Person holding health insurance policy document with stethoscope, calculator and dollar bills on a bright office desk

What Is Full Coverage Health Insurance

Content

When shopping for health insurance, you've probably heard the term "full coverage" thrown around by agents, coworkers, or advertisements. It sounds reassuring—like a safety net that catches every medical expense. But what does full coverage health insurance actually mean, and does it live up to the promise its name suggests?

The reality is more nuanced than most people expect. Understanding what this term really represents can save you from surprise bills and help you choose a plan that genuinely fits your healthcare needs and budget.

Understanding Full Coverage Health Insurance

Here's something most insurance companies won't lead with: "full coverage health insurance" isn't an official category recognized by the Centers for Medicare & Medicaid Services or any state insurance department. Instead, it's industry shorthand—a marketing-friendly term that typically describes plans with comprehensive benefits and lower out-of-pocket costs compared to high-deductible or catastrophic options.

When someone refers to full coverage health insurance, they usually mean a plan that covers a wide range of medical services with relatively predictable cost-sharing. These plans often feature lower deductibles, reasonable copays for doctor visits, and coverage that kicks in before you've spent thousands of dollars on care.

The full coverage health insurance meaning has evolved to represent policies that protect you from both routine healthcare costs and major medical expenses. Unlike bare-bones plans that only cover emergencies or serious illnesses, comprehensive coverage helps pay for preventive care, specialist visits, prescription medications, and mental health services—the everyday healthcare needs most Americans face.

A common misconception: people assume "full coverage" means zero out-of-pocket costs. That's rarely true. Even the most generous employer-sponsored plans require some cost-sharing through premiums, deductibles, copays, or coinsurance. The "full" part refers to the breadth of services covered, not the elimination of all personal financial responsibility.

Another point of confusion—full coverage health insurance explained simply means you're getting robust benefits across multiple categories of care, but it doesn't guarantee that every possible medical service or treatment will be covered. Experimental procedures, cosmetic treatments, and certain alternative therapies typically remain excluded regardless of how comprehensive your plan appears.

What Full Coverage Health Insurance Typically Includes

A truly comprehensive plan covers the ten essential health benefits mandated by the Affordable Care Act, plus additional services that make healthcare more accessible and affordable throughout the year.

Services Usually Covered

Full coverage plans typically include hospitalization for surgeries, accidents, and serious illnesses. You'll have coverage for emergency room visits, ambulance services, and urgent care facilities—critical protections when health crises strike without warning.

Preventive care sits at the heart of these plans. Annual physicals, immunizations, cancer screenings, and wellness visits come at no cost beyond your premium, thanks to ACA requirements. Women's health services including mammograms and contraception, along with pediatric care like well-child visits, fall under this umbrella.

Prescription drug coverage usually spans multiple tiers, from generic medications to brand-name and specialty drugs. While you'll pay more for higher-tier medications, you won't face the full retail price that can reach hundreds or thousands of dollars per month.

Specialist visits—cardiologists, orthopedists, dermatologists, endocrinologists—are accessible with reasonable copays, often ranging from $40 to $80 per visit. Mental health and substance abuse services receive parity treatment, meaning therapy sessions and psychiatric care carry similar cost-sharing as physical health services.

Maternity and newborn care represent another major component. From prenatal visits through delivery and postpartum care, comprehensive plans cover the full pregnancy journey. Pediatric services extend this protection to your children, including dental and vision care up to age 19.

Laboratory tests, diagnostic imaging (X-rays, MRIs, CT scans), and rehabilitative services like physical therapy round out the typical health insurance full coverage package. Medical equipment and supplies, including wheelchairs, oxygen equipment, and diabetes testing supplies, also receive coverage.

Author: Melissa Grant;

Source: blaverry.com

What May Still Require Out-of-Pocket Costs

Even with comprehensive coverage, certain expenses fall outside the plan's scope or require significant cost-sharing. Adult dental and vision care rarely appear in standard health insurance policies—you'll need separate dental and vision plans for routine cleanings, glasses, or contact lenses.

Cosmetic procedures, fertility treatments beyond basic diagnostics, and weight-loss surgery (unless deemed medically necessary) typically require full out-of-pocket payment. Long-term care services, private nursing, and custodial care in nursing homes don't fall under health insurance coverage.

Out-of-network care presents another cost trap. Even full coverage health insurance examples show that visiting providers outside your plan's network can result in balance billing, where you're responsible for the difference between what your insurer pays and what the provider charges. This gap can reach thousands of dollars for a single hospital stay.

Brand-name drugs when generics are available, experimental treatments, and alternative medicine like acupuncture or chiropractic care beyond limited visits often require higher copays or full payment.

Full Coverage vs HMO and PPO Plans

Understanding the relationship between coverage comprehensiveness and plan structure helps clarify a common source of confusion. Full coverage isn't a plan type—it's a description of benefit generosity that can exist within different organizational frameworks like HMOs and PPOs.

An HMO (Health Maintenance Organization) requires you to choose a primary care physician who coordinates all your care and provides referrals to specialists. You must stay within the HMO's network except for emergencies, but in exchange, you typically enjoy lower premiums and minimal paperwork.

A PPO (Preferred Provider Organization) offers more flexibility. You can see any provider without referrals, visit out-of-network doctors (though at higher cost), and access specialists directly. This freedom comes with higher premiums and often larger deductibles.

Both HMO and PPO structures can offer full coverage health insurance vs hmo or full coverage health insurance vs ppo comparisons that show comprehensive benefits. An HMO plan might provide extensive coverage for all services—as long as you follow the network and referral rules. A PPO might offer the same comprehensive benefits with added flexibility to seek care outside the network.

The real question isn't "full coverage vs HMO or PPO" but rather "which plan structure delivers comprehensive benefits while matching my healthcare preferences and budget?"

| Plan Type | Provider Network Flexibility | Referral Requirements | Typical Monthly Premium Range (Individual) | Average Deductible | Best For |

| Full Coverage HMO | Low (in-network only) | Yes (PCP referral needed) | $450–$650 | $500–$1,500 | People who want comprehensive benefits, don't mind coordinated care, and prioritize lower costs |

| Full Coverage PPO | High (in and out-of-network) | No | $550–$850 | $1,000–$3,000 | Those who value provider choice, travel frequently, or see specialists regularly |

| Standard HMO | Low (in-network only) | Yes | $350–$500 | $1,500–$3,500 | Budget-conscious individuals comfortable with network restrictions |

| Standard PPO | High (in and out-of-network) | No | $450–$700 | $2,000–$5,000 | People wanting flexibility without maximum benefit comprehensiveness |

Premium and deductible ranges reflect 2026 marketplace averages for 30-year-old non-smokers; actual costs vary by location, age, and tobacco use.

How Full Coverage Health Insurance Works in Practice

How does full coverage health insurance work when you actually need medical care? The mechanics involve several cost-sharing components working together.

Your premium represents the monthly fee you pay simply to maintain coverage, regardless of whether you use medical services. Think of it as membership dues. For employer-sponsored plans, your company typically covers 70-80% of this cost, while you pay the remainder through paycheck deductions.

Author: Melissa Grant;

Source: blaverry.com

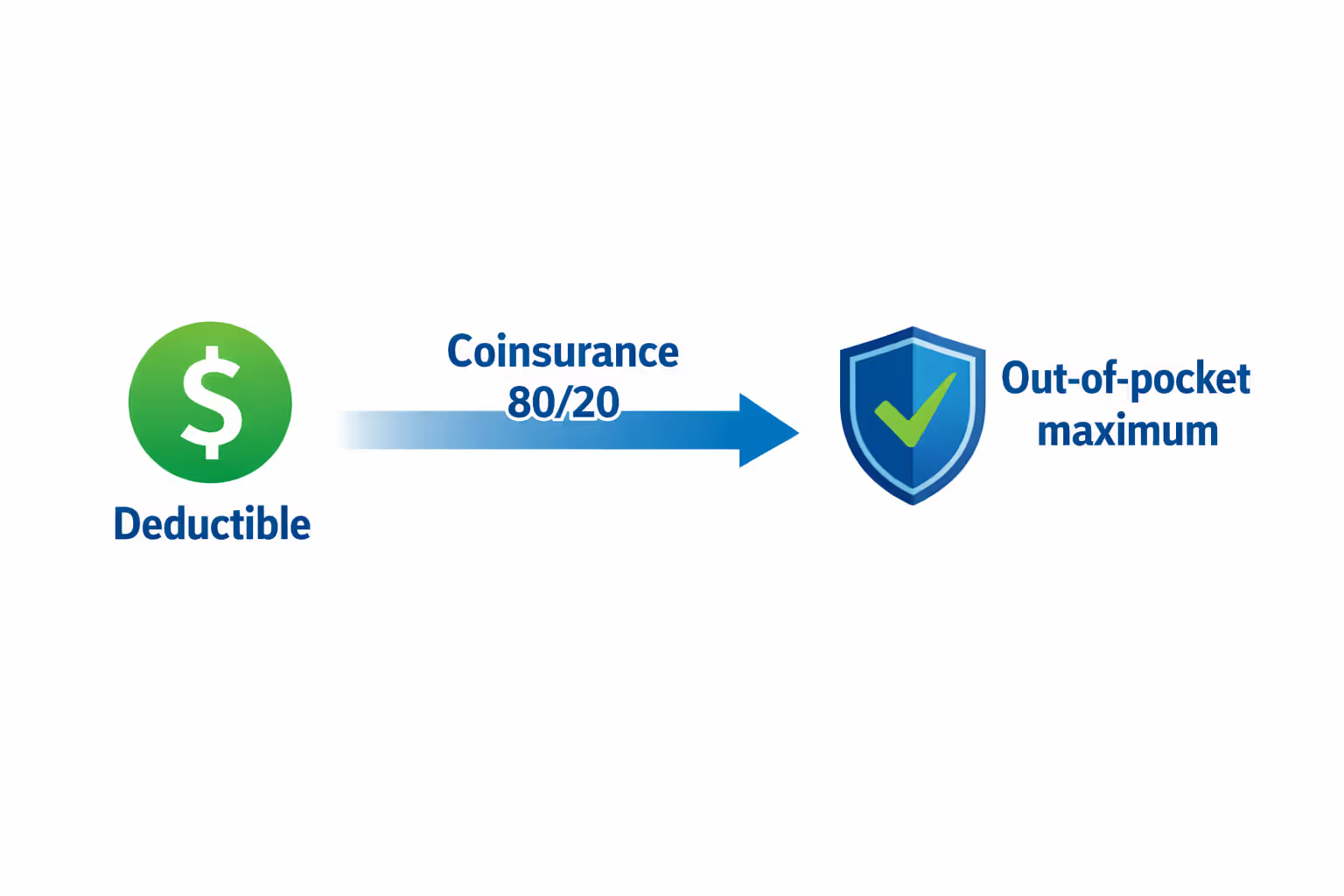

The deductible is the amount you must spend on covered services before your insurance begins sharing costs. With comprehensive plans, deductibles typically range from $500 to $2,000 for individuals. Some services—particularly preventive care—bypass the deductible entirely, meaning your insurance covers them from day one.

After meeting your deductible, cost-sharing continues through copays and coinsurance. A copay is a fixed amount ($25 for primary care, $50 for specialists, $15 for generic prescriptions) you pay at each visit or service. Coinsurance is a percentage split—you might pay 20% of the cost while insurance covers 80%.

The out-of-pocket maximum caps your annual spending on covered services. Once you reach this limit (often $5,000-$8,000 for individuals in comprehensive plans), your insurance pays 100% of covered costs for the rest of the year. Your premiums don't count toward this maximum, but deductibles, copays, and coinsurance do.

Here's a practical scenario: Sarah has full coverage health insurance for beginners through her employer. Her plan has a $1,000 deductible, $30 primary care copays, 20% coinsurance for hospital care, and a $6,000 out-of-pocket maximum.

In March, Sarah visits her doctor for a sinus infection ($30 copay). In June, she needs an MRI ($400, applied to her deductible). In August, she requires outpatient surgery costing $8,000. She's already met her $1,000 deductible, so she pays 20% coinsurance on the remaining $7,000—that's $1,400. Combined with her earlier expenses, she's spent $1,830 out-of-pocket. If she needs additional care, she'll continue paying 20% coinsurance until hitting her $6,000 maximum, after which the plan covers everything at 100%.

The term 'full coverage' creates an expectation of financial protection that doesn't always match reality. I advise clients to focus less on marketing language and more on three numbers: the deductible, the out-of-pocket maximum, and the premium. Those figures tell you exactly what you'll pay in both typical years and worst-case scenarios. A plan isn't truly comprehensive if accessing its benefits would bankrupt you

— Michael Chen

Who Should Consider Full Coverage Health Insurance

Comprehensive plans make financial sense for specific groups, while others might benefit from leaner options.

Families with children gain tremendous value from full coverage. Kids need regular well-child visits, immunizations, and occasional sick visits. When you multiply copays across multiple family members, plans with lower cost-sharing quickly pay for themselves despite higher premiums. Parents also appreciate the predictability—you can budget for healthcare costs without fearing a single illness will drain your savings.

People managing chronic conditions—diabetes, asthma, heart disease, autoimmune disorders—benefit enormously from comprehensive coverage. Regular specialist visits, ongoing medications, and monitoring tests add up quickly. A plan with a $600 monthly premium but $1,000 deductible and $30 specialist copays costs far less annually than a $400 premium plan with a $5,000 deductible when you're seeing doctors monthly.

Anyone anticipating major medical expenses should prioritize comprehensive benefits. Planning surgery, starting fertility treatments, or managing a recent diagnosis? Full coverage plans minimize your financial exposure during high-utilization periods.

Risk-averse individuals who value peace of mind over premium savings also gravitate toward these plans. If the thought of a surprise $3,000 bill causes significant stress, paying an extra $100 monthly for lower deductibles and copays might be worth it for psychological comfort alone.

Conversely, young, healthy adults with minimal healthcare needs might find comprehensive plans wasteful. If you visit the doctor once yearly for a physical and rarely need prescriptions, you're essentially paying for benefits you won't use. A high-deductible health plan paired with a health savings account offers lower premiums and tax advantages that better match your usage pattern.

Self-employed individuals and freelancers face a tougher calculation. Without employer subsidies, you're paying the full premium. Comprehensive plans can easily cost $700-900 monthly. You'll need to honestly assess your healthcare utilization and risk tolerance. Many opt for mid-tier plans that balance coverage and affordability rather than choosing the most comprehensive option.

Author: Melissa Grant;

Source: blaverry.com

Common Questions About Full Coverage Health Insurance

Choosing health insurance ranks among the most consequential financial decisions you'll make, yet it's one that most people approach with limited information and significant confusion. The term "full coverage" offers a helpful shorthand for comprehensive benefits, but it shouldn't be the only factor driving your decision.

Start by honestly assessing your healthcare utilization patterns. Review the past two years—how many doctor visits did you have? What prescriptions do you take regularly? Have you needed specialists, physical therapy, or emergency care? These patterns typically continue, making them reliable predictors of future needs.

Calculate the total cost of ownership for each plan option, not just the monthly premium. Add up premiums for the full year, then add your expected out-of-pocket costs based on typical usage. Include the worst-case scenario too—what would you pay if you hit the out-of-pocket maximum? This exercise reveals which plan truly costs less for your situation.

Consider your financial resilience. Could you handle a $3,000 surprise medical bill without derailing other financial goals? If not, comprehensive coverage with lower deductibles provides crucial protection. If you maintain a robust emergency fund, you might comfortably absorb higher cost-sharing in exchange for premium savings.

The right health insurance balances premium affordability, coverage comprehensiveness, and your personal healthcare needs. For some, that means embracing full coverage despite higher monthly costs. For others, a leaner plan with more cost-sharing makes better financial sense. Neither choice is inherently superior—the best plan is the one that protects your health and finances based on your unique circumstances.