Laptop on a desk showing health insurance plan comparison website with Bronze Silver and Gold tier cards, documents and calculator nearby in a bright home office

How to Get Health Insurance in the United States

Content

Most Americans find the health insurance system baffling. You've got enrollment windows that slam shut without warning, confusing plan names, and prices that seem to shift based on invisible calculations. Last year, my neighbor missed his enrollment deadline by three days—just three days—and spent eight months uninsured because he didn't realize qualifying for a special exception required documentation he didn't have.

The coverage you can access right now depends entirely on your employment status, what you're earning, how old you are, and whether your life recently changed in specific ways the government recognizes. Someone working full-time at a large company has different doors open than a freelance graphic designer or someone collecting unemployment checks.

What follows is the practical roadmap: which coverage types exist, who gets to use them, the actual windows when you can sign up, and the expensive mistakes that drain bank accounts. You'll learn to match your situation with the right insurance source and navigate the application without the usual headaches.

When You Can Enroll in Health Insurance

Insurance companies won't sell you coverage any random Tuesday you decide you want it. They've established rigid timeframes with narrow exceptions built around preventing people from gaming the system.

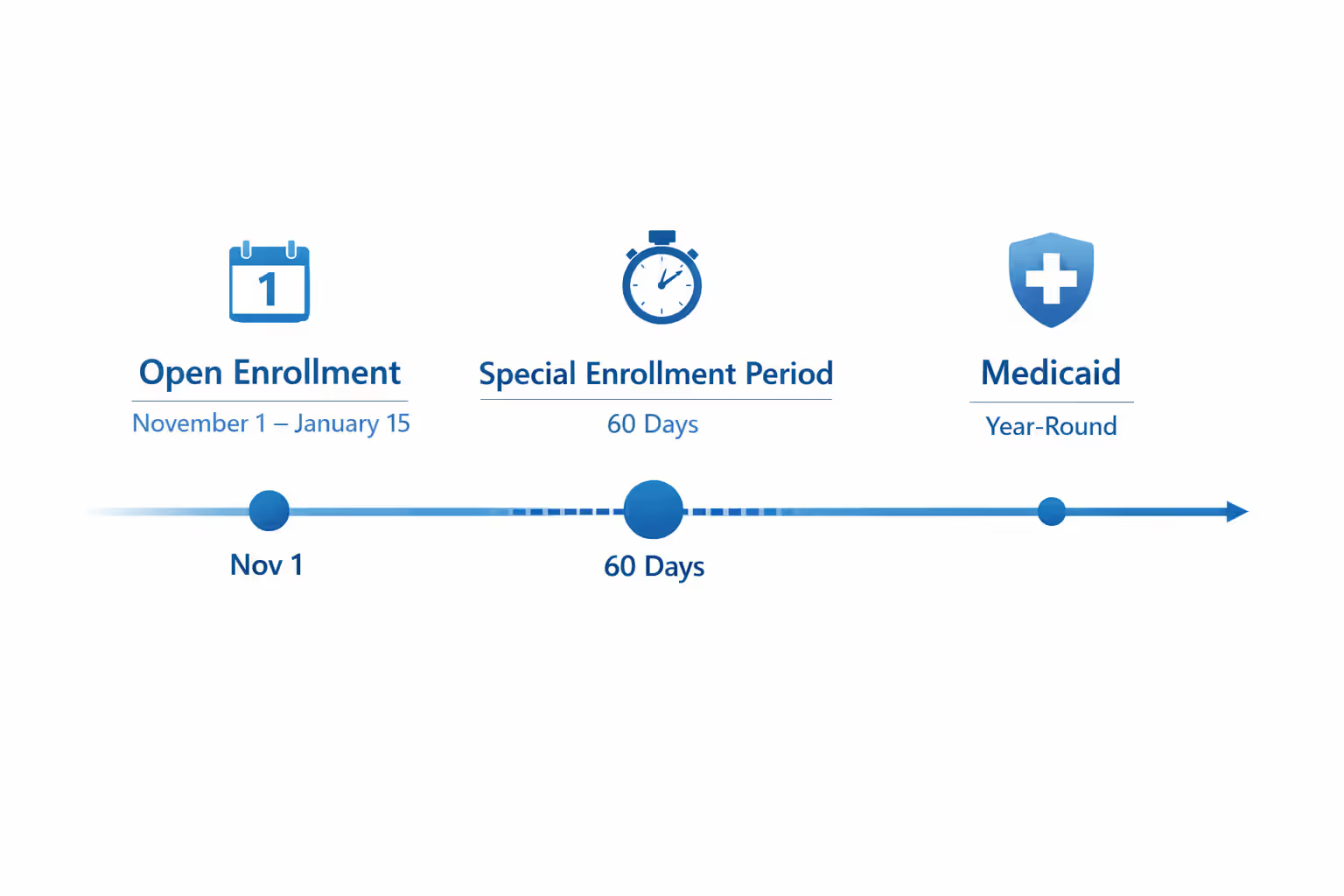

The Open Enrollment Period runs November 1 through January 15 annually. Planning to get covered starting January 1? Complete your purchase by December 15. Browse plans on December 28 and enroll by January 15, your coverage starts February 1. Wait until January 20 to start shopping? You've missed your chance and you're waiting until next November unless something major shifts in your life.

Those major life shifts unlock Special Enrollment Periods. Lost your job and the insurance attached to it? Sixty days to pick replacement coverage. Got married last month? You've opened a window. Had a baby, brought home an adopted child, or finalized divorce papers? Each qualifies. Relocated to another state or even crossed into a different county? That works. Your income changed enough to affect what subsidies you're eligible for? Another qualifying trigger. Finally became a U.S. citizen? You're covered.

The restriction: action required within sixty days of whatever happened. You'll prove it actually occurred—termination letters from employers, official marriage certificates, signed lease agreements showing your address change.

What if you need insurance starting tomorrow? Your choices narrow fast. Medicaid accepts applications twelve months a year. Qualify based on what you're earning, and some states turn coverage on the same month you submit paperwork. Others make it effective up to ninety days before you applied, assuming you met requirements during that earlier period. Children's Health Insurance Program follows comparable rules.

Short-term plans represent another quick option, though these barely qualify as real insurance. Coverage can activate within one to three days, but they won't touch pre-existing conditions, they cap total benefits at amounts that won't cover major illness, and they exclude essential benefits like maternity care and prescriptions. Think of them as disaster-only protection for healthy people bridging temporary gaps.

Author: Melissa Grant;

Source: blaverry.com

Starting a new job? Employer plans usually impose waiting periods—thirty, sixty, or ninety days are common—before you can join. Once that waiting period expires, coverage generally kicks in on the first day of whichever month comes next.

Where to Get Health Insurance Based on Your Situation

Finding insurance means figuring out which pathways you're actually allowed to walk through. Let's examine each source systematically.

Health Insurance Marketplaces function as shopping hubs for anyone lacking employer coverage. Most states direct residents to the federal marketplace at HealthCare.gov, while about twelve states operate their own platforms—California runs Covered California, New York operates NY State of Health, and so on. The compelling reason to use Marketplaces? Premium tax credits that can demolish your costs. Picture someone earning $40,000 yearly watching a $450 monthly premium shrink to $175 after subsidies kick in. These tax credits only apply to Marketplace purchases—buy directly from an insurance company and you're paying full price. Income ranging from 100% to 400% of federal poverty level (approximately $15,060 to $60,240 for one person) qualifies you for assistance.

Employer-sponsored insurance covers most working-age Americans. Companies employing 50+ full-time workers must offer plans or pay penalties. Smaller businesses aren't required to provide anything but many do to compete for employees. Employer plans usually deliver the best deal because your company shoulders 70-85% of premiums. You're only covering the remainder through paycheck deductions. That $600 monthly premium might only cost you $150. You'll enroll when initially hired (after any waiting period runs out) or during your company's annual enrollment window, which could land anywhere from October through January depending on the organization.

Medicaid serves low-income individuals and families, though "low-income" definitions shift dramatically by state. Thirty-eight states expanded Medicaid under the ACA, covering adults earning up to 138% of federal poverty level—roughly $20,783 for one person. The twelve states that refused expansion maintained tighter restrictions, sometimes limiting Medicaid exclusively to pregnant women, children, elderly residents, and disabled individuals. Expansion states give a single adult earning $20,000 completely free Medicaid coverage. States that rejected expansion might not qualify that same person for anything. Apply through your state's Medicaid office or through the Marketplace, which automatically transfers you to Medicaid when you're eligible. Premiums run from zero to minimal amounts.

Medicare becomes available at 65 for most Americans, plus it covers younger people with particular disabilities or end-stage renal disease. Your Initial Enrollment Period spans seven months total: the three months leading up to your 65th birthday, the birthday month itself, and the three months following. Miss this window and penalty surcharges attach to your Part B and Part D premiums—forever. Those penalties grow larger the longer you delay, tacking on 10% for every twelve-month period you should have carried Part B but didn't.

Private insurance companies sell coverage directly without marketplace involvement. Why skip the marketplace? When your income pushes you above subsidy eligibility, shopping directly sometimes uncovers plan options not displayed on the exchange. Some carriers provide broader networks or distinctive benefits exclusively in their direct-sale products. The tradeoff: you're paying full price with zero tax credits reducing the blow.

COBRA allows continuing your previous employer's coverage after leaving a job—valuable if you're mid-treatment with a specialist or managing serious health issues. You'll pay the complete premium (the portion your employer covered plus your contribution) plus a 2% administrative fee. That plan costing you $200 monthly in payroll deductions? The actual total might run $850 monthly. COBRA typically extends eighteen months, occasionally longer under specific circumstances.

Getting Coverage Without a Job

Losing employment doesn't eliminate your insurance options—though plenty of people assume they're stuck.

When employer-sponsored coverage terminates, that loss activates a sixty-day special enrollment window for Marketplace plans. Here's where numbers get interesting: your reduced income might qualify you for substantial subsidies unavailable while employed. That $500 monthly Silver plan could drop to $75 after tax credits once your income falls from $65,000 down to $30,000.

Medicaid eligibility hinges completely on current monthly income, not what you earned half a year ago. Lost your $60,000 position? Currently making $20,000 in unemployment benefits (unemployment income counts toward calculations), you might qualify for Medicaid in expansion states. Apply through your state's program or via the Marketplace—applications automatically verify Medicaid eligibility first and redirect you when appropriate.

Spouse carries employer coverage? Already married? Join their plan mid-year because your coverage loss counts as a qualifying event for them. Haven't married yet? Getting married itself opens special enrollment for both partners. Adult children can remain on parental plans until their 26th birthday without questions about employment, student enrollment, or marital status.

Short-term plans cost considerably less because they cover considerably less. Expect $150-300 monthly for bare-bones coverage excluding pre-existing conditions, capping total benefits, and cherry-picking covered services. Broke your arm playing weekend softball? Covered. Need surgery for a condition diagnosed before the policy started? Denied. These work for healthy people expecting to secure comprehensive coverage within several months.

Author: Melissa Grant;

Source: blaverry.com

Health Insurance Options for Small Business Owners

Operating your own business—whether you're a solo freelancer or managing fifteen employees—opens specific coverage pathways.

The Small Business Health Options Program (SHOP) allows businesses with 1 to 50 employees to purchase group coverage. Companies with fewer than 25 full-time equivalent employees earning average wages below $61,000 might qualify for the Small Business Health Care Tax Credit, covering up to 50% of premium costs for two consecutive years.

Sole proprietors without employees usually find better deals buying individual coverage through the Marketplace. The key benefit: the self-employed health insurance deduction allows writing off 100% of premiums when calculating self-employment tax. This deduction appears on your Schedule 1 (Form 1040), reducing adjusted gross income even without itemizing other deductions. Say you're paying $600 monthly for family coverage—that's $7,200 annually reducing taxable income.

Some trade associations and professional groups offer association health plans to members. The National Association for the Self-Employed, Freelancers Union, and industry-specific organizations sometimes negotiate group rates. These plans aren't universally available and vary wildly in quality and cost, but they're worth investigating within your field.

Business owners with employees face a choice: offer group coverage or not? Companies below 50 full-time employees face no legal requirement to provide insurance. Strong benefits attract better talent though. Some small businesses use Health Reimbursement Arrangements (HRAs) instead, reimbursing employees for premiums they pay on individual plans purchased through the Marketplace.

How to Shop for and Compare Health Insurance Plans

Comparing health plans demands looking past monthly premiums to understand total costs. Here's the systematic approach.

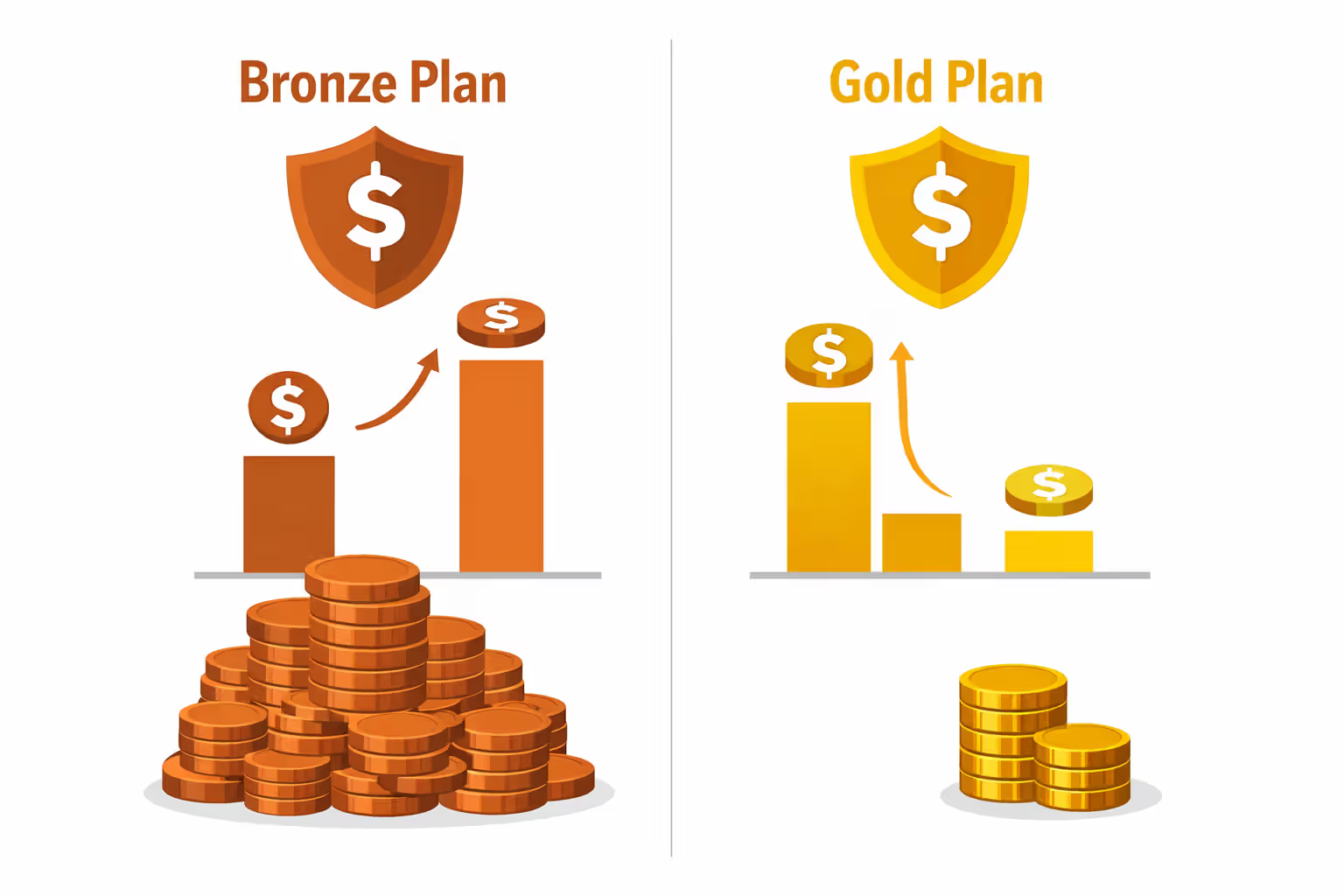

Step 1: Decode metal tiers. Marketplace plans arrive in Bronze, Silver, Gold, and Platinum categories. These tiers reflect actuarial value—the percentage the plan pays toward covered services. Bronze covers 60% on average (you're paying 40%), Silver covers 70%, Gold covers 80%, Platinum covers 90%. Higher metal tiers bring higher premiums but lower expenses when you actually use healthcare. There's also Catastrophic coverage for people under 30 or with hardship exemptions—rock-bottom premiums, sky-high deductibles, essentially disaster insurance.

Here's where it gets interesting: Silver plans unlock cost-sharing reductions when your income falls between 100% and 250% of federal poverty level. These CSRs reduce your deductibles, copays, and coinsurance beyond what premium tax credits provide. A Silver CSR plan might deliver superior coverage compared to Gold plans while costing less—but only when you qualify income-wise.

Step 2: Calculate actual annual costs. Monthly premiums mislead people. Add everything together: premium × 12 months + anticipated deductible + estimated copays and coinsurance + prescription costs. Example: Bronze plan at $250 monthly with $7,000 deductible versus Gold plan at $450 monthly with $1,500 deductible. You're seeing your doctor monthly, need a specialist quarterly, and take two prescriptions. Run those visits through each plan's cost-sharing structure. The Gold plan might actually cost $1,200 less annually despite higher premiums.

Author: Melissa Grant;

Source: blaverry.com

Step 3: Verify your doctors accept the network. This step trips up countless people every year. Don't trust online directories—call your doctor's office directly. Ask specifically: "Do you accept

?" Networks shift yearly. Last year's participation means nothing now. Check your preferred hospital too, especially when you have planned surgeries. Out-of-network care in an HMO plan? You're paying full cost except emergencies. PPO plans cover out-of-network providers at reduced rates, maybe 50-60% instead of 80%. EPO plans fall between HMO and PPO—no referrals needed but zero out-of-network coverage.Step 4: Review prescription formularies. Look up every medication you take regularly in each plan's formulary (drug list). Medications get organized into pricing tiers: Tier 1 typically covers generics with lowest copays, Tier 2 handles preferred brands, Tier 3 addresses non-preferred brands, Tier 4 deals with specialty medications. Your blood pressure medication might cost $10 monthly on one plan's Tier 1 and $75 monthly on another's Tier 3. Some plans demand prior authorization or step therapy (attempting cheaper alternatives first) for certain medications.

Step 5: Compare additional features. What's the deductible—the amount you're paying before insurance starts covering things? What's the out-of-pocket maximum—your annual spending cap after which insurance pays 100%? Are specific services you need covered? How does the plan handle telehealth visits? Some plans bundle dental and vision coverage, gym membership reimbursements, or wellness programs.

The Marketplace comparison tool displays plans side-by-side. Filter by network inclusion of your doctors, metal tier, and premium range. State marketplaces often provide superior comparison features compared to HealthCare.gov—more filtering options, clearer cost estimates, better formulary tools.

What Type of Health Insurance You Should Get

Your health status, budget, and risk tolerance determine which plan makes sense. Let's examine scenarios.

You're healthy and rarely visit doctors: Bronze plans or catastrophic coverage keep monthly costs low while protecting against worst-case disasters. You'll pay more when you do need care—that $7,500 deductible stings if you break your leg skiing—but you're wagering on staying healthy. Maximize savings by pairing with an HSA-eligible high-deductible plan, where you stash pre-tax money for medical expenses. Those HSA contributions reduce taxable income while building a medical emergency fund.

You have chronic conditions or see doctors regularly: Gold or Platinum plans usually cost less overall. Say you're diabetic: monthly endocrinologist visits, quarterly A1C tests, daily medications. A Bronze plan's $600 deductible seems appealing until you realize you're hitting that deductible by February then paying 40% coinsurance all year. Gold plans charge higher premiums but you might spend $3,000 less annually in total costs.

Your income qualifies for cost-sharing reductions: Silver plans with CSRs beat everything else. Earning $32,000 as a single person, you qualify for enhanced Silver coverage that lowers deductibles and copays dramatically—sometimes reducing a $4,000 deductible down to $500. This extra help only applies to Silver tier plans, making them superior coverage compared to Gold while costing less after subsidies.

You're covering your family: Consider split strategies. Put the family member with ongoing health needs on a comprehensive plan while covering healthy kids on a lower-tier plan. Some families qualify for CHIP for their children while parents buy Marketplace coverage. Check whether your employer's family coverage actually saves money versus splitting coverage—sometimes individual Marketplace plans with subsidies cost less than employer family plans.

Provider choice matters to you: PPOs let you see out-of-network doctors at reduced coverage rates—you'll pay more but you have flexibility. HMOs require staying in-network except for emergencies, usually charging nothing or nominal copays for out-of-network care. EPOs need no referrals like PPOs but provide zero out-of-network coverage like HMOs (except emergencies). POS plans blend HMO and PPO features, requiring referrals but offering some out-of-network coverage.

Budget reality check: Can you actually pay a $6,000 deductible if something unexpected happens tomorrow? Do you have emergency savings covering the out-of-pocket maximum? A "better" plan on paper doesn't help when you can't afford to use it because you're avoiding care due to cost-sharing.

Author: Melissa Grant;

Source: blaverry.com

Steps to Apply for Health Insurance

Applications vary by coverage source but follow similar patterns. Here's the walkthrough.

For Marketplace coverage:

Step 1: Set up an account at HealthCare.gov or your state's marketplace website. You'll provide an email and create login credentials for accessing your account later.

Step 2: Fill out the household application. You're answering questions about household size, expected annual income, current coverage status, citizenship, and whether anyone in your household has access to other coverage. The application takes 30-60 minutes typically. Save your progress when you need to dig up information—you don't have to finish in one sitting.

Step 3: Review eligibility results immediately. The system calculates whether you qualify for Medicaid, CHIP, or premium tax credits. Your estimated monthly subsidy appears right there, showing what you'll actually pay after assistance.

Step 4: Browse available plans in your area. Use filters to narrow by your doctors, metal tier, monthly cost, or deductible amount. Read plan details carefully—really carefully. Check provider directories, formularies, and benefits summaries.

Step 5: Select your plan and finish enrollment. Critical point here: pay your first month's premium directly to the insurance company (not the Marketplace). You'll receive payment instructions separately. Miss that payment deadline and your coverage never activates despite enrolling.

Required documentation includes proof of income like recent pay stubs, last year's tax return, W-2 forms, or profit-and-loss statements for self-employed individuals. You'll need Social Security numbers for everyone applying. If anyone isn't a U.S. citizen, bring immigration documents. Current health insurance information helps but isn't always required. The system verifies most information electronically, so you typically won't upload documents unless it flags inconsistencies needing verification.

For employer-based coverage: Contact human resources for enrollment paperwork and deadlines. You'll choose between plan options if multiple are offered, decide on dependent coverage, set beneficiaries, and authorize paycheck deductions. New employees usually enroll within 30 days of hire.

For Medicaid: Applications go through your state's Medicaid agency, the Marketplace, or in-person at county social service offices. Processing takes several weeks in most states. Some states provide emergency Medicaid coverage immediately for urgent medical situations while processing regular applications.

About premium subsidies: Your tax credit calculations use your estimated income for the coverage year—not last year's income. Estimate as accurately as possible. When you file taxes, you'll reconcile the difference between your estimated income and actual income. Earned more than expected? You might owe some subsidy repayment (though repayment caps exist). Earned less? You'll get additional credit money back. Update your Marketplace application whenever your income changes significantly during the year to adjust subsidies and avoid tax-time surprises.

Most plans start on the first day of whatever month follows your enrollment. Enroll December 10, coverage begins January 1. Enroll January 20, coverage starts February 1. The earlier you enroll after becoming eligible, the shorter your coverage gap.

Common Mistakes When Getting Health Insurance

The biggest mistake I see people make is waiting until they're sick to think about health insurance. Understanding enrollment periods and subsidy eligibility before you need coverage gives you options and prevents gaps that can be both financially devastating and medically dangerous. Take the time to explore your choices during open enrollment—your future self will thank you

— Jennifer Martinez

Even informed shoppers make errors that cost serious money or create coverage gaps.

Missing deadlines tops the list. November 1 arrives and people think "I've got time" then suddenly it's January 20 and enrollment closed five days ago. Set phone calendar alerts for November 1 and December 10 (giving yourself buffer time before the December 15 deadline for January 1 coverage). Experience a qualifying life event? Don't procrastinate. You've got 60 days but why create unnecessary coverage gaps?

Assuming you don't qualify for financial help without actually checking. Families earning $100,000+ sometimes qualify for subsidies depending on household size and location. Always complete a Marketplace application to see your real costs with subsidies before buying directly from an insurance company.

Picking the cheapest monthly premium automatically backfires hard. That $180 monthly Bronze plan looks amazing compared to the $420 monthly Gold plan until you need your gallbladder removed and suddenly you're paying $7,500 out-of-pocket versus $1,800. Do the math on total annual costs, not just monthly premiums.

Trusting provider directories blindly leads to surprise bills six months later when you discover your cardiologist isn't actually in-network despite appearing in the online directory. Call providers directly. Confirm participation for your specific plan. Insurance companies are terrible at keeping directories current.

Overlooking prescription coverage details hits people with chronic conditions hard. You compared premiums and deductibles carefully but didn't check drug formularies. Now your three medications cost $400 monthly on this plan versus $85 monthly on the plan you didn't choose.

Forgetting to actually pay premiums. Sounds obvious, but enrollment isn't complete until you pay. The Marketplace forwards your information to the insurance company, but payment comes from you directly to them. Schedule automatic payments to prevent accidental lapses that leave you uninsured despite thinking you enrolled.

Not reporting income changes to the Marketplace creates tax problems. Got a raise? Lost your job? Picked up freelance income? Report changes within 30 days so your tax credits adjust appropriately. Otherwise you're either missing out on assistance you qualify for or receiving too much advance credit you'll repay at tax time.

Comparison of Health Insurance Sources

| Source | Who Qualifies | Monthly Cost Range | Enrollment Timing | Coverage Start Date |

| Marketplace Plans | Anyone lacking affordable employer coverage, Medicaid, or Medicare | $200-600 pre-subsidy; fluctuates significantly based on age, geography, and plan selection | November 1–January 15 annually; 60-day window following qualifying life events | First day of the month after you enroll (when enrolled by 15th of prior month) |

| Employer Plans | Employees and frequently their dependents at participating companies | $150-250 for individual coverage; employer shoulders majority of total premium | Upon hire (after waiting period); during company's annual enrollment window | First of month following completion of waiting period (typically 30-90 days) |

| Medicaid | Low-income individuals; thresholds differ by state (up to 138% poverty level in expansion states) | $0-50 monthly in most states; frequently entirely free | Year-round applications accepted | Frequently same month as application; may apply retroactively up to three months |

| Medicare | Individuals 65 or older; younger people with qualifying disabilities; end-stage renal disease patients | Part B: $174.70 monthly standard; Part D varies considerably; supplemental Medigap: $100-300 | Seven-month period surrounding 65th birthday initially; October 15–December 7 for annual modifications | Birthday month when enrolled during initial period |

| Private Insurance | Anyone; no restrictions regarding income or employment | $300-800+ depending on age and coverage level; no subsidies available | Available throughout the year from insurance carriers | Depends on company; typically first of following month |

| COBRA | Individuals recently losing employer-based coverage through job loss or reduced hours | Complete premium amount + 2% admin fee (typically $600-900 monthly for individuals) | Within 60 days following employer coverage loss | Applies retroactively to coverage termination date when elected within 60-day window |

Frequently Asked Questions About Getting Health Insurance

Health insurance protects against both medical disasters and financial catastrophes that could wipe out years of savings. Your specific path depends on whether you're employed, how much you earn, your health situation, and your timing.

Start by figuring out when you're actually allowed to enroll—those enrollment periods aren't suggestions. Then identify which coverage sources match your circumstances. Most people qualify for subsidies that make coverage far more affordable than they assume. Take time comparing plans based on total annual spending, not just monthly premiums. Confirm your doctors participate in whichever plan network you're considering. Double-check prescription coverage if you take medications regularly.

Mark every deadline in multiple places—your phone calendar, email reminders, sticky notes on your bathroom mirror if needed. Missing open enrollment means months without coverage. When your life circumstances change, report updates to the Marketplace promptly to keep subsidies accurate and prevent tax complications.

The system rewards people who understand the rules and plan ahead. Healthcare decisions made during open enrollment affect your finances and wellbeing for an entire year.

Whether this is your first time shopping for coverage, you're between jobs, or you're reassessing what you currently have, investing a few hours into research and comparison pays off enormously. Health insurance isn't about checking a compliance box—it's about ensuring you can access medical care when you need it without facing bankruptcy. Make informed choices, respect deadlines, and reach out to navigators, brokers, or your state marketplace's help programs if you're feeling overwhelmed. These resources exist specifically to guide people through this process at no cost to you.