Author: Melissa Grant;

Source: blaverry.com

Allowing reimbursement without verified coverage. An employee who drops insurance but continues receiving reimbursements is receiving taxable income. You must verify ongoing coverage—typically by requiring quarterly substantiation rather than only checking once at enrollment. One construction company discovered during a benefits audit that three employees had dropped coverage six months earlier but kept receiving reimbursements. The cleanup involved amended tax forms, back taxes, and penalties.

Frequently Asked Questions

Employer reimbursement for health insurance premiums fundamentally changes how small and mid-sized companies provide health benefits. Instead of battling group insurance renewals and forcing everyone into the same three plan options, employers establish a budget and employees choose coverage actually matching their needs.

The approach isn't perfect. Shopping for insurance overwhelms many employees—the options, terminology, and decision-making create analysis paralysis. Coordinating with premium tax credits introduces genuine complexity that requires math and planning. Employees with serious health conditions sometimes discover individual market options cost more than group coverage would have.

Yet for many businesses—particularly those with 10-75 employees—reimbursement arrangements solve genuine problems. Budget certainty becomes reality. Administrative burden drops dramatically compared to managing group enrollment. Employees get real choice instead of being told "take it or leave it."

A graphic design firm with employees scattered across five states can offer competitive benefits without negotiating multi-state group coverage. A growing startup can begin offering health benefits at 15 employees without committing to group insurance's complexity. A retail chain can differentiate allowances between different locations, acknowledging that insurance in Manhattan costs more than insurance in Oklahoma City.

Success requires serious communication investment. Employees need guidance on shopping for coverage, understanding what documentation to submit, and calculating how reimbursement affects their taxes. Employers investing in education—through benefits advisors, online tools, or detailed explanatory sessions—consistently see higher participation and satisfaction.

Whether you're an employer evaluating benefit options or an employee trying to understand your reimbursement offer, look at the complete picture: contribution amount, plan availability in your area, your anticipated healthcare needs, and tax implications. Employer reimbursement isn't inherently superior or inferior to group insurance—it's a fundamentally different model that excels in specific circumstances.

For the right company with the right employees, it transforms health benefits from an expensive headache into a manageable, appreciated part of the compensation package. That's worth considering carefully.