Stethoscope lying on a stack of dollar bills next to a health insurance policy document and a small calculator on a light blue medical background

What Is a Health Insurance Premium

Content

A health insurance premium is the amount you pay—typically every month—to keep your health insurance policy active, regardless of whether you visit a doctor or use any medical services. Think of it as a membership fee that maintains your access to coverage. Miss a payment, and your insurer can cancel your policy, leaving you responsible for the full cost of any medical care.

More than 150 million Americans receive coverage through employer-sponsored plans, while roughly 21 million purchase individual policies through marketplaces or directly from insurers. Each of these people pays a premium, though the amounts vary dramatically based on factors like age, location, and plan design. Understanding how premiums work—and what drives their cost—helps you make smarter decisions during open enrollment and avoid overpaying for coverage you don't need or underbuying protection that leaves you financially exposed.

How Health Insurance Works

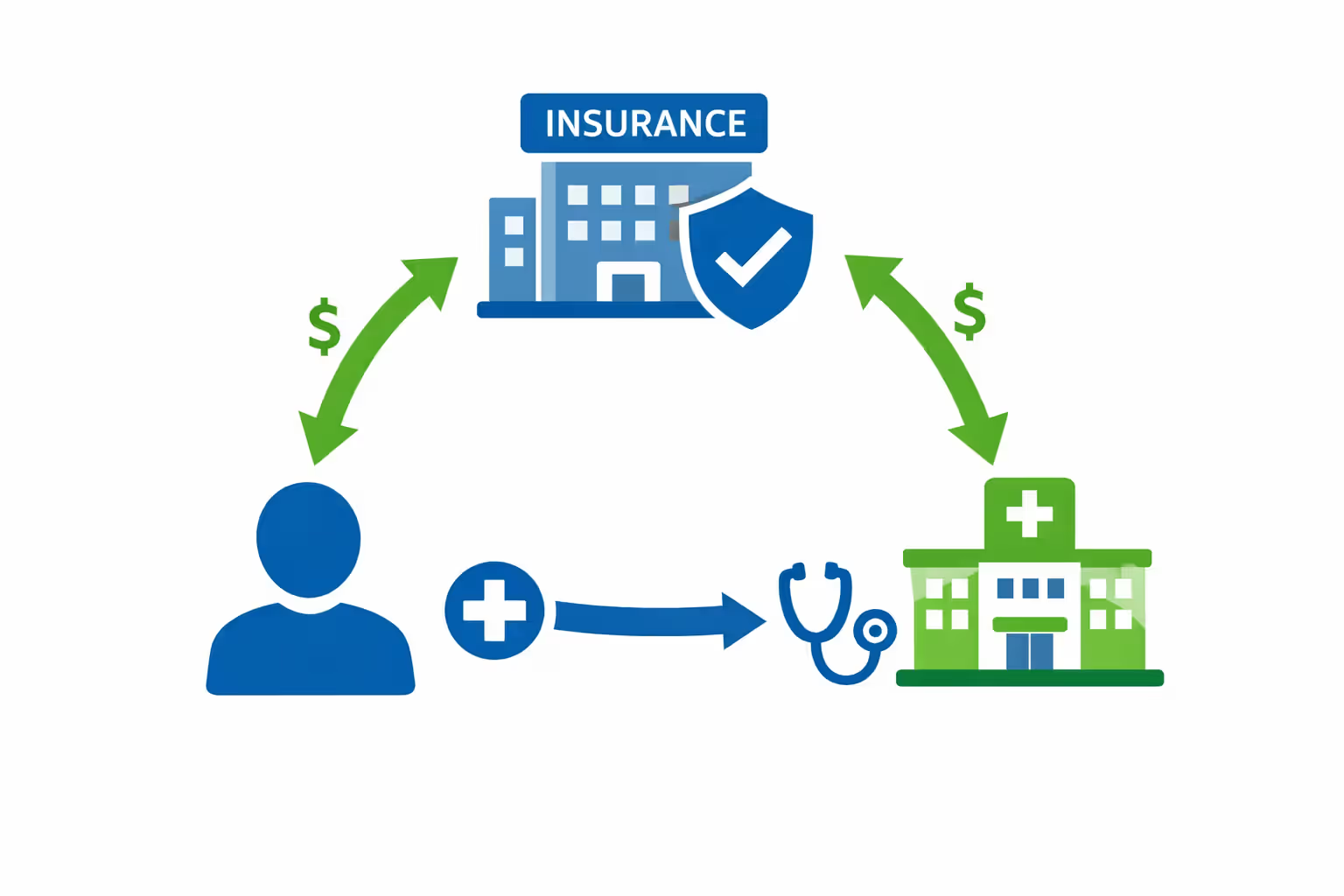

Health insurance is a contract between you and an insurance company. You agree to pay premiums, and the insurer agrees to cover a portion of your medical expenses according to the terms of your policy. The definition of health insurance centers on this risk-sharing arrangement: you pay predictable monthly amounts, and the insurer absorbs the unpredictable costs of illness, injury, and preventive care.

When you visit a doctor or hospital, the provider bills your insurance company. Your insurer processes the claim, applies any deductibles or copays you owe, then pays its share directly to the provider. This system protects you from catastrophic bills—a three-day hospital stay can easily exceed $30,000, but your out-of-pocket cost might be a few thousand dollars or less, depending on your plan.

Author: Derek Whitmore;

Source: blaverry.com

Most plans cover preventive services like annual checkups, vaccinations, and certain screenings at no cost to you, even before you meet your deductible. This encourages early detection and reduces long-term costs for both you and the insurer. Beyond preventive care, coverage kicks in for everything from prescription drugs to emergency room visits, though you'll typically share costs through deductibles, copays, and coinsurance until you hit your plan's out-of-pocket maximum.

Understanding Your Health Insurance Premium

A health insurance premium is the fixed payment you make to maintain active coverage. Most people pay monthly, though some insurers offer quarterly or annual payment options, sometimes with a small discount for paying upfront. The premium is non-negotiable once you've enrolled—you can't lower it mid-year by promising to stay healthy or avoid the doctor.

What does your premium actually cover? It pays for the insurer's administrative costs, claims processing, network negotiations with hospitals and doctors, and the pooled risk of covering everyone in your plan. Crucially, it also funds the medical care of sicker members. Health insurance works because healthy people subsidize those who need expensive treatments, spreading financial risk across a large group.

The premium in health insurance is separate from the costs you pay when you actually use care. If your monthly premium is $450 and you never see a doctor all year, you've still paid $5,400 to maintain coverage. That might feel wasteful, but it protects you from bankruptcy if you're diagnosed with cancer or injured in an accident. The premium is your ticket to coverage; other costs come into play only when you need services.

One common confusion: people assume a higher premium means better coverage or lower out-of-pocket costs. That's often true, but not always. A plan with a $600 monthly premium might have a $1,000 deductible, while a $400 premium plan could carry a $6,000 deductible. The premium is just one piece of your total cost picture.

Author: Derek Whitmore;

Source: blaverry.com

What Affects Your Premium Cost

Health insurance premiums vary widely based on factors insurers are legally allowed to consider. Two people in the same household can pay different amounts for the same plan if they differ in age or tobacco use. Understanding these variables helps you anticipate costs and identify opportunities to save.

Age and Location

Age is the single biggest factor in premium pricing. Insurers can charge older adults up to three times more than younger enrollees for the same plan. A 25-year-old in Phoenix might pay $320 monthly for a Silver plan, while a 60-year-old in the same city could pay $960 for identical coverage. This reflects the reality that older people use more medical services and face higher treatment costs.

Location matters almost as much. Premiums in rural Wyoming often run 40% higher than in urban areas of California, even after adjusting for age. Why? Fewer hospitals and doctors mean less competition, and insurers have less negotiating leverage. State regulations also play a role—some states allow more plan variation or have different mandates that affect pricing. Moving across a county line can sometimes change your premium by $100 or more per month.

Plan Type and Coverage Level

The Affordable Care Act established four metal tiers—Bronze, Silver, Gold, and Platinum—that determine how costs are split between you and your insurer. Bronze plans have the lowest premiums but cover only about 60% of medical costs on average, leaving you to pay 40% through deductibles and coinsurance. Platinum plans carry the highest premiums but cover roughly 90% of costs, minimizing what you pay when you need care.

Plan type also affects premiums. HMOs (Health Maintenance Organizations) typically cost less than PPOs (Preferred Provider Organizations) because they restrict you to a narrower network and require referrals to see specialists. EPOs (Exclusive Provider Organizations) fall somewhere in between. If you rarely need care and want the flexibility to see any doctor, a PPO's higher premium might frustrate you. If you have chronic conditions and see specialists regularly, that same premium could save you thousands in out-of-network charges.

Tobacco Use and Family Size

Insurers can charge tobacco users up to 50% more than non-users, though some states limit this surcharge. A $400 monthly premium can jump to $600 if you smoke, vape, or use other tobacco products. Quitting for at least six months usually qualifies you for non-tobacco rates, though you'll need to certify your status when you enroll.

Family size directly impacts premiums because you're buying coverage for multiple people. Adding a spouse might increase your monthly cost by $350, and each child could add $150 to $250, depending on their ages. Some employer plans charge a flat family rate regardless of whether you're covering two people or five, but individual market plans price each person separately. A family of four can easily face premiums exceeding $1,500 per month before any subsidies.

Premium vs. Deductible vs. Out-of-Pocket Costs

Many people confuse premiums with other health insurance costs, leading to poor plan choices. Here's how the main terms differ:

| Term | What It Is | When You Pay | Example |

| Premium | Fixed monthly fee to keep coverage active | Every month, whether you use care or not | $450/month for a Silver plan |

| Deductible | Amount you pay for covered services before insurance starts sharing costs | Per year, resets January 1; you pay until you hit the limit | $3,000 deductible means you pay the first $3,000 of non-preventive care |

| Copay | Fixed fee for specific services | Each time you use that service | $30 for a primary care visit, $75 for urgent care |

| Coinsurance | Percentage of costs you pay after meeting your deductible | After deductible is met, until you hit out-of-pocket max | 20% coinsurance means you pay $200 of a $1,000 procedure; insurer pays $800 |

| Out-of-Pocket Maximum | Cap on what you pay in a year (excludes premiums) | Accumulates throughout the year; once hit, insurer pays 100% | $8,000 max means after you've paid $8,000 in deductibles, copays, and coinsurance, everything else is free |

The relationship between these costs defines your financial exposure. A plan with a $300 premium, $5,000 deductible, and $8,500 out-of-pocket max could cost you $12,100 in a year if you need surgery ($3,600 in premiums plus $8,500 in medical costs). A plan with a $550 premium, $1,500 deductible, and $6,000 max might cost you $12,600 in the same scenario ($6,600 in premiums plus $6,000 in medical costs). The "cheaper" premium plan actually costs less if you have major medical expenses.

What is premium health insurance in this context? It's not necessarily the most expensive plan—it's the plan that offers the best balance of upfront costs and financial protection for your specific health needs and budget.

How to Lower Your Health Insurance Premium

Premium costs feel fixed, but several strategies can reduce what you pay each month.

Premium tax credits (also called subsidies) are available to individuals and families earning between 100% and 400% of the federal poverty level who buy coverage through the Health Insurance Marketplace. For 2026, that's roughly $15,000 to $60,000 for a single person, or $31,000 to $124,000 for a family of four. These credits apply directly to your monthly premium, sometimes cutting costs by hundreds of dollars. You claim them when you enroll, and the government pays your insurer directly. If your income falls near a subsidy threshold, even small changes—like contributing more to a 401(k)—can increase your credit.

Employer contributions cover an average of 70-85% of premium costs for workers who get job-based coverage. If your employer offers a health plan, you're almost always better off taking it than buying individual coverage, even if the employer plan seems expensive. A $200 monthly employee contribution might represent a $1,000 total premium, with your employer paying the other $800.

Choosing a higher deductible lowers your premium but increases your risk. Bronze and catastrophic plans (available to people under 30 or those with hardship exemptions) carry the lowest premiums but the highest deductibles—sometimes $7,000 or more. This makes sense if you're healthy, have savings to cover the deductible, and want protection against worst-case scenarios. It's a bad choice if you take expensive medications or have planned procedures, because you'll pay full price until you meet that deductible.

HSA-compatible high-deductible plans offer a unique advantage: you can contribute pre-tax dollars to a Health Savings Account, reducing your taxable income while building a fund for medical expenses. For 2026, individuals can contribute up to $4,300 and families up to $8,550. If you're in the 22% tax bracket, a $4,000 HSA contribution saves you $880 in federal taxes, effectively lowering your net health insurance cost.

I see clients fixate on the monthly premium and ignore the deductible, then panic when they owe $4,000 before insurance pays a dime. The right plan isn't the one with the lowest premium—it's the one where your total annual cost, including expected medical expenses, fits your budget and risk tolerance

— Sarah Mitchell

Comparing plans annually matters because premiums, networks, and coverage change every year. The Gold plan that was a great deal last year might have increased by 15% while a different insurer's Silver plan stayed flat. Marketplace open enrollment runs from November 1 to January 15, and most employer open enrollments happen in October or November. Block out an hour to compare at least three plans, factoring in your expected doctor visits, prescriptions, and any planned procedures.

Common Premium Mistakes to Avoid

Even financially savvy people make errors when choosing health insurance. Here are the costliest:

Picking the lowest premium without checking the deductible. A plan that saves you $100 monthly but adds $3,000 to your deductible costs you more if you need any significant care. Run the math: multiply the monthly savings by 12, then compare it to the deductible difference. If the deductible gap is larger, you're gambling that you won't need care.

Ignoring subsidies. Roughly 40% of Marketplace-eligible people don't realize they qualify for premium tax credits. If you're self-employed, between jobs, or working part-time, check HealthCare.gov during open enrollment. A family earning $75,000 might qualify for $400+ in monthly credits, turning a $1,200 premium into $800.

Not comparing plans annually. Insurers adjust premiums, networks, and formularies every year. Your current plan might drop your specialist or move your medication to a higher cost tier. Switching plans takes 20 minutes and can save you thousands.

Misunderstanding what the premium pays for. Your monthly payment keeps your coverage active, but it doesn't directly pay for your care—that comes from the pooled funds of all enrollees. Some people skip preventive visits because "I'm already paying the premium," not realizing those visits are free and can catch problems early when they're cheaper to treat.

Dropping coverage to save money. Going uninsured might save you $300-$500 monthly, but a single emergency room visit can cost $3,000, and a hospital stay can exceed $50,000. You also face a gap in coverage that can trigger medical underwriting questions or waiting periods if you try to re-enroll later (though ACA plans can't deny you for pre-existing conditions, timing your enrollment outside open enrollment requires a qualifying life event).

Author: Derek Whitmore;

Source: blaverry.com

Frequently Asked Questions About Health Insurance Premiums

Your health insurance premium is the foundation of your coverage—the non-negotiable cost of maintaining access to care. While it's tempting to focus solely on finding the lowest monthly payment, smart consumers balance premium costs against deductibles, out-of-pocket maximums, and network quality. A plan that saves you $75 monthly but costs $3,000 more when you actually need care isn't a bargain.

Start by estimating your annual medical expenses: regular prescriptions, expected doctor visits, planned procedures. Compare at least three plans, calculating total annual cost (premiums plus expected out-of-pocket spending) for each. Check whether you qualify for subsidies, and don't overlook HSA-compatible plans if you're comfortable with higher deductibles and want tax advantages.

The right health insurance premium is the one that gives you adequate protection without straining your budget. Review your coverage every year during open enrollment, adjust as your health needs change, and remember that the best plan isn't always the cheapest—it's the one that covers you when it matters most.