Family sitting at kitchen table reviewing health insurance documents and insurance cards on laptop

Who Is the Policyholder for Health Insurance

Content

Ever stared at a medical form asking for "policyholder information" and drawn a complete blank? You're not alone. This seemingly simple question trips up thousands of people daily at doctor's offices, pharmacies, and hospital admissions desks. Getting it wrong can delay care, trigger billing headaches, or even result in claim denials that could've been prevented.

Policyholder Definition and Role

The policyholder owns the health insurance policy. Period. They signed the enrollment paperwork, agreed to the contract terms, and carry the legal relationship with the insurance company. Most times, they're cutting the checks for premiums—though we'll see exceptions in a moment.

Picture the policyholder as the account manager. They decide which family members get added to coverage. They receive letters from the insurer about policy changes. When open enrollment rolls around, they're the ones clicking through plan options and making selections. Need to report a marriage or newborn? That call comes from the policyholder, not from other covered relatives.

What does day-to-day ownership look like? You'll sign up during the enrollment window, provide accurate Social Security numbers and addresses for everyone joining the plan, and keep premiums flowing on time. Miss payments? Coverage vanishes—sometimes without warning—leaving your family stuck with scheduled surgeries or ongoing treatments and nowhere to send the bills.

Here's a common misconception: people assume the sickest family member or the person visiting doctors most often must be the policyholder. Wrong. A marathon-running dad can be the policyholder while his daughter with Type 1 diabetes generates 95% of the medical claims. Policyholder status addresses ownership and control, not medical usage.

The confusion makes sense. We think, "Who benefits most from this insurance?" But insurers think, "Who signed the contract with us?" Those are different questions entirely.

The policyholder is the person who has entered into the contract with the insurance company. Understanding this distinction is the first step to avoiding costly billing errors and claim denials

— Karen Pollitz

Policyholder vs Subscriber vs Member

Insurance companies love their jargon. Different terms float around that sound identical but mean distinct things. Switch insurers or compare documents from various carriers, and the terminology soup gets thicker.

Policyholder and subscriber usually point to the same person—whoever enrolled and maintains primary responsibility. Some companies lean toward "subscriber" for workplace group plans, while "policyholder" pops up more with plans bought individually. Either term identifies whose name sits at the top of the account.

Member casts a wider umbrella. Everyone with coverage under the policy counts as a member—policyholder included, plus all dependents. When a dad enrolls himself plus his wife and three kids under one family plan, that's five members total. Just one policyholder.

Dependent describes relatives covered through someone else's policy. Kids under 26 can stay on a parent's plan as dependents. Spouses usually qualify as dependents when one partner owns the coverage. Dependents get full benefits but can't touch administrative controls or policy settings.

Primary insured shows up on some insurance cards, typically meaning the policyholder. But watch out—in situations where someone carries multiple insurance sources, "primary" might indicate which plan pays claims first. Completely different concept.

Let me break down these distinctions with clear examples:

| Role | Who This Describes | Decision-Making Power | Everyday Example |

| Policyholder | Whoever signed the insurance contract and controls the account | Premium payments, adding family members, plan changes, correspondence with insurer | Sarah bought a marketplace plan last November and signed all the paperwork |

| Subscriber | Another word for policyholder (companies pick one term or the other) | Same authority as policyholder—these terms mean identical things | Marcus signed up through his employer's benefits portal during onboarding |

| Member | Every single person getting care under this policy | Following network rules, using your benefits, seeing doctors | Sarah's household has three members: her, her husband, and their daughter |

| Dependent | Relatives piggybacking on someone else's coverage | Zero administrative control, but full access to medical services | Sarah's 23-year-old daughter stays covered while finishing grad school |

Why does this matter? When you're on the phone with customer service and they request the subscriber number, they want the policyholder's ID—not a dependent's member number, even though dependents carry their own cards with unique IDs.

How Policyholder Status Works in Different Plan Types

Where your coverage originates shifts how the policyholder role operates. Each insurance source adds its own wrinkles to ownership and responsibility.

Employer-Sponsored Plans

Sign up for health insurance at work, and you become the policyholder for your slice of coverage—yes, even though your employer negotiated the master contract and might kick in 60% or 80% of premium costs. The company holds the overall group policy, but you own your specific coverage certificate.

You make the calls on who joins your coverage. Want to add your spouse? Your newborn? Your 22-year-old who just graduated college? Those decisions belong to you, not your boss.

Flip side: if you quit or get fired, the employer decides whether coverage stops immediately or extends through month's end. I've seen companies cut coverage the same day they process termination paperwork. Others let you ride out the month you already paid for.

Premium splits get messier with workplace plans. Maybe your company covers 75% of your individual premium but only 50% of dependent costs. You watch the employee portion vanish from your paycheck—$180 every two weeks for you, plus another $240 for your spouse and kids. You're still the policyholder despite your employer footing most of the bill.

Individual and Family Plans

Marketplace plans and policies purchased straight from insurers follow the cleanest policyholder blueprint. Whoever fills out the application and signs on the dotted line becomes the policyholder—no ambiguity. You cover the entire premium (minus subsidies, if you qualify) and make every decision about the coverage.

Married couples sometimes ask: can we both be policyholders together? Nearly all insurers reject this setup. Pick one spouse to be the policyholder. The other gets coverage—identical benefits, same network, equal access—but zero administrative authority.

This arrangement causes friction when marriages fall apart but divorce isn't finalized. The policyholder spouse can kick the other off at the next open enrollment or once divorce paperwork clears. The non-policyholder spouse? They can't exit independently, can't switch plans, can't do anything without involving the policyholder.

Author: Ethan Bradford;

Source: blaverry.com

Medicare and Medicaid

Medicare enrollees always serve as their own policyholders. You can't list someone else as a dependent on Original Medicare or Medicare Advantage. Each person signs up individually after hitting 65 or qualifying through disability.

Married Medicare couples maintain separate policies, even when choosing identical Medicare Advantage plans or Medigap policies. My parents both enrolled in the same Humana Medicare Advantage plan but received separate member IDs, separate bills, and separate customer service accounts. Neither spouse controls the other's coverage decisions.

Medicaid runs differently across state lines, but generally treats each covered person as their own policyholder—children included. A family might have every member on Medicaid, yet each person carries their own case file and coverage determination. Parents help minor kids with paperwork but don't "own" their children's Medicaid coverage like a parent owns a private family plan covering dependents.

Policyholder Responsibilities and Rights

Carrying policyholder status means wielding specific powers that dependents lack, alongside obligations affecting everyone under your coverage umbrella.

Keeping premiums paid tops the responsibility chart. Maybe your spouse chips in for their share, or your 25-year-old reimburses you for their portion. Doesn't matter—the insurer sees one name on the payment: yours. Bounced checks, late payments, insufficient funds? All that reflects on your record, not on the dependent who might've short-changed you.

Making enrollment choices falls exclusively to policyholders. Open enrollment arrives each fall. Your 24-year-old can't ring up the insurer asking to switch from the silver plan to the platinum plan. That decision flows through you, the policyholder.

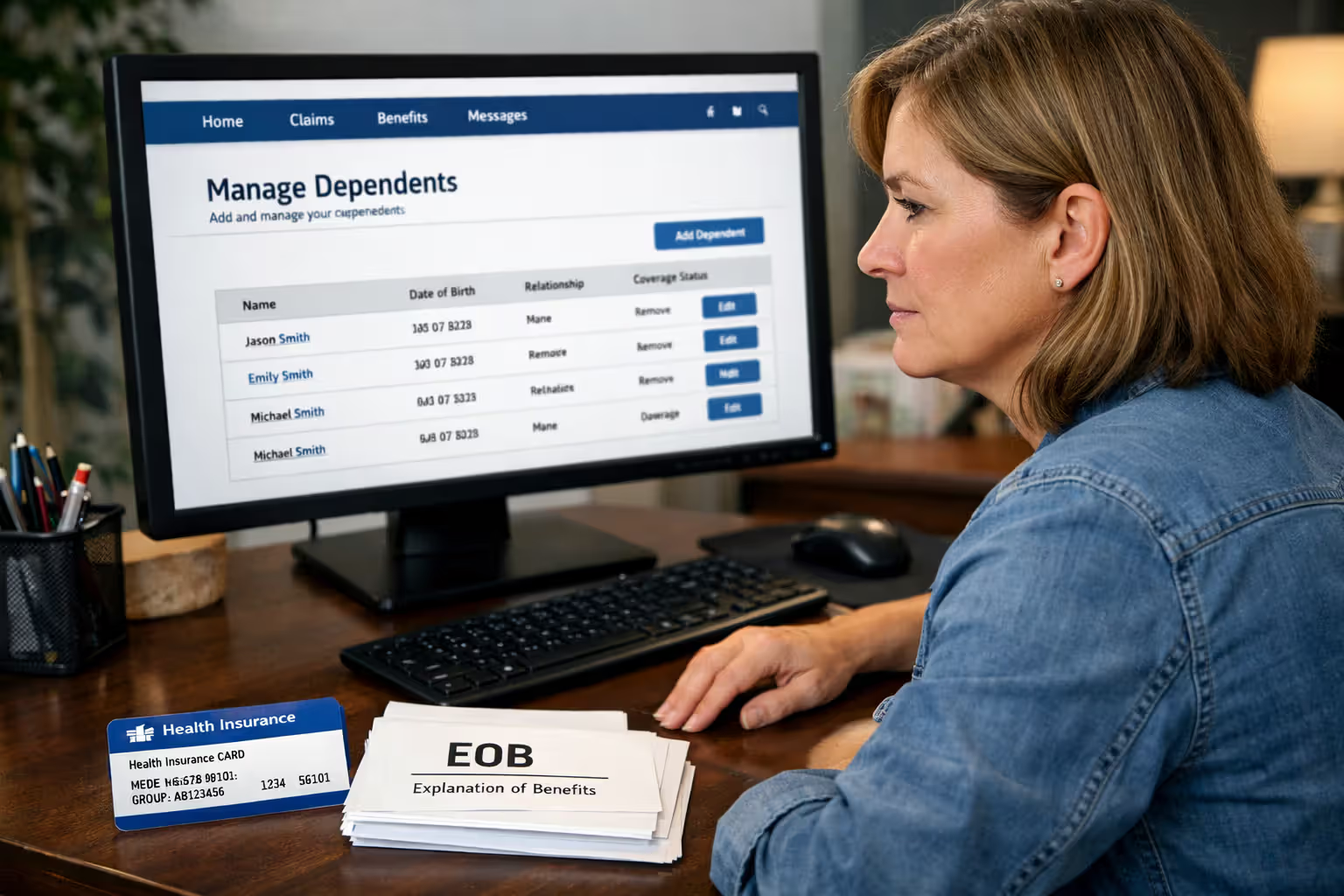

How much visibility do you get into everyone's medical claims? Most insurers send explanation of benefits statements to the policyholder for everything happening under the policy—your routine physical, your spouse's MRI, your teenager's urgent care visit for a sprained ankle. Certain insurers let adult dependents create their own portal logins to view their specific claims, though you (the policyholder) still see the complete picture.

Adding family and removing them requires your signature. You report births within 30 days (60 days for some insurers), marriages, adoptions, divorces—all within tight timeframes. Blow past these deadlines? Your newborn might wait until next open enrollment for coverage, sticking you with $15,000 in hospital bills because you missed the 30-day window.

Want to drop coverage mid-year? Only the policyholder can attempt that move (assuming no qualifying event allows it). Dependents can't cancel coverage even if they're desperate to get off the plan because they landed their own insurance through a new job.

One widely misunderstood power: accessing medical records. Being the policyholder doesn't hand you automatic keys to your dependents' health information. HIPAA privacy protections shield patients regardless of who funds insurance. Your 17-year-old's pediatrician won't fork over their medical charts just because you're the policyholder—you need separate authorization.

Author: Ethan Bradford;

Source: blaverry.com

Common Policyholder Scenarios and Examples

Real-life situations show how policyholder status plays out practically for families.

Parent covering children: Jennifer works at a tech startup and signs up for the employee health plan, adding her two teenage sons as dependents. She's the policyholder. Her 18-year-old son needs knee surgery after a skateboarding accident. The hospital makes Jennifer sign financial paperwork even though her son reached legal adulthood six months ago. The insurance company mails all explanation of benefits statements to Jennifer's address, giving her visibility into exactly what medical services her sons received—unless they file HIPAA restrictions.

Spouse as policyholder: Marcus scored excellent insurance through his engineering job—$20 copays, $1,500 deductible, huge provider network. His wife Elena ditched her workplace coverage (which had a $6,000 deductible and required referrals for everything) and jumped onto his plan as a dependent. Marcus owns the policy. When Elena needs coverage verification for a new cardiologist, she shows her own insurance card bearing her name and member ID. But if billing disputes pop up? The insurer communicates with Marcus. Should Marcus lose his job? Elena's coverage vanishes too, even though she could've maintained her own employer plan.

Adult children on parents' plans: Sophia celebrates her 24th birthday and moves 2,000 miles away for grad school in Seattle while her parents stay in Austin. She remains on her father's health insurance as a dependent. Her dad is the policyholder. Sophia visits a new doctor who asks for policyholder name and birthdate—her father's details, not hers. Some medical offices get confused and attempt billing Sophia directly, assuming she carries her own policy. She explains she's a dependent, provides her dad's information, and occasionally loops him into billing conversations when the office refuses to believe a 24-year-old uses someone else's insurance.

Domestic partners: Alex and Jordan aren't married but share an apartment and have been together for four years. Alex's employer permits domestic partner coverage. Alex becomes the policyholder; Jordan becomes the dependent. Unlike married couples, Alex typically owes taxes on the value of Jordan's coverage since the IRS doesn't recognize domestic partners as spouses for tax purposes. If they split up, Alex must boot Jordan at the next open enrollment or within 30 days if the employer allows mid-year relationship changes.

Blended families: Rachel remarries and wants her new stepchildren on her health plan. Whether she can add them hinges on her employer's policies and state regulations. If permitted, she becomes the policyholder for coverage spanning her biological kids and stepkids. Should she and her spouse divorce, she generally must remove the stepchildren, even after covering them for years—though some states carve out exceptions when stepparents maintain a parental role.

Author: Ethan Bradford;

Source: blaverry.com

How to Find Out Who the Policyholder Is

Figuring out the policyholder should be straightforward, yet insurance cards don't always spell it out clearly.

Examine your insurance card: Most cards display the subscriber or member name prominently. See one name at the top followed by "and dependents" or several names in a list? That first name tells you who the policyholder is. Some cards show a subscriber ID distinct from dependent member IDs—that subscriber ID belongs to the policyholder.

Dig through policy paperwork: Your insurance packet, welcome letter, or coverage certificate explicitly identifies the policyholder. These documents arrived when coverage kicked off and should live with other vital records. Digital versions usually sit in your online account under "Documents" or "Policy Details."

Access your online account: Whoever can log in as the primary account holder is the policyholder. Can't create an account because "a subscriber account already exists for this policy number"? Someone else is the policyholder. You might establish a dependent access account with restricted features.

Phone the insurance company: Customer service instantly identifies the policyholder when you provide the policy or member ID. They'll confirm the policyholder's name, birthdate, and contact information in their system.

Consult your HR department: For workplace plans, your benefits coordinator knows who enrolled and who's listed as dependents. They can retrieve your enrollment forms showing who signed as the employee/policyholder.

Check whose bank account displays insurance deductions. That person likely owns the policy—though this method isn't foolproof when couples share finances and pay from joint accounts.

One trap to dodge: assuming whoever racks up the most medical bills is the policyholder. The parent visiting doctors once every three years might be the policyholder while their chronically ill child who's a dependent generates dozens of claims annually.

Frequently Asked Questions About Policyholders

Think of the policyholder as the command center for health insurance coverage. They hold authority and responsibility extending far beyond their own medical appointments. Whether you're the mom covering your family, the employee adding a spouse, or the 25-year-old still on your parent's plan, grasping who the policyholder is prevents headaches during claim filing, coverage modifications, or billing disputes.

Figure out who holds this role on your current coverage today. Store policy documents where you can grab them quickly. Understand your rights if you're a dependent. Fulfill your obligations if you're the policyholder. Sure, terms like policyholder, subscriber, member, and dependent might sound like insurance industry gobbledygook, but these labels carry real weight when you need coverage to function properly.

Unsure about your policyholder status? Check your insurance card right now. Log into your member portal. Call your insurer directly. Spending five minutes getting clarity beats spending five hours untangling confusion later when you're managing a medical emergency or racing to add a newborn during a tight enrollment deadline.