Family sitting at kitchen table reviewing health insurance documents on laptop with paperwork spread out

How Much Is Health Insurance Per Month

Content

Shopping for health insurance means confronting sticker shock. Most Americans buying their own coverage in 2025 will see individual marketplace plans ranging from $450 to $650 monthly before any financial help kicks in. Family plans? You're looking at $1,200 to $1,800 each month. If you get insurance through work, expect to chip in around $125 to $180 monthly for yourself alone—your employer handles the rest.

But here's where it gets interesting: these national averages tell only part of the story. A 25-year-old living in Austin might write a check for $320 monthly for a Silver-tier plan, while a 55-year-old in Casper, Wyoming could face $850 for nearly identical benefits. And if you qualify for income-based subsidies? That $575 premium could drop to $50. Or nothing at all.

The pricing puzzle depends on six major factors working together: your age, where you live, which plan tier you select, whether you use tobacco, how many family members need coverage, and your household income. We'll break down exactly how each piece affects your final bill.

Average Health Insurance Costs by Plan Type

Let's start with real numbers. What are people actually paying across different coverage categories?

| Coverage Type | Average Monthly Premium | Who Covers the Cost |

| Individual Marketplace (full price) | $575 | You pay everything |

| Family Marketplace (full price) | $1,650 | You pay everything |

| Employer Plan for Individual | $625 total ($145 from your paycheck) | You and employer split it |

| Employer Plan for Family | $1,950 total ($520 from your paycheck) | You and employer split it |

| Medicare Advantage | $18 (you still pay Part B at $185) | You pay both parts |

| Medicaid | $0–$15 | State programs cover most/all |

When you buy marketplace plans through healthcare.gov or your state's exchange, expect wide price swings. That healthy 30-year-old might snag a Bronze plan starting at $350, but want Platinum coverage with all the bells and whistles? You're paying north of $700. These numbers assume you earn too much for subsidies.

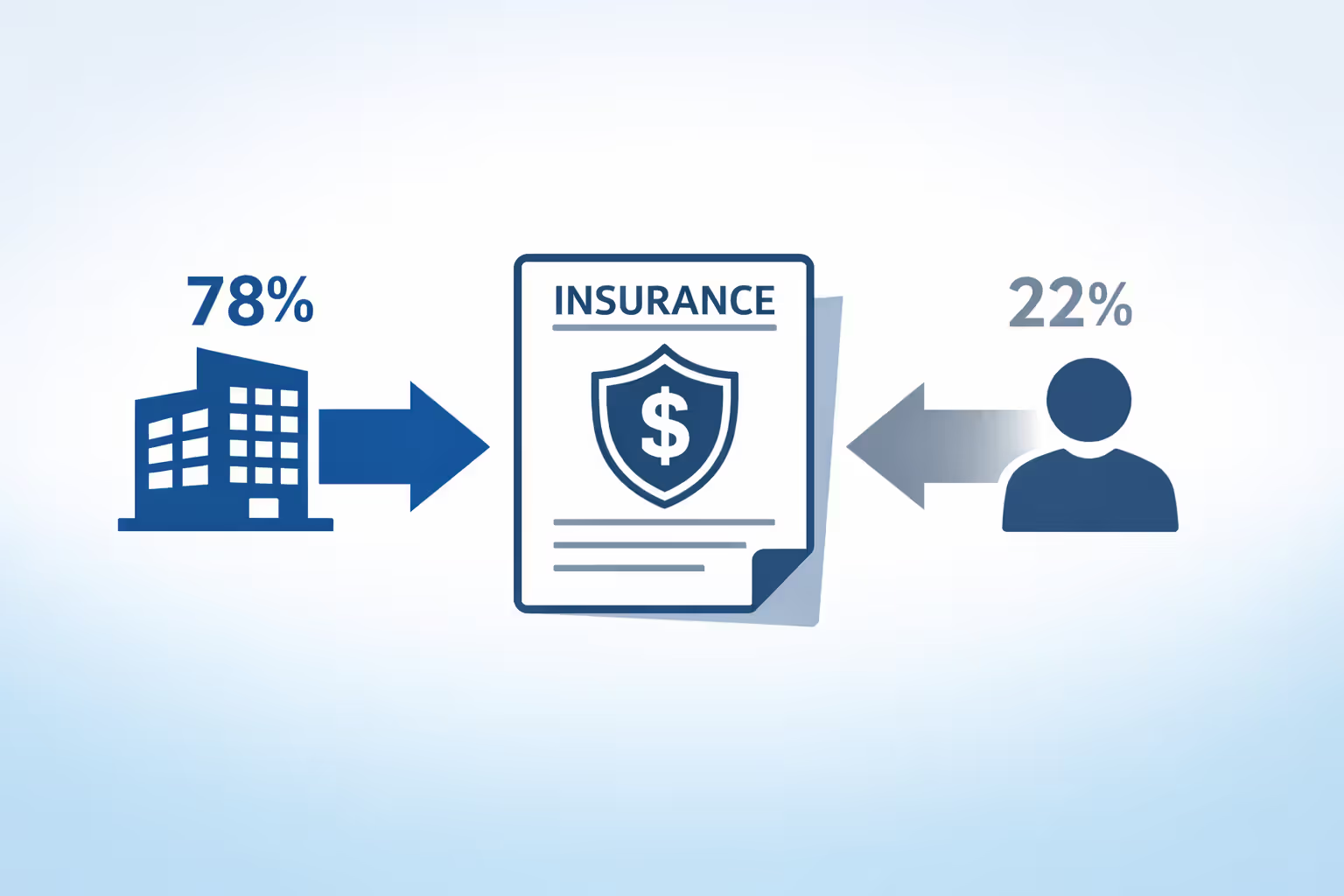

Employer coverage remains king for most working Americans—about 160 million people get insured this way. While the full cost of single coverage averages $625, most workers only see $145 leaving their paycheck. Your employer quietly pays the other $480 as part of your compensation package. Family plans cost more in total dollars, but you're still getting a better deal than buying separate policies for each person in your household.

Medicare Advantage plans look cheap at $18 monthly, but there's a catch: you're already paying that $185 Part B premium to Medicare before the Advantage plan even enters the picture. Some Medicare Advantage options charge zero in additional premiums, while others climb past $100 depending on extra benefits like dental or vision coverage.

Medicaid varies wildly by state. If your state expanded Medicaid and you earn below 138% of poverty level, you're probably paying nothing. Non-expansion states might charge small copays or monthly fees, but rarely more than $15.

What Affects Your Health Insurance Premium

Six factors control what you'll pay. Insurers run the numbers on each one to calculate your risk profile and set your price within federal rules.

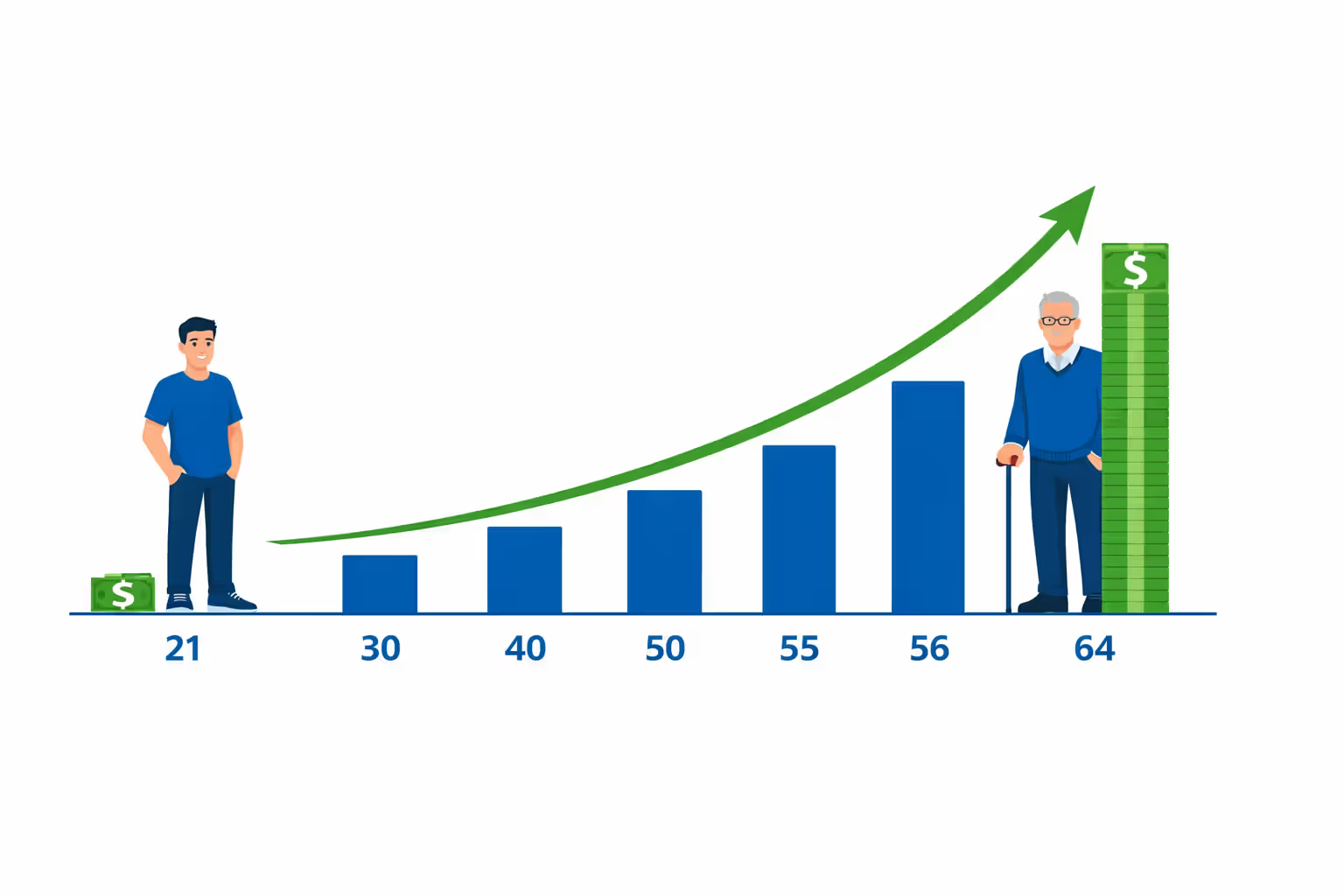

Age hits hardest. Federal law lets insurers charge a 64-year-old up to three times what they'd charge a 21-year-old for identical coverage. Without this 3:1 cap, the gap would stretch even wider. You'll notice premium jumps at ages 30, 40, and 50, but the really steep climb starts at 55.

Author: Ethan Bradford;

Source: blaverry.com

Location creates surprises. Insurance regulation happens state by state, and competition varies dramatically from one zip code to another. That same Silver plan costing $420 in Atlanta might run $900 in rural Alaska. Healthcare delivery costs, number of competing insurers, and state-specific regulations all push prices up or down.

Plan tier sets your monthly cost versus your costs at the doctor's office. Bronze options deliver the smallest monthly bills but slam you with massive deductibles when you need care. Platinum flips this equation—you pay more every month but less per visit. The metal tiers (Bronze, Silver, Gold, Platinum) reflect what percentage of total healthcare costs the plan covers on average: Bronze handles about 60%, Platinum takes care of roughly 90%. You're not getting superior doctors or bigger networks with expensive tiers—just different math on who pays what when.

Tobacco use can inflate your premium by half in most states. That $500 monthly bill becomes $750 if you smoke cigarettes, cigars, pipes, or use chewing tobacco. A few states ban or limit these surcharges, but where they're allowed, the penalty hurts. The good news: complete a cessation program, document your non-use period, and the surcharge disappears.

Family size drives up costs, but with a twist. Insurers typically price out the first three kids at full rate, then throw in additional children free. Two adults plus one kid might cost $1,400 monthly. Add three more kids? You might pay $1,650 instead of the $2,100 you'd expect from straight multiplication.

Income doesn't change what the insurer charges, but it transforms what you actually pay through subsidy eligibility. Picture two people buying identical Silver plans. One earns $35,000 and qualifies for subsidies that slash their cost to $150 monthly. The other makes $65,000 and writes a check for the full $550.

Premium variation is one of the most misunderstood aspects of health insurance. People often assume high premiums mean better coverage, but that's not accurate. A 60-year-old and a 25-year-old buying the same Silver plan get identical benefits—the older person simply pays more because they're statistically more likely to need care

— Cynthia Cox

Monthly Costs for Marketplace Plans vs Private Insurance

Marketplace plans sold through healthcare.gov follow standardized metal tiers. Private insurance purchased straight from insurers off the exchange might offer different benefit designs but usually costs about the same—or more. The crucial difference? Only marketplace enrollment unlocks premium subsidies.

Here's the cost breakdown by metal tier for a 40-year-old individual in 2025:

| Plan Tier | Average Premium (Full Price) | Average Premium (With Financial Help)* | Typical Deductible |

| Bronze | $450 | $95 | $6,500–$8,000 |

| Silver | $575 | $125 | $4,500–$6,000 |

| Gold | $685 | $240** | $2,000–$3,500 |

| Platinum | $795 | $315** | $500–$1,500 |

Based on household income around 200% of poverty level (~$30,000 for one person)

*Subsidies shrink as plans get richer; Gold/Platinum buyers often earn too much for major help

Bronze plans work for healthy people comfortable gambling on high deductibles in exchange for smaller monthly bills. You're basically buying catastrophic protection. With $6,500+ deductibles, you're covering most routine care yourself until you hit that threshold.

Silver plans hit the sweet spot for subsidy value. Premium tax credits apply across all tiers, but Silver plans offer an exclusive bonus: cost-sharing reductions that shrink your deductibles and copays if you earn under 250% of poverty level. This double subsidy makes Silver remarkably affordable for moderate-income households.

Gold plans make sense when you've got chronic conditions or know you'll need medical care. Higher monthly payments, sure, but lower deductibles mean less sticker shock at the pharmacy or specialist's office.

Platinum plans rarely pencil out financially unless you're managing serious health conditions requiring constant care. The premium jump from Gold to Platinum often outweighs the out-of-pocket savings unless you're practically living at the doctor's office.

Author: Ethan Bradford;

Source: blaverry.com

Private insurance purchased off-exchange costs roughly what you'd pay for unsubsidized marketplace plans, but you sacrifice subsidy eligibility. Why would anyone choose this? Timing. You can buy off-exchange plans any time, not just during the November-January open enrollment window. Some off-exchange plans also feature benefit designs unavailable on marketplaces, though ACA regulations have narrowed these differences considerably.

Short-term health plans represent a separate category of private coverage. They'll cost you 50-70% less than ACA-compliant plans—maybe $200 monthly versus $575 for Silver marketplace coverage. The tradeoff? They exclude pre-existing conditions, cap total benefits, and don't count as real coverage under federal law. They're unsuitable for anyone with health concerns.

How Much Does Employer Health Insurance Cost

Roughly 160 million Americans get coverage through work, making employer-sponsored insurance the dominant source for working-age people. The cost structure works completely differently than individual market insurance because your employer subsidizes most of the premium.

In 2025, the average employer health plan costs $625 monthly for single coverage and $1,950 for family coverage. But employees don't pay these full amounts.

Employee contributions typically hit about 22% for individual coverage and 27% for family plans. That translates to roughly $145 monthly from your paycheck for single coverage and $520 for family coverage. Your employer covers the remainder—$480 for individuals, $1,430 for families—as part of your total compensation package.

These averages hide massive variation. Some generous employers cover 90-100% of individual premiums, only asking employees to contribute toward dependent coverage. Other employers, especially small businesses struggling with tight margins, might split costs 50-50 or demand higher employee shares.

Company size influences premium costs too. Large employers with 500+ workers negotiate better rates through sheer volume, averaging $610 monthly for single coverage. Small employers under 50 workers face steeper rates around $675 monthly for comparable benefits. This economy of scale explains why small business employees often contribute more despite working for less profitable companies.

High-deductible health plans paired with Health Savings Accounts have exploded in popularity among employers. These plans run 15-20% cheaper on monthly premiums—perhaps $525 instead of $625 for single coverage—but dump more cost onto employees through deductibles exceeding $3,000. The HSA component lets you sock away pre-tax money to cover these deductibles, creating tax benefits that partially offset the higher out-of-pocket risk.

The tax treatment of employer contributions creates a hidden subsidy compared to individual market coverage. Your employer deducts their $480 monthly contribution as a business expense, while you receive it tax-free. That $625 employer plan with your $145 contribution effectively costs you less than a $450 individual market plan you'd buy with after-tax dollars.

Author: Ethan Bradford;

Source: blaverry.com

Ways to Lower Your Health Insurance Costs

Several strategies can dramatically cut your monthly health insurance bill. Which one works best depends on your income level, employment situation, and health needs.

Premium tax credits deliver the biggest bang for marketplace shoppers. These income-based subsidies reduce monthly premiums for households earning 100-400% of poverty level—roughly $15,000-$60,000 for individuals, $31,000-$120,000 for families of four in 2025. The credits get applied automatically when you enroll through healthcare.gov or your state marketplace. You don't file extra paperwork or wait until tax season.

A household pulling in $40,000 annually might qualify for $350 monthly in premium tax credits, cutting a $575 Silver plan down to $225. That same household earning $55,000 might receive $200 in credits, paying $375 monthly. Credits gradually phase out as income climbs, vanishing completely above 400% of poverty level.

Cost-sharing reductions work differently than premium subsidies. They don't touch your monthly bill, but they slash deductibles, copays, and out-of-pocket maximums for Silver plan buyers earning under 250% of poverty level. A standard Silver plan might carry a $4,500 deductible, but with cost-sharing reductions, that drops to $2,000 or even $500 for the lowest-income qualifying households.

Health Savings Accounts pair with high-deductible plans to create tax advantages. Money you contribute gets deducted from your taxable income, grows without tax consequences, and comes out tax-free for qualified medical expenses—a triple tax benefit. For 2025, you can stash up to $4,300 as an individual, $8,550 for families. If you're relatively healthy and can afford to fund an HSA, the tax savings often beat the cost of higher deductibles.

Medicaid expansion offers free or nearly free coverage in 40 states for adults earning up to 138% of poverty level (about $20,780 for individuals in 2025). If you live in an expansion state and earn below this threshold, Medicaid costs dramatically less than any private insurance option—usually zero in monthly premiums.

Spousal coverage sometimes delivers better value than individual marketplace plans. If your spouse has employer insurance with reasonable dependent coverage costs, joining their plan might beat buying separate individual coverage, particularly if you don't qualify for substantial subsidies.

Plan timing matters for marketplace shoppers. Enrolling during the main open enrollment period (November through January for most states) gives you the full plan year. Miss this window and you're stuck waiting for special enrollment triggered by qualifying life events like marriage, childbirth, or job loss—or you're forced toward pricier short-term plans.

Network selection creates a real price gap. HMO plans run 10-15% cheaper than PPO plans because they lock you into network providers and require primary care referrals before seeing specialists. If you're comfortable with these restrictions and have solid in-network options nearby, HMO plans deliver meaningful monthly savings.

Author: Ethan Bradford;

Source: blaverry.com

Health Insurance Cost Examples by State

Real premiums vary wildly depending on where you call home. Here's what a 40-year-old non-smoker pays monthly for Silver marketplace plans across six different states (2025 rates, no subsidies applied):

Florida — Miami residents pay approximately $550 monthly for Silver coverage. Multiple insurers compete across South Florida markets, which helps keep prices moderate. Head to rural Florida counties and prices jump to $625+ as carrier options thin out. Florida's large population and competitive insurance markets create relative affordability compared to less populated states.

Wyoming — Cheyenne residents face some of America's steepest premiums at roughly $825 monthly for Silver plans. Limited competition (often just one or two insurers statewide) and sparse population density drive costs skyward. Wyoming's small risk pool combined with expensive healthcare delivery in rural areas fuels premium inflation.

California — Los Angeles Silver plans average $485 monthly thanks to robust competition and state-level subsidies that stack on top of federal assistance. California's state exchange (Covered California) negotiates hard with insurers and actively manages plan offerings to control costs. San Francisco runs slightly higher at $520 monthly, while Central Valley cities drop to $450.

Texas — Houston residents pay around $575 monthly for Silver coverage, landing close to the national average. Dallas comes in slightly cheaper at $545, while rural West Texas counties climb past $650. Texas's large unsubsidized market and lack of Medicaid expansion create unique pricing dynamics compared to expansion states.

North Carolina — Charlotte residents pay approximately $625 monthly for Silver plans. North Carolina's insurance market has stabilized after some rocky early ACA years, with 3-4 carriers competing in most counties. Rural mountain and coastal counties see prices rise to $700+ as competition thins.

Arizona — Phoenix Silver plans average $515 monthly, reflecting moderate competition and relatively young demographics in urban areas. Tucson runs similar at $530. Rural Arizona counties, particularly near the California border, exceed $650 monthly with limited insurer participation.

These examples all assume a 40-year-old individual. A 60-year-old in these same locations would pay roughly 2.5 times these amounts because of age-based pricing rules. A family of four would pay approximately 2.8-3.2 times the individual rate depending on the children's ages.

Subsidy eligibility transforms these calculations completely. A household earning $35,000 in Wyoming might pay just $150 monthly despite the $825 base premium, while that same household in California might pay $75 monthly for a plan priced at $485 before subsidies.

Frequently Asked Questions About Health Insurance Costs

Health insurance ranks among the biggest monthly expenses for Americans buying their own coverage. Grasping how insurers calculate premiums, what causes price variation, and where to find financial assistance helps you make confident decisions during open enrollment.

The difference between listed price and actual cost can be enormous. That plan showing $650 monthly might actually cost you $150 after subsidies get applied, or potentially nothing if Medicaid covers you. Always verify eligibility for financial assistance before assuming coverage exceeds your budget. Healthcare.gov's calculator gives instant estimates once you plug in household size and income.

Choosing plans involves weighing trade-offs between monthly premiums and costs when you actually need care. Smaller monthly bills mean bigger deductibles and higher cost-sharing when you visit the doctor. Larger monthly premiums buy you better protection against medical bills piling up. Your current health status, comfort with financial risk, and overall financial situation should drive this choice more than price alone.

Where you live can generate surprising savings if you're considering relocation. A $300 monthly premium difference between states adds up to $3,600 annually—meaningful money if other factors make a move attractive. Remote workers with location flexibility should factor health insurance costs into residency decisions alongside housing costs and taxes.

Shopping annually during open enrollment protects you against price increases and plan changes. Insurers tweak premiums, provider networks, and covered benefits every year. That plan offering great value last year might have hiked rates 20% or dropped your preferred hospital from its network. Spending 15 minutes comparing options each November can save hundreds monthly.

Health insurance costs will probably keep climbing faster than your paycheck grows, making it critical to understand cost drivers and ways to reduce your bill. Whether you're buying individual coverage, evaluating employer options, or helping aging parents navigate Medicare choices, smart decisions start with realistic cost expectations and thorough comparison of what's available in your area.