Office desk with health insurance document, stethoscope, calculator, pen, laptop, and small figurines representing employees

Do Employers Have to Offer Health Insurance?

Content

The short answer? It depends on how many people work there. Big companies face strict rules about health coverage, while smaller businesses don't have the same legal obligations. Since the Affordable Care Act passed in 2010, businesses with 50+ full-time workers must follow specific requirements—or they'll face serious financial consequences. If you're trying to figure out whether your job should include health benefits, or you're running a business and wondering about your obligations, here's what actually matters.

When Employers Must Provide Health Insurance

The ACA created what's officially called the "employer shared responsibility provision"—most people just call it the employer mandate. Here's how it works: companies that qualify as applicable large employers must offer health coverage to their full-time staff and dependents, or they'll owe money to the IRS.

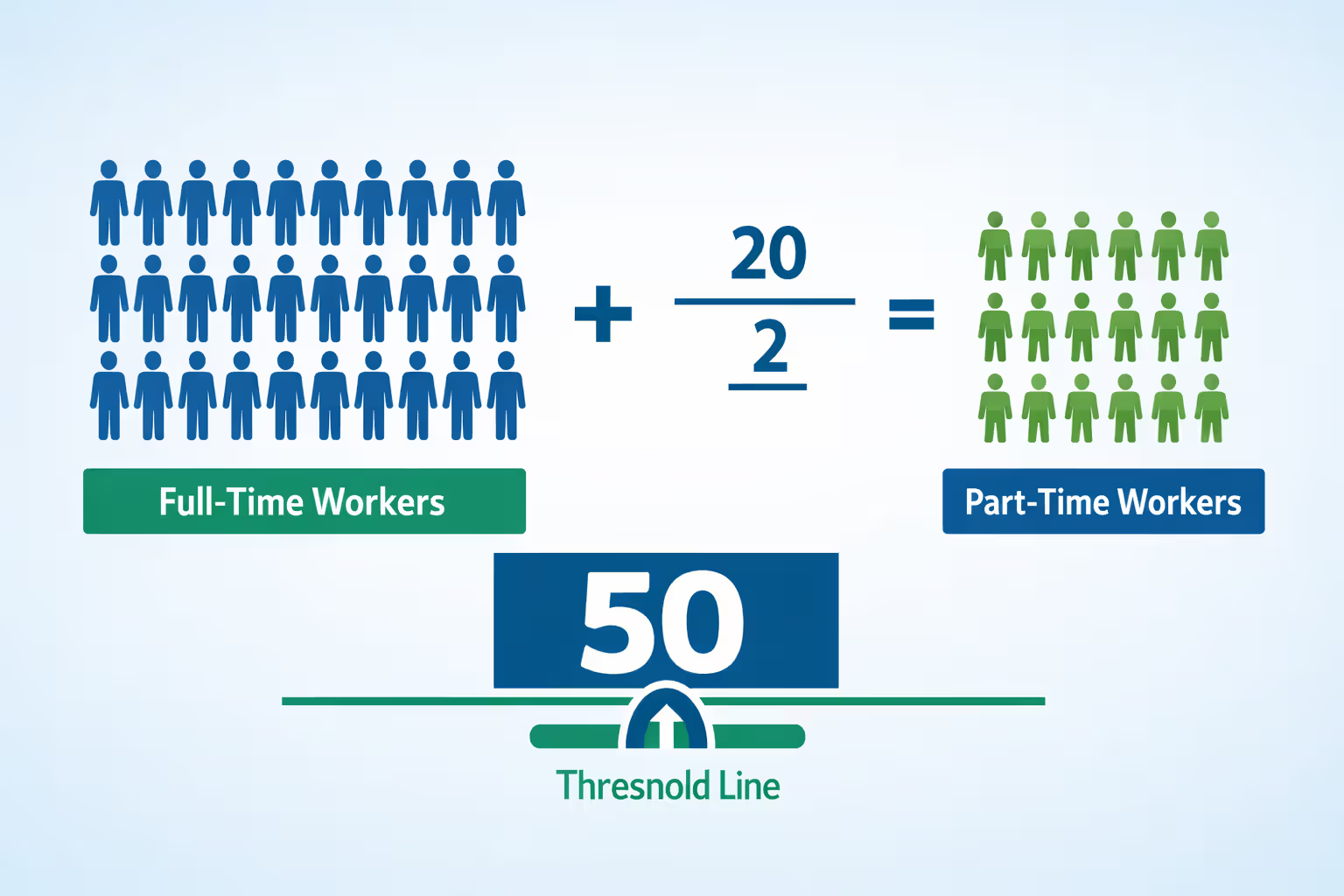

So who counts as an applicable large employer? Any business with at least 50 full-time equivalent employees during the previous calendar year. Calculating this number isn't always straightforward. You start by counting everyone who works 30+ hours weekly. Then you take all your part-time employees, add up their monthly hours, and divide by 120. That second number gets added to your full-time count.

Here's a real-world example: Say you run a retail chain with 40 people working full-time schedules and another 20 employees who each work about 60 hours monthly. Your FTE calculation looks like this: 40 full-timers + (1,200 total part-time hours ÷ 120) = 50 FTEs. You've just crossed the threshold, which means the mandate applies to you starting the next plan year.

Companies figure this out based on the prior year's numbers, then apply that status to the current year. One thing businesses can't do? Split themselves into multiple smaller companies to dodge the requirement. The IRS specifically looks at "controlled groups" and "affiliated service groups," counting all their workers together. If you own three restaurants with 20 employees each, you're still a 60-employee company in the government's eyes.

Author: Melissa Grant;

Source: blaverry.com

The mandate covers common-law employees only—that's people whose work you control and direct. Independent contractors don't count toward your threshold, no matter how many hours they log. Churches with official religious exemptions, certain tribal governments, and some public employers get carved out of these rules entirely, even if they're huge organizations.

Who Qualifies as a Full-Time Employee for Health Coverage

The ACA sets the bar at 30 hours per week on average, or 130 hours in a month. Notice that's different from what most companies traditionally called "full-time"—many businesses used 35 or 40 hours as their internal standard. For health insurance purposes, though, federal law drew the line at 30 hours, and that's what triggers an employer's coverage obligation.

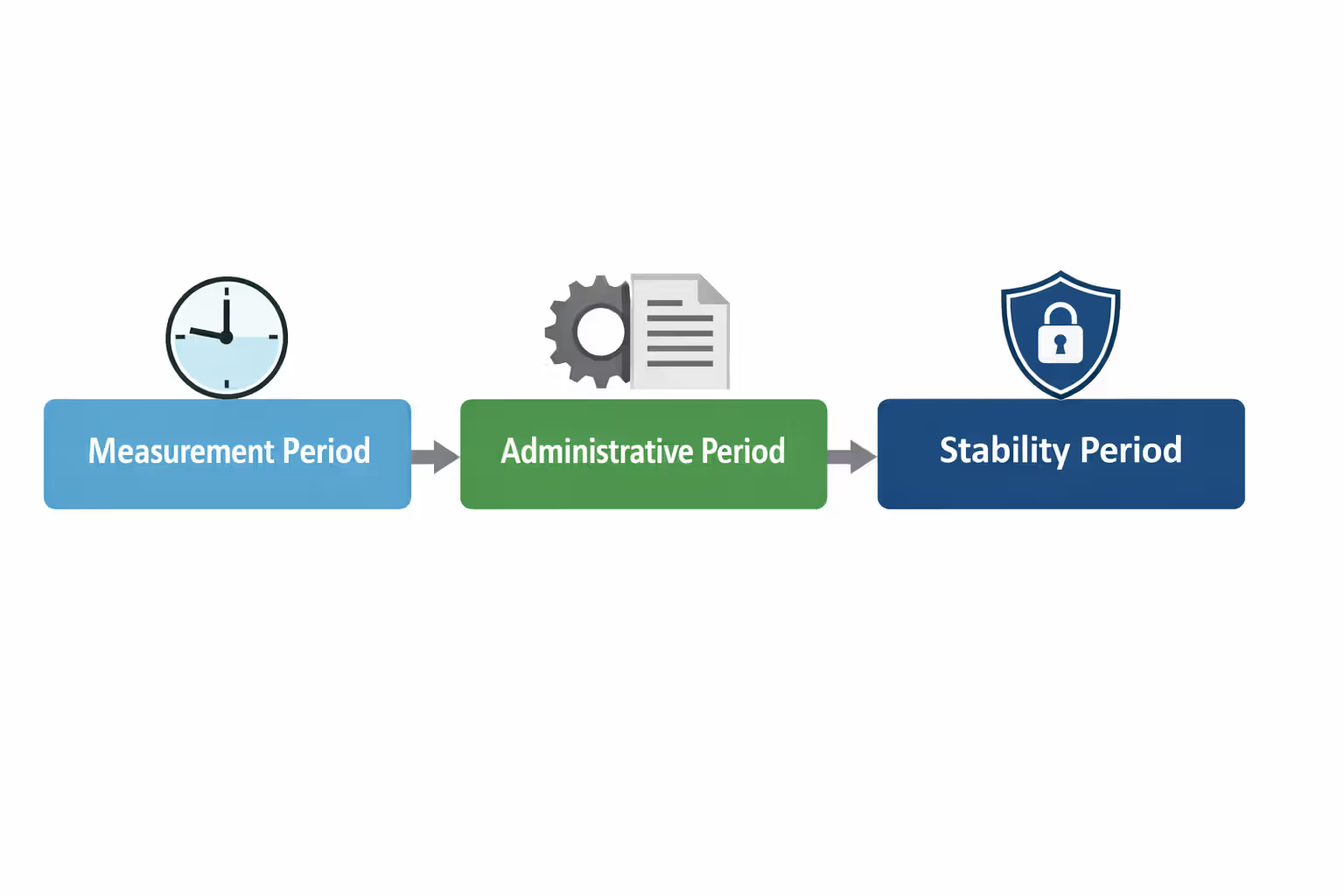

Tracking who crosses this threshold gets complicated when schedules vary. Employers can choose between two approaches: monthly measurement or look-back measurement.

Monthly measurement sounds simple—you check hours each month and adjust coverage eligibility right away. But this creates chaos for workers with inconsistent schedules. Someone might qualify one month, lose eligibility the next, then qualify again. Most large employers avoid this approach precisely because it's so unstable.

The look-back method works better for variable schedules. You pick a measurement period—usually between 3 and 12 months—and track hours during that window. Then you get an administrative period of up to 90 days to process enrollment paperwork. Finally, there's a stability period lasting 6 to 12 months where the employee's coverage status stays locked in, regardless of hour fluctuations. Someone who averaged 32 hours weekly during measurement gets coverage for the entire stability period, even if their hours drop to 20 in month three.

Author: Melissa Grant;

Source: blaverry.com

New hires create a separate challenge. If you can't reasonably predict whether someone will work full-time hours, you're allowed an initial measurement period stretching up to 12 months. But if it's obvious someone's being hired for a full-time role—say, you're bringing on a new department manager—coverage must be offered within three months (that's the maximum waiting period federal law allows).

Seasonal workers get special treatment. If someone works six months or fewer annually, you can exclude their off-season months from FTE calculations. But during their active work period, they need coverage offers if they're hitting 30+ hours weekly. This exception matters hugely for ski resorts, summer camps, tax preparation services, and agricultural businesses.

What Coverage Employers Must Offer

You can't just offer any health plan and call it done. The ACA established two key tests your coverage must pass: minimum essential coverage and minimum value. Plus, it needs to be affordable by the government's definition.

Minimum essential coverage means real major medical insurance—not dental-only plans, vision coverage, or those accident policies that pay out fixed amounts. Your plan needs to cover hospital stays (both inpatient and outpatient), doctor visits, lab work, preventive services, and prescription medications. Those limited-benefit plans companies sometimes offered years ago? They don't cut it anymore.

The minimum value standard requires your plan to pay at least 60% of total medical costs for covered benefits. That's an actuarial calculation, meaning insurance experts crunch the numbers to figure out what percentage the plan covers versus what employees pay through deductibles, copays, and coinsurance. A plan that looks generous but actually leaves employees paying 50% of costs would fail this test.

Affordability centers on what the employee pays for their own coverage—family coverage costs don't matter for this calculation. In 2026, employee-only premiums can't exceed 9.02% of the worker's household income. Since employers rarely know what someone's household earns, the IRS created three safe harbors. Most companies use the W-2 safe harbor, making sure premiums stay under 9.02% of what they paid that employee during the year.

Coverage must extend to dependents under 26, though employers aren't required to offer spousal coverage (many do anyway). The affordability test applies only to the employee's own premium—dependent coverage can cost whatever the employer decides, which creates situations where adding kids to the plan becomes financially impossible even though the employee's portion seems reasonable.

Plan years typically run January through December, though employers can choose different 12-month periods. Once you establish a plan year and start offering coverage, it must continue without gaps. Employees who say "no thanks" during initial enrollment generally can't change their minds until the next open enrollment period or after experiencing a qualifying life event like getting married or having a baby.

Penalties for Not Offering Health Insurance

Large employers that don't offer coverage to at least 95% of their full-time workers face what's called the Section 4980H(a) penalty. Tax attorneys sometimes call it the "sledgehammer" because it's so punishing. For 2026, we're talking $2,970 per full-time employee per year—though you subtract the first 30 employees from the penalty calculation.

Let's say you employ 100 full-time people and offer zero coverage. If even one employee goes to the marketplace and gets premium tax credits (subsidies), you'll owe penalties on 70 employees. That's $207,900 annually ($2,970 × 70). Notice how the penalty hits regardless of how many employees actually get subsidies—one person receiving help triggers the penalty based on your total headcount.

The Section 4980H(b) penalty works differently. This applies when you offer coverage but it fails the affordability or minimum value tests. Here you're looking at $4,460 per employee who ends up receiving marketplace subsidies. So if your coverage is too expensive and 10 employees go to the marketplace and qualify for help, you'd owe $44,600 for just those 10 workers.

We see employers all the time who think they're fine because they offer a health plan, but the plan requires employees to pay 12 or 15 percent of their salary for coverage.That's way over the affordability limit, which means every employee who gets marketplace subsidies instead generates a penalty of several thousand dollars

— Jennifer Martinez

The IRS discovers non-compliance by matching Form 1095-C (which employers must file) against individual tax returns showing premium tax credits. You'll eventually get Letter 226-J in the mail proposing penalties, with 30 days to respond and explain why you shouldn't owe the money. This often happens two or three years after the coverage year, creating nasty surprises for businesses that thought they'd escaped scrutiny.

One more painful detail: these penalties aren't tax-deductible. A $200,000 penalty costs you the entire $200,000—unlike regular business expenses that at least reduce your taxable income. The true cost of non-compliance exceeds the penalty's face value once you factor in that lack of deductibility.

Exceptions and Employers Not Required to Offer Coverage

Small businesses employing fewer than 50 full-time equivalent workers face zero federal mandate. They represent the vast majority of American employers—we're talking millions of small companies—and they can decide whether to offer benefits based purely on what makes business sense. Competition for talent, budget constraints, and employee expectations drive those decisions, not federal penalties. (Some states have created their own requirements, but that's separate from federal law.)

Grandfathered plans—meaning health coverage that existed on March 23, 2010 and has been maintained continuously without major changes—get exemptions from certain ACA requirements. But the employer mandate itself still applies if you're a large employer. Grandfathered status affects plan design rules like preventive coverage requirements, not whether you must offer insurance in the first place.

Author: Melissa Grant;

Source: blaverry.com

Churches and church-controlled organizations can claim religious exemptions by filing Form 8274. This exempts the organization from penalties, and it means employees can't get marketplace premium tax credits even if the church offers no coverage. The exemption reflects the constitutional separation between church and state.

Federal, state, and local government employers follow their own rules and don't face 4980H penalties. That doesn't mean they ignore health coverage—most government positions include benefits—but the penalty structure doesn't apply to them. Tribal governments received specific exemptions, though many tribes voluntarily provide coverage as part of their employment packages.

Businesses with predominantly part-time workforces might stay under the 50-FTE threshold despite having hundreds of workers on payroll. A restaurant group employing 200 people who each work 15 hours weekly would calculate FTEs like this: 200 employees × 15 hours = 3,000 weekly hours ÷ 30 hours per FTE = 100 FTEs. Wait—that's over 50, so the mandate applies. But if those same employees worked 12 hours weekly instead, you'd have 80 FTEs. A few hours per week can determine whether the mandate kicks in.

Staffing agencies and professional employer organizations complicate things. The IRS looks at who's the "common-law employer"—meaning who actually controls what work gets done and how. The company directing the work typically bears responsibility for the mandate, not the payroll processor. Trying to hide behind corporate structures doesn't work; the IRS examines the actual employment relationship.

Employer-Sponsored Insurance vs. Marketplace Plans

Author: Melissa Grant;

Source: blaverry.com

Workers with access to employer coverage that passes the affordability and minimum value tests can't get premium tax credits for marketplace plans. That makes employer insurance the only subsidized option for most people at large companies, even when marketplace plans might otherwise suit them better.

Cost differences swing wildly depending on circumstances. Employers generally cover 70-85% of premiums for employee-only coverage, leaving workers paying the rest. But family coverage? That's a different story. Employers don't have to contribute any specific amount toward dependents, so adding a spouse and kids might cost $800, $1,200, or more monthly. Marketplace plans could theoretically cost less after subsidies, except those subsidies evaporate when affordable employer coverage exists.

The affordability test creates what's called the "family glitch." If employee-only coverage costs $200 monthly and meets the 9.02% threshold, that person can't access marketplace subsidies—even if adding three kids costs an additional $900 monthly. The test looks only at the employee's own premium, ignoring the fact that family coverage might eat up 25% of household income. Millions of workers face this problem, and despite various legislative proposals, the glitch remains unfixed as of 2026.

Coverage quality typically favors employer plans. Group policies usually include broader provider networks, lower deductibles, and more comprehensive benefits compared to marketplace silver plans. Employer plans average somewhere between $1,500-$3,000 annual deductibles for individual coverage. Marketplace plans purchased without subsidies often carry $5,000-$8,000 deductibles or higher.

Workers can always decline employer coverage and buy marketplace plans instead—nobody forces you to take your employer's insurance. But you'll pay full price without subsidies unless the employer coverage fails the affordability or minimum value tests. Some people choose this route anyway when employer networks exclude their preferred doctors or when they'd rather have a high-deductible catastrophic plan paired with a health savings account.

| Feature | Employer-Sponsored Insurance | Marketplace Plans | Key Differences |

| What you pay monthly | Employer covers 70-85%; you pay 15-30% | You pay everything unless subsidies apply | Your portion usually costs less with employer coverage |

| Family coverage costs | Often expensive; employers can charge whatever they want | Might qualify for subsidies if employer plan costs too much | Marketplace sometimes wins for families due to subsidy rules |

| Subsidy availability | Never—employer coverage disqualifies you | Only when employer offers nothing or unaffordable/inadequate coverage | Having access to employer insurance blocks marketplace help |

| Doctor networks | Usually broad PPO or HMO networks | Depends on metal tier; bronze/silver often have narrow networks | Employer plans typically include more providers |

| Annual deductibles | Averages $1,500-$3,000 | $5,000-$8,000 common for unsubsidized plans | Employer plans usually require less out-of-pocket before coverage kicks in |

| When you can enroll | Annual open enrollment or after major life changes | Annual open enrollment or after qualifying events | Timing rules work similarly for both |

Switching from employer to marketplace coverage mid-year requires a qualifying event—simply preferring marketplace options doesn't count. You'll need to experience something like marriage, divorce, having a baby, or losing other coverage. Otherwise, you're waiting for annual open enrollment, which happens once yearly for each type of coverage.

Employee Rights and Enrollment Deadlines

Federal law caps waiting periods at 90 days from your hire date if you're eligible for coverage. Employers can offer insurance immediately or after 30 days—that's their choice—but 90 days is the absolute maximum. The clock starts ticking on your first day of work, not the first of the month or the start of a pay period.

Some employers tack on an orientation period of up to one month before the 90-day wait begins. That potentially extends your total wait to four months, though the orientation period must involve legitimate onboarding—not just a delay tactic to postpone coverage. Most employers stick with straightforward 60- or 90-day waiting periods to avoid compliance headaches.

Coverage takes effect on the first day of the month after your waiting period ends. If you're hired January 15 and there's a 60-day wait, you become eligible around March 16, meaning coverage starts April 1. Some employers simplify this by setting effective dates at the beginning of the month following 30, 60, or 90 days of employment, which creates clearer expectations.

Annual open enrollment runs for a few weeks each year—usually 2 to 4 weeks, depending on the employer. This is when you can enroll for the first time (if you initially declined), switch between plan options, add family members, or drop coverage entirely. Employers set their own open enrollment windows; many schedule them in November or December for January 1 effective dates. Miss this window and you're stuck with your current status until next year, unless something major happens in your life.

Those major happenings are called qualifying life events, and they open special enrollment periods lasting 30-60 days. Getting married, divorced, having or adopting a baby, losing other coverage, or moving to a new state all qualify. You've got 30 days to notify HR after the event occurs, and you'll need documentation—marriage certificates, birth certificates, or proof of lost coverage.

COBRA continuation coverage kicks in when you lose coverage due to job loss, reduced hours, or certain other qualifying events. You can keep your employer plan for 18-36 months (depending on the situation) by paying the full premium yourself, plus a 2% administrative fee. This costs way more than active employee coverage, but it maintains continuity and avoids gaps that might cause pre-existing condition issues when you eventually transition to new coverage.

Want to verify your employer coverage meets minimum value standards? Request the Summary of Benefits and Coverage (SBC) from HR. Employers must provide this standardized document at enrollment and annually afterward. It shows deductibles, out-of-pocket maximums, and coverage examples in easy-to-understand formats. If you're worried about affordability, calculate whether your premium exceeds 9.02% of your W-2 wages from that employer.

Form 1095-C provides official documentation of coverage offers and enrollment status. Employers must send this form by March 2 following the coverage year. You'll use it to complete your tax return and verify you had coverage throughout the year. If your Form 1095-C shows something different from what you remember, address the discrepancy with HR immediately—don't wait until tax season creates complications.

Frequently Asked Questions

Large employers employing 50 or more full-time equivalent workers must offer affordable, adequate health coverage to staff averaging 30+ weekly hours—that's the core of the employer mandate. Smaller businesses face no such federal requirement, though competitive pressure and state laws might influence their decisions. These rules matter whether you're an employee trying to understand your rights or an employer designing compliant benefit programs. Workers should verify their eligibility, confirm that coverage meets federal standards, and only explore marketplace alternatives when employer offerings fail affordability or adequacy tests. The complexity increases when you factor in marketplace subsidy rules, varying work schedules, and the interaction between employer contributions and family coverage costs—making it essential to understand how company size, hours worked, premium amounts, and plan quality all influence your health insurance options and obligations.