Business owner reviewing employee health insurance documents in a modern office with diverse team members nearby

When Does an Employer Have to Offer Health Insurance

Content

Back in 2010, the Affordable Care Act flipped the script on workplace health benefits. Now, certain employers don't just have the option to provide insurance—they're legally required to do it. The rules hinge on how many people you employ and how many hours they work.

Both business owners and workers need to understand these regulations. If you're running a company, you'll want to avoid costly penalties. If you're an employee, you should know exactly when you're entitled to coverage.

Employer Size and the ACA Mandate

Here's the magic number: 50. Once your business averages 50 or more full-time equivalent workers over a calendar year, the IRS considers you an Applicable Large Employer. And that designation brings serious obligations.

What counts as an Applicable Large Employer? Think of it this way—the IRS looks back at the previous year and calculates your average workforce. If that average hits 50 or higher, you've crossed into ALE territory. At that point, the employer shared responsibility rules apply to you.

Counting workers gets surprisingly complicated. Someone clocking 30+ hours weekly counts as one full-time employee. But what about part-timers? You'll need to add up all their monthly hours and divide by 120. That gives you how many full-time equivalents they represent.

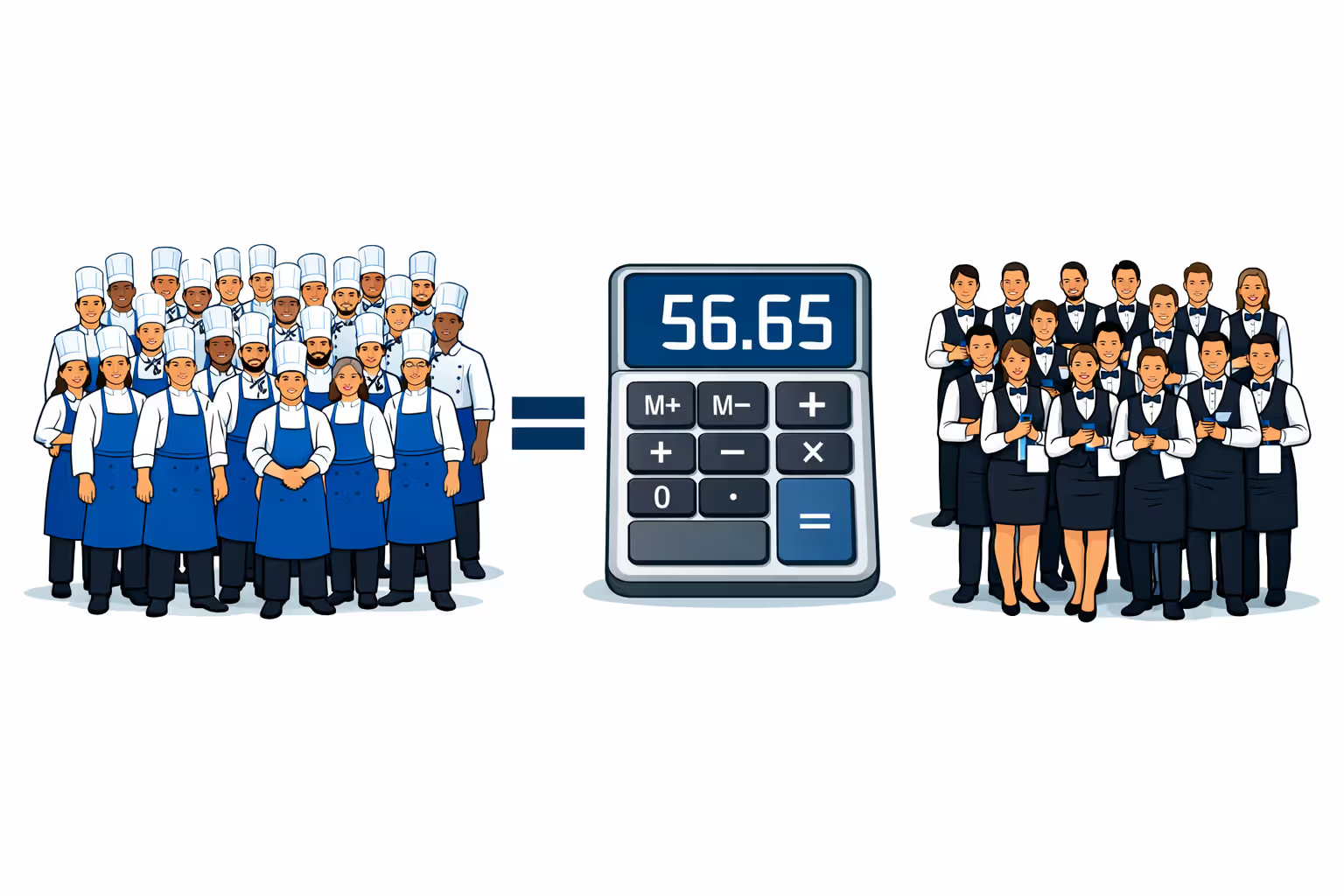

Let's walk through a real scenario. Imagine you run a busy restaurant. You've got 35 salaried managers and line cooks putting in 35+ hours every week. You also employ 30 servers who average about 20 hours weekly. Here's the math on those servers: multiply 30 workers by 20 hours by 4.33 weeks, then divide the whole thing by 120. That equals 21.65 FTEs. Add that to your 35 full-timers, and you're at 56.65 total FTEs. Congratulations—you're officially an ALE.

Businesses teetering around 49 or 50 employees? You'll want to run these calculations every single month. And here's some good news: if seasonal help pushes you over 50 FTEs, but only for 120 days or less in a year, the IRS gives you a pass.

What if you've got 49 employees? You're off the hook. No federal penalties exist for smaller companies that choose not to offer health benefits. That said, offering insurance still helps you compete for talented workers.

Author: Ethan Bradford;

Source: blaverry.com

Employee Eligibility Requirements for Coverage

Once you've hit ALE status, the law requires you to offer insurance to full-time workers and their kids (up to age 26). The government defines full-time as 30 hours per week, regardless of what you call the position internally.

You've got two ways to track who qualifies:

Monthly measurement: Each month, you count the hours every person worked. Anyone hitting 130+ hours (basically 30 hours weekly) qualifies as full-time for that period.

Look-back measurement: This works better when schedules bounce around. You pick a period—usually between 3 and 12 months—and calculate average hours. Someone averaging 30+ hours during that window earns coverage for the entire next stability period, even if their hours occasionally drop.

Picture a big-box retailer using a 12-month look-back for cashiers whose hours swing wildly between holidays and slow seasons. An associate averaging 32 hours during the measurement period gets a full year of coverage. Even if business slows and their schedule shrinks to 25 hours some weeks, they keep their insurance.

New hires create special situations. If you can't predict someone's hours at hiring, you're allowed an initial measurement period lasting up to 12 months. But here's the catch—if someone's obviously hired for full-time work, they need a coverage offer within the standard waiting period.

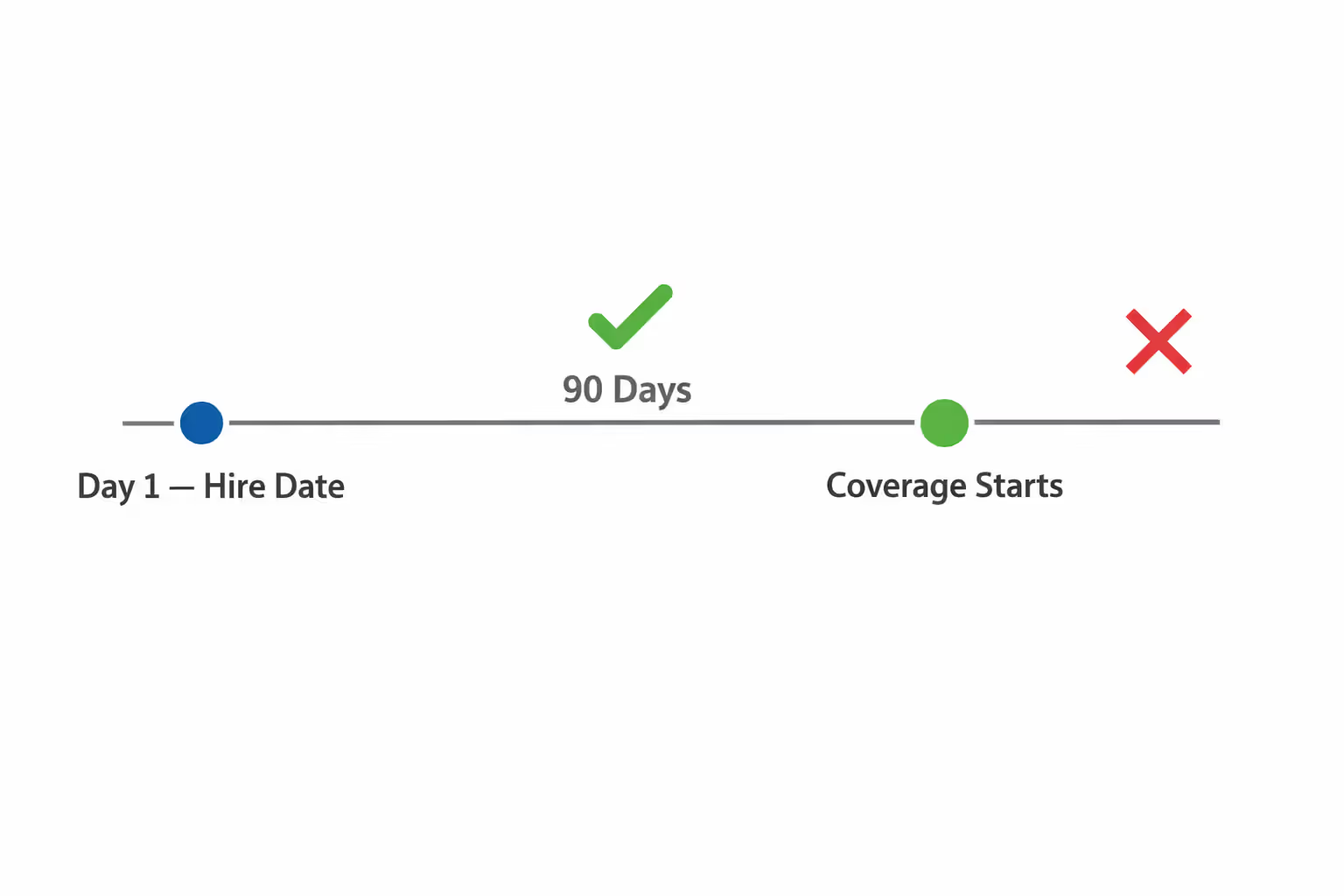

Maximum Waiting Periods Before Coverage Starts

Federal rules cap waiting periods at 90 days. You can't make someone work four months before they're eligible for insurance. You can offer it immediately or anywhere within those three months—but not longer.

That 90-day countdown begins on day one of employment. Not after orientation week. Not when probation ends. From the hire date.

Here's what you can do:

- Wait 90 calendar days

- Start coverage the first day of the month after 90 days

- Begin coverage the first day of the pay period after 90 days

Here's what you can't do: require a six-month performance evaluation before someone gets insurance access. That violates the 90-day rule. I've seen employers make this mistake—they think a probationary period resets the clock. It doesn't.

Author: Ethan Bradford;

Source: blaverry.com

What Coverage Must Employers Offer

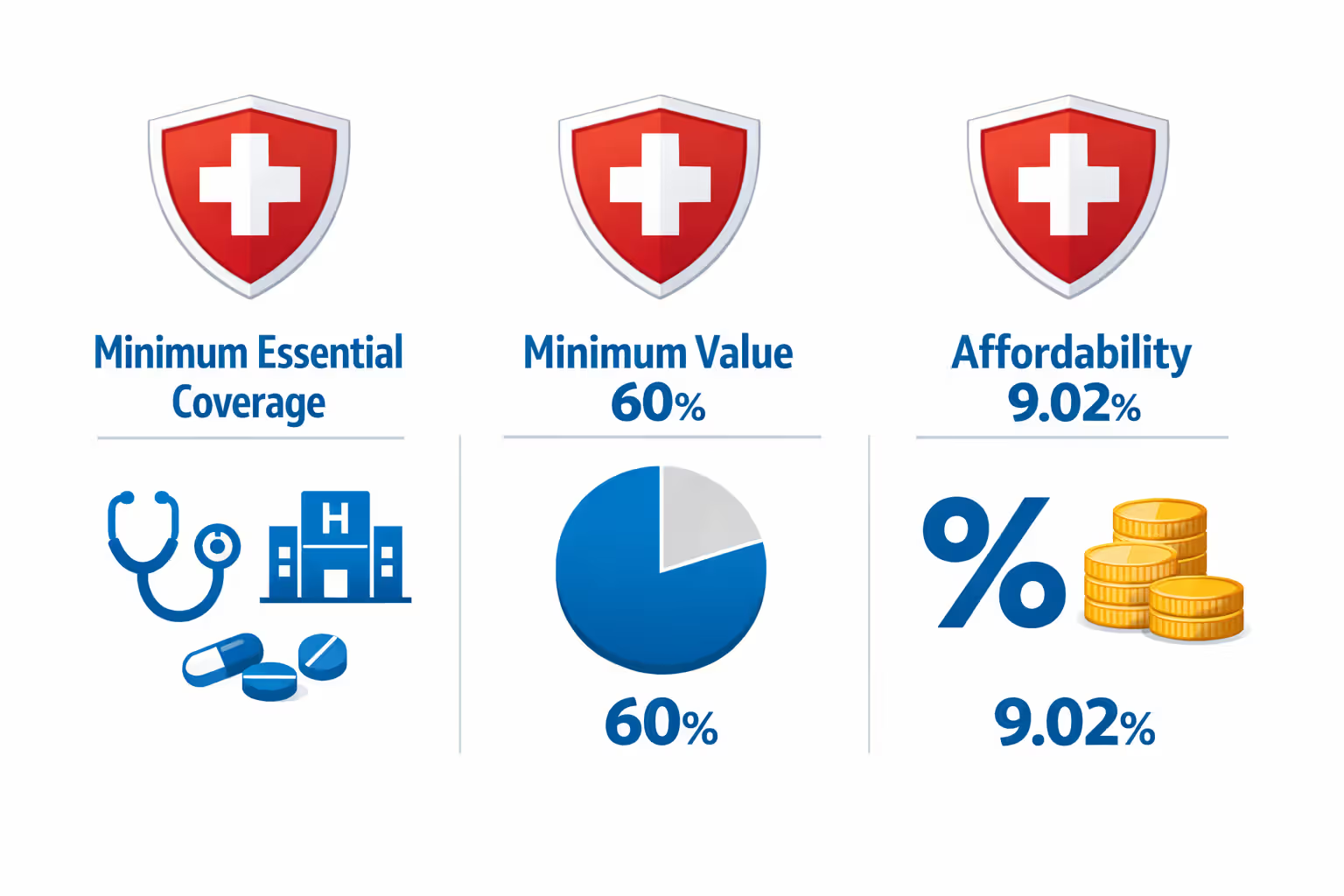

ALEs can't just offer any insurance plan and call it compliant. The coverage must check three boxes: it needs to be minimum essential coverage, meet minimum value requirements, and stay affordable for workers.

Minimum essential coverage means real health insurance. We're talking doctor visits, hospital stays, emergency room trips, prescriptions, and preventive care. Those limited plans covering only dental work or vision? They don't count. Accident-only policies? Nope.

Minimum value is an actuarial calculation. Your plan must cover at least 60% of total healthcare costs for a typical population. Most bronze-level marketplace plans hit this target. Silver, gold, and platinum plans exceed it. The IRS offers a calculator to determine if your plan passes, or your insurance carrier can certify it.

Affordability gets technical. Employee-only premiums can't exceed 9.02% of household income in 2026 (this percentage adjusts yearly). Of course, you probably don't know what your employees' spouses earn. That's why the IRS created three safe harbors:

- W-2 safe harbor: The premium stays under 9.02% of Box 1 wages on the employee's W-2

- Rate of pay safe harbor: For hourly workers, the premium doesn't exceed 9.02% of 130 hours times their hourly rate

- Federal poverty line safe harbor: The premium stays under 9.02% of the federal poverty line for a single person

Say you run a factory paying $15 hourly. Using the rate-of-pay safe harbor, you could charge up to $176.29 monthly for employee-only coverage. That's $15 times 130 hours times 0.0902.

You must offer coverage to employees' children under 26. Spousal coverage? That's optional. Here's a frustrating quirk: affordability only measures employee-only premiums. Family coverage can cost whatever. I've seen situations where employee-only coverage runs $150 monthly (affordable), but adding three kids jumps it to $850 (potentially crushing for someone earning $35,000 annually).

Author: Ethan Bradford;

Source: blaverry.com

Enrollment Deadlines and Coverage Start Dates

Initial enrollment happens when workers first qualify. You're required to notify new hires about their coverage options within 14 days of their start date. Once eligible, employees typically get 30 days to complete enrollment.

When does coverage actually kick in? Most ALEs align effective dates with the first of the month following eligibility and completed enrollment. Someone hired January 5th completes their 90-day wait on April 5th. Coverage would typically start May 1st.

Annual open enrollment comes around once yearly—usually autumn for calendar-year plans. This window lets employees switch plans, add or drop dependents, or change their coverage level. Most companies run open enrollment for 2-4 weeks.

Qualifying life events create mid-year enrollment opportunities. Major changes like these trigger special enrollment:

- Getting married or divorced

- Having or adopting a baby

- Losing other insurance coverage

- Moving to a new state that affects plan availability

- Major income shifts

Workers must request these special enrollments within 30-60 days of the event (varies by plan). Someone getting married in June doesn't need to wait until November to add their new spouse.

Most employer plans run January through December, though some companies use fiscal year calendars instead. Plans must provide continuous coverage for at least 12 months before renewal.

Employer Coverage vs. Marketplace Insurance

When your employer offers qualifying coverage, you generally can't get subsidized marketplace insurance. This "firewall" prevents people from getting government subsidies when they already have access to employer coverage.

You can still buy marketplace coverage—you'll just pay full price. Why would someone do that?

- Their employer's network doesn't include their long-time doctor

- The marketplace plan covers their medications better

- They prefer different deductibles or copays

- Individual coverage through work is affordable, but family coverage costs a fortune

The subsidy block only applies when employer coverage is "adequate and affordable." If employee-only premiums exceed 9.02% of household income, the coverage fails affordability. At that point, you could qualify for marketplace tax credits.

Consider a retail worker earning $28,000 annually. Their employer charges $250 monthly for individual coverage. That's $3,000 per year—10.7% of income. Since that exceeds 9.02%, the coverage is officially unaffordable. This worker could pursue subsidized marketplace coverage instead.

The overlap between employer coverage and marketplace subsidies confuses countless workers. Grasping affordability calculations empowers employees to make smart coverage choices, especially when family coverage costs spiral out of control

— Sarah Mitchell

The family coverage gap causes real problems. Remember—affordability calculations only examine employee-only premiums. An employer might charge $150 monthly for solo coverage (affordable) but $900 for a family plan. Even though that family plan might eat up 20% of a lower-wage worker's income, they still can't access marketplace subsidies. The employee-only premium passed the affordability test, which is all the law considers.

Penalties for Non-Compliance

ALEs that don't offer coverage to at least 95% of full-time workers and their dependents face the Section 4980H(a) penalty. People call this the "sledgehammer penalty" for good reason. In 2026, it's $2,970 per year for each full-time employee, minus the first 30.

Imagine a company with 80 full-time employees that offers zero coverage. Their penalty: 50 employees (80 minus 30) times $2,970. That's $148,500 annually.

Section 4980H(b) kicks in when you offer coverage, but it fails affordability or minimum value requirements—and at least one worker gets subsidized marketplace insurance. This "tack-hammer penalty" runs $4,460 annually per employee who received that subsidy.

The IRS discovers these situations through marketplace data sharing. Employees who got subsidies get reported to the IRS, which then cross-references employer information. You'll receive Letter 226J showing proposed penalties. You've got 30 days to respond with documentation proving you were compliant.

Penalties calculate monthly, then total up for the year. Offer coverage for only half the year? You'll pay half-year penalties for the months without compliant coverage.

Author: Ethan Bradford;

Source: blaverry.com

Common Employer Health Insurance Mistakes

Misclassifying employees as part-time: Calling someone part-time doesn't make them part-time. The IRS cares about actual hours worked, not job titles. I've seen employers label workers "part-time" while scheduling them 35 hours weekly. That doesn't fly.

Incorrect FTE calculations: Some companies forget to include part-time hours when counting FTEs. Others miscalculate seasonal worker exceptions. Discovering you were actually an ALE after the year ends creates retroactive penalty exposure running into six figures.

Inadequate coverage offerings: Assuming any health plan satisfies the mandate is dangerous. Plans must genuinely meet minimum value standards and affordability thresholds. Some employers offer bare-bones coverage thinking they're protected. The IRS disagrees—emphatically.

Missing reporting deadlines: ALEs file Forms 1094-C and 1095-C annually. These forms report coverage offers and enrollment to the IRS while providing statements to employees. For 2026, employee statements are due March 2, 2027. IRS filing is due March 31, 2027, if filing electronically. Miss these deadlines? Separate penalties of $60 to $310 per form stack up fast.

Extending waiting periods beyond 90 days: Requiring probationary periods, waiting for performance reviews, or mandating seasonal completion before coverage access can accidentally create waiting periods exceeding 90 days. Each of these violations risks penalties.

Failing to offer dependent coverage: Spousal coverage is your choice. But children under 26? Required. Some employers mistakenly cap dependent coverage at age 18 or limit it to full-time students.

Ignoring variable-hour workers: Restaurants, retail chains, and seasonal operations sometimes exclude variable-hour employees from tracking. Apply measurement periods correctly, and you'll often find these workers qualify for coverage.

Employer Health Insurance Requirements by Company Size

| Number of Employees | ACA Mandate Status | Penalty Risk | Reporting Requirements |

| 1-49 FTEs | Exempt from mandate | No federal penalties apply | No ACA reporting required (Forms 1094-C/1095-C don't apply) |

| 50-99 FTEs | Mandate applies (ALE status) | Yes—penalties apply if coverage not offered or fails requirements | Annual filing of Forms 1094-C and 1095-C required |

| 100+ FTEs | Mandate applies (ALE status) | Yes—penalties apply if coverage not offered or fails requirements | Annual filing of Forms 1094-C and 1095-C required; IRS scrutiny increases with company size |

Frequently Asked Questions

The employer health insurance mandate targets companies with 50 or more full-time equivalent employees. These businesses must offer affordable coverage meeting minimum value standards to full-time workers within 90 days of eligibility. The 30-hour weekly threshold separates full-time from part-time status. Non-compliance penalties can hit thousands of dollars per employee each year.

Companies approaching the 50-employee mark should carefully monitor workforce composition and hours. Employees should understand their qualification criteria and how employer offers impact marketplace subsidy eligibility. The relationship between employer coverage and marketplace options creates complexity—particularly around family coverage costs.

Accurate FTE calculations, correct employee hour classification, timely coverage offers, and complete annual reporting protect employers from penalties. For employees, understanding these rights ensures you receive entitled coverage or pursue alternatives when employer options prove inadequate or unaffordable.

Whether you're structuring a compliant benefits program as an employer or evaluating coverage choices as an employee, these requirements shape your health insurance decisions throughout 2026 and beyond