Family sitting at kitchen table reviewing medical bills and health insurance documents with worried expressions

Why Is Health Insurance So Expensive in America

Content

Pull up your most recent insurance statement and look at the numbers. Last January, your family plan cost $420 monthly. Now it's $570. That deductible? Jumped from $2,800 to $4,200. And despite paying all that money, you still dropped $340 at your doctor's office last month for what should've been routine care.

The total picture looks even worse. Between premium payments and what your employer kicks in (yeah, they're paying way more than you see), the average family plan now runs $25,572 per year according Kaiser Family Foundation data. Back in 2010, that same coverage cost $13,770. Your paycheck didn't double in that timeframe—probably didn't even grow 40%—but insurance costs sure did.

So who's the bad guy here? That's the frustrating part: there isn't just one. You've got a dozen different factors—some obvious, others buried in industry mechanics—all working together to drain your wallet. Let me walk you through exactly where your money goes.

How Health Insurance Pricing Actually Works

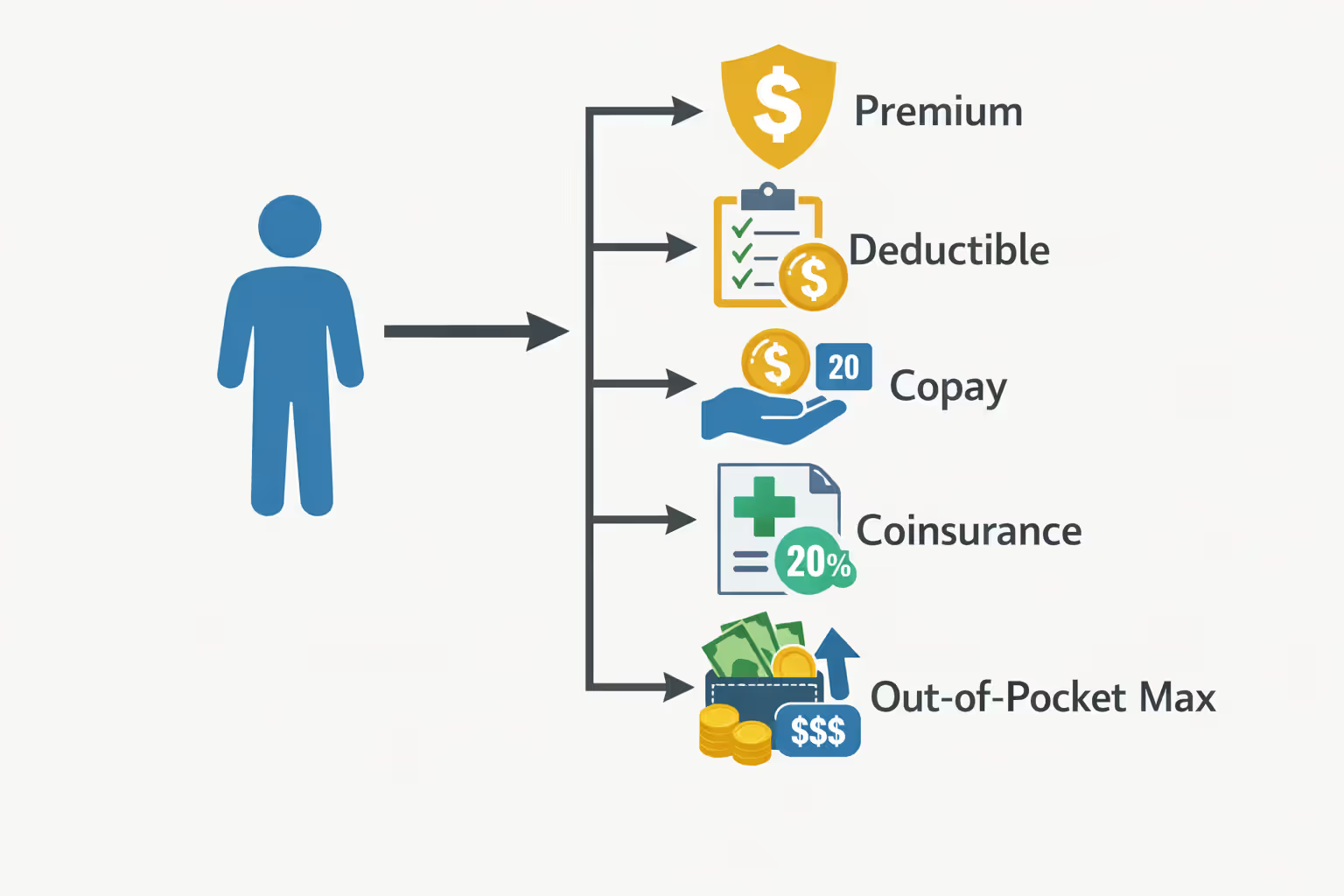

Most people get blindsided by healthcare costs because they don't understand how the billing actually breaks down. You're juggling multiple payment types, and each one works differently.

Your premium comes first. Think of it as a gym membership—you're paying every month whether you walk through the door or not. Stop paying and your coverage vanishes immediately, no grace period, no second chances.

Next comes the deductible, which trips up almost everyone. Let's say you've got a $3,200 deductible and you tear your ACL in April. That emergency room visit, the MRI, the orthopedic consultation? You're covering every dollar of that $3,200 yourself before your insurance touches anything. Every copay, every test, every prescription counts toward reaching this threshold. Only after you've spent $3,200 does your insurance company start splitting bills with you.

Co-payments are simpler—fixed prices for certain services. Maybe $40 when you visit your primary doctor, $75 for specialists, $15 for generic prescriptions. These don't change based on the actual cost of care; they're flat fees you pay regardless. You'll pay these even after clearing your deductible.

Coinsurance confuses people constantly. After hitting your deductible, you don't stop paying—you split costs with your insurer using a percentage formula. Most common split is 80/20. So when you need that $5,000 shoulder surgery, you're still paying $1,000 (your 20%) while insurance handles $4,000 (their 80%).

The out-of-pocket maximum supposedly protects you from financial catastrophe. Once you've paid $9,200 in qualified expenses, insurance covers everything else at 100% for the remainder of that calendar year. Sounds reassuring until you realize most people never hit this ceiling—they just hemorrhage money all year without triggering complete coverage.

Here's the trap nobody warns you about: spending $650 monthly on premiums doesn't mean you'll pay less when you actually get sick. You can absolutely get stuck paying massive premiums AND a $5,000 deductible. Insurance companies deliberately mix these elements, forcing you to choose between paying upfront or gambling on staying healthy.

All this complexity requires an enormous infrastructure. Claims processors, billing specialists, customer service agents, fraud investigators, appeals coordinators—insurance companies employ thousands of people just to manage these moving parts. Those salaries and computer systems cost billions, and every penny gets baked into your premium.

Author: Ethan Bradford;

Source: blaverry.com

Main Factors Driving High Health Insurance Costs

Multiple systemic problems collide to make American health insurance absurdly expensive compared to literally every other developed country on Earth.

Administrative Costs and Insurance Company Profits

Administrative waste consumes approximately $950 billion every year in the American healthcare system—somewhere between a quarter and a third of total healthcare spending. Compare that to countries running single-payer systems like Canada or Taiwan, where administrative overhead runs 5-10% of total spending. We're burning three to six times more money on paperwork than necessary.

Why such bloat? Every insurance company builds separate claims processing systems, negotiates individual contracts with thousands of doctors and hospitals, maintains distinct member websites, and pays teams to determine whether treatments are "medically necessary." Hospitals fight back by hiring massive billing departments—sometimes ten billing staff for every practicing physician—just to navigate coding requirements across dozens of different insurers with different rules.

Insurance companies need profits too. The ACA limits their administrative spending and profit to 20% (forcing them to spend 80% on actual medical care), but that still leaves substantial room for profit-taking. Major insurers post quarterly profits in the billions. That money comes from one place: your monthly premium check.

Network management creates another expensive layer. Each insurer separately negotiates payment rates with hospitals, doctors, laboratories, imaging centers, and specialists. These fragmented networks require constant maintenance and verification. You've experienced this headache: you call three times to confirm your gastroenterologist accepts your plan, then show up for your appointment and discover they stopped accepting it six weeks ago despite being listed as "in-network" on the website you checked yesterday.

Prescription Drug Prices

Americans get absolutely hammered on medication costs—routinely paying double or triple what Canadians or Germans pay for identical pills manufactured in the same factories. A three-month supply of a cholesterol medication costing $95 in Montreal might run $285 in Miami. Same drug, same manufacturer, same dosage—radically different price.

Pharmaceutical companies justify these prices by claiming they fund research and development of new treatments. Check their actual spending, though: they pour more money into marketing departments than research labs. The United States and New Zealand are the only countries allowing direct-to-consumer drug advertising, which floods television with commercials pushing expensive brand-name drugs when cheaper alternatives work just as well.

Patent manipulation extends monopoly pricing far beyond original patent protections. Drug makers slightly reformulate an existing tablet into a capsule, patent the new delivery method, and secure another twelve years of exclusive high pricing. Or they combine two existing generic drugs, patent the combination, and charge premium prices despite zero actual innovation.

Look at insulin—discovered in 1921, costs roughly $10 per vial to manufacture. American patients pay $300-$400 monthly for this medication they literally cannot live without. People ration insulin, stretching supplies by skipping doses, sometimes dying as a direct result. Meanwhile, pharmacy benefit managers (the middlemen between insurers and drug manufacturers) extract fees and rebates that inflate prices without providing any benefit to actual patients.

Author: Ethan Bradford;

Source: blaverry.com

Hospital and Medical Provider Fees

Hospital pricing in America exists in a completely irrational alternate dimension. A single bag of saline solution might appear on your bill at $137. Getting an MRI costs $425 at one imaging center and $2,800 at a hospital four miles away—identical procedure, comparable equipment quality, wildly different prices with no justification.

Hospitals practice aggressive "cost-shifting." Medicare and Medicaid frequently reimburse below actual treatment costs, so hospitals inflate prices charged to privately insured patients to make up the difference. Your insurance company then "negotiates discounts" from these deliberately inflated list prices, but even the discounted rates far exceed what other countries pay for the same procedures.

Healthcare consolidation drives prices relentlessly higher. As hospital systems merge and gobble up physician practices, they gain enormous negotiating leverage. A dominant health system serving a region can demand higher reimbursement rates, knowing insurers can't exclude them without losing access to essential providers that patients need. Those increased costs flow directly into higher premiums.

Defensive medicine wastes tens of billions on unnecessary tests and procedures ordered primarily for legal protection rather than medical benefit. Doctors order that extra CT scan not because it'll change your diagnosis or treatment plan, but because having it in your chart protects them from potential malpractice lawsuits. They're covering legal bases rather than improving actual patient outcomes.

Medical technology advances deliver genuine miracles—cancer treatments that add years to lives, robotic surgical systems that reduce complications, diagnostic equipment that catches diseases earlier. All of it costs millions. Hospitals distribute these equipment expenses across all patients through facility fees, equipment charges, and inflated procedure costs that ultimately drive premium increases for everyone.

How Plan Types Affect Your Costs

The structure of your specific plan has enormous impact on both what you pay monthly and what you'll owe when you actually need medical care.

HMO (Health Maintenance Organization) plans carry the lowest monthly premiums but lock you into narrow provider networks. You choose a primary care physician who coordinates all your care and writes referrals any time you need to see specialists. Go outside the network without authorization? You'll pay full price yourself unless it qualifies as a genuine emergency. HMOs work well if you already have doctors in that network and you're fine with less flexibility in exchange for lower premiums.

PPO (Preferred Provider Organization) plans cost more monthly but give you significantly more freedom. You can see any doctor without needing referrals, though staying in-network saves money through negotiated discount rates. Out-of-network care still gets covered—you just pay higher coinsurance percentages. PPOs make sense when you want easy specialist access without gatekeeping, or when you travel frequently and need coverage that works across state lines.

EPO (Exclusive Provider Organization) plans occupy middle ground between HMOs and PPOs. You don't need referrals to see specialists, but coverage only exists for in-network providers (genuine emergencies excepted). Monthly costs usually sit between HMO and PPO pricing. These work if you want specialist access without referral hassles but won't need out-of-network coverage.

HDHP (High Deductible Health Plan) plans feature lower monthly premiums paired with deductibles starting around $1,600 for individuals or $3,200 for families. You'll cover most routine medical costs entirely out-of-pocket until hitting these high thresholds. The major advantage? Eligibility for Health Savings Accounts (HSAs) that let you contribute pre-tax dollars for medical expenses. HDHPs suit relatively healthy people who rarely need care and want to minimize monthly costs while building tax-advantaged medical savings.

| Plan Design | Avg. Individual Yearly Premium | Avg. Deductible Amount | Standard Max Out-of-Pocket | How Much Provider Choice | Who Benefits Most |

| HMO | $7,200 | $1,800 | $6,500 | Very Limited (★☆☆☆☆) | Budget-focused with trusted local doctors already in-network |

| PPO | $8,900 | $2,200 | $7,800 | Extensive (★★★★☆) | Anyone valuing maximum provider choice and flexibility |

| EPO | $8,100 | $2,000 | $7,200 | Moderate (★★★☆☆) | People comfortable staying in-network who dislike needing referrals |

| HDHP | $6,400 | $3,500 | $7,000 | Varies (★★★☆☆) | Healthy individuals, disciplined savers who maximize HSA benefits |

Choose poorly and you'll waste thousands. A healthy 32-year-old paying $325 monthly for a PPO when an HDHP would cost $195 throws away $1,560 yearly—money that could be growing tax-free in an HSA. Flip the scenario? Someone managing multiple chronic conditions choosing an HDHP might face $4,200 in out-of-pocket costs before insurance contributes a single dollar to their care.

Hidden Costs That Increase Your Health Insurance Bill

Beyond the obvious premiums and deductibles, several sneaky factors inflate what you actually spend on healthcare.

Surprise billing strikes when you carefully choose an in-network hospital but get treated by an out-of-network provider—an anesthesiologist during surgery, an emergency room physician, a radiologist interpreting your scans. You assumed you were covered properly, then a $3,400 bill arrives four months later. Federal legislation passed in 2021 limits surprise billing in many situations, but loopholes remain, particularly for ground ambulance transport which can cost thousands.

Denied claims force you to either pay out-of-pocket or fight through exhausting appeals processes. Insurers deny 15-20% of claims initially—sometimes legitimately because services aren't covered, often for technical reasons like incorrect billing codes or missing prior authorization. Even when you win appeals, the process takes months and requires incredible persistence. Many people just pay to avoid the hassle.

Coverage gaps hide in policy fine print. Your plan might cover physical therapy but cap it at 18 visits per year—completely inadequate for serious injuries requiring four months of rehabilitation. Mental health coverage may carry higher cost-sharing percentages than physical health services. Fertility treatments, medical weight loss programs, certain preventive screenings—these often face complete exclusions or strict limitations that come as unpleasant surprises.

Employer contribution changes gradually shift costs to employees. Your company might maintain the same percentage split on premium contributions but switch you to a plan with a $1,500 higher deductible. Technically your premium contribution stayed flat, but your actual financial exposure jumped substantially without you noticing during open enrollment.

Out-of-network balance billing happens when providers charge more than your insurance considers reasonable. Your insurer pays their maximum allowed amount for a procedure, then the provider bills you directly for the difference—potentially hundreds or thousands for a single appointment or surgery.

Author: Ethan Bradford;

Source: blaverry.com

Common Mistakes That Make Health Insurance More Expensive

People accidentally jack up their healthcare spending through completely preventable errors.

Choosing plans based purely on monthly premium cost ignores your real annual spending picture. A plan charging $165 monthly with a $5,500 deductible might ultimately cost more than one charging $285 monthly with a $1,800 deductible—assuming you need any significant medical care during the year. You need to calculate total potential costs based on your expected healthcare usage, not just grab whichever plan has the lowest monthly payment.

Ignoring HSA opportunities leaves substantial tax-advantaged money sitting on the table completely unused. If you qualify for an HDHP with an HSA, contributing just $120 monthly saves $30-40 in taxes (depending on your bracket) while simultaneously building funds for future medical expenses. HSAs deliver triple tax advantages unique in the tax code: contributions reduce your taxable income, money grows investment returns tax-free, and withdrawals for qualified medical expenses come out completely tax-free. Find me another investment vehicle offering that combination.

Skipping preventive care appears to save money short-term but creates far more expensive problems down the road. Standard plans cover annual physicals, recommended cancer screenings, and vaccinations without charging you any deductibles or copays whatsoever. Catching high blood pressure, pre-diabetes, or early-stage colon cancer during routine screening costs dramatically less—and causes far less suffering—than treating advanced disease years later. That colonoscopy you're avoiding could prevent $150,000 in cancer treatment costs.

Not comparing marketplace options annually means missing better deals or subsidy eligibility changes you don't know about. Insurance companies adjust plans, pricing structures, and provider networks every single year without fail. Auto-renewing your current plan might cost you $2,400+ more than switching to a competitor's similar plan with nearly identical coverage. During open enrollment, invest ninety minutes comparing options thoroughly—it's effectively worth $200+ per hour of your time.

Author: Ethan Bradford;

Source: blaverry.com

Using emergency rooms for non-emergencies triggers facility fees of $1,200-$3,500 before doctors even examine you or run any tests. Urgent care centers charge $175-$350 for similar services treating the same non-life-threatening conditions. Unless you're experiencing genuine emergencies—chest pain suggesting heart attack, severe bleeding, difficulty breathing, suspected stroke symptoms—urgent care or same-day primary care appointments save substantial money.

Failing to verify network status before scheduling appointments leads directly to surprise bills you weren't expecting. Provider networks change constantly, sometimes even mid-year during your coverage period. That specialist who definitely accepted your insurance four months ago might have dropped your plan since then. One three-minute phone call confirming current network status prevents an $950 out-of-network bill showing up six weeks later.

How to Reduce Your Health Insurance Expenses

Strategic approaches can dramatically lower your healthcare spending without sacrificing coverage you genuinely need.

Maximize subsidies if you qualify for them. Premium tax credits through the ACA marketplace can slash monthly costs by hundreds for households earning up to 400% of federal poverty level (roughly $58,320 for individuals, $120,000 for families of four). Many people assume they don't qualify without actually running the numbers. Check the marketplace calculator—you might qualify for substantial financial help you didn't know existed.

Leverage employer plans strategically. If your employer offers multiple plan options, carefully model your expected annual costs under each scenario. Factor in any employer HSA contributions, which some companies offer as incentives for HDHP enrollment. If your spouse's employer also offers coverage, compare total household costs under different enrollment combinations—sometimes splitting coverage between two employer plans makes financial sense despite seeming complicated.

Use telemedicine for minor health issues. Virtual doctor visits typically cost $30-$60 versus $125-$225 for in-person office appointments for the same consultation. Many plans now cover telemedicine with lower cost-sharing than traditional office visits. Works perfectly for sinus infections, minor rashes, urinary tract infections, and prescription refills when you don't need hands-on physical examination.

Request generic medications proactively. Generic drugs cost 80-85% less than brand names despite being chemically identical by FDA requirement. When your doctor writes a prescription for a brand-name medication, specifically ask whether a generic equivalent exists and works just as well. Pharmacy benefit managers sometimes create perverse financial incentives favoring expensive brands—your doctor might not realize that $220 brand drug has a $18 generic alternative that's medically equivalent.

Negotiate medical bills directly with providers. Hospitals and medical practices often accept reduced payment amounts or interest-free payment plans for patients paying substantial bills out-of-pocket. Before paying a large medical bill, call the billing department and directly ask about discounts for prompt payment in full or financial hardship programs. Many facilities write off significant portions of bills rather than pursuing aggressive collections that cost them money too.

Time non-urgent procedures strategically around your deductible. Already met your deductible in November? Schedule that elective knee surgery or planned hernia repair before year-end rather than waiting until February when your deductible resets to zero. Conversely, if you haven't touched your deductible by late October, delaying non-urgent procedures until next plan year might make financial sense depending on your expected total costs.

Compare facility costs before scheduling procedures. For planned procedures like imaging, colonoscopies, or outpatient surgeries, call multiple providers requesting cash prices or insurance cost estimates. That routine MRI might cost $675 at an independent imaging center versus $2,650 at a hospital outpatient department. Your insurance covers both facilities, but lower costs mean reaching your deductible faster or paying less total coinsurance.

Participate in employer wellness programs when offered. Some employers reduce premium contributions or make direct HSA deposits for employees completing biometric health screenings, participating in fitness challenges, or achieving specific health goals like tobacco cessation. These programs might save $400-$750 annually for relatively minimal time investment.

American health insurance costs reflect a system fundamentally designed around fragmented private markets rather than centralized price regulation. We've built a structure where every participant—insurers, hospitals, pharmaceutical companies, and various intermediaries—extracts profit margins at each transaction point, and those cumulative costs get passed directly to consumers through premiums and cost-sharing. Until we address core structural issues around pricing transparency, administrative simplification, and market consolidation, costs will keep outpacing both general inflation and wage growth indefinitely

— Dr. Emily Chen

Frequently Asked Questions About Health Insurance Costs

Health insurance costs in America stem from deeply interconnected systemic problems: crushing administrative complexity, unchecked pharmaceutical pricing power, aggressive provider consolidation, and a fragmented market structure that prioritizes profit extraction over cost containment at every transaction point. No single factor explains why Americans pay exponentially more than citizens of other wealthy nations for comparable—or frequently worse—health outcomes.

Understanding the actual mechanics behind your insurance costs—from how premiums and deductibles interact to hidden expenses lurking in policy fine print—empowers substantially better decision-making during open enrollment and throughout the year. Selecting the appropriate plan type for your specific situation, avoiding common expensive mistakes, and employing strategic cost-reduction approaches can save thousands annually without sacrificing coverage you genuinely need.

The broader system desperately needs structural reform to achieve meaningful cost reductions that benefit everyone, but individual action still delivers measurable results right now. Compare plans thoroughly during every open enrollment period, maximize all available subsidies and tax advantages, leverage preventive care to catch problems early when they're cheapest to treat, and don't hesitate to negotiate bills directly or aggressively question charges that seem excessive. Every dollar saved on healthcare expenses becomes a dollar available for competing financial priorities—whether building emergency savings, investing for retirement, paying down debt, or simply reducing chronic financial stress.

Healthcare costs will almost certainly continue rising faster than general inflation in the near term given current system incentives, making informed insurance choices increasingly critical for basic financial security and stability. The complexity isn't accidental or natural, but you don't need specialized expertise to make substantially better decisions. Focus on understanding your own specific health needs realistically, calculating total potential annual costs rather than fixating on premium amounts alone, and systematically taking advantage of every available cost-saving opportunity within the current system.