Hands holding health insurance document on desk with calculator stethoscope and dollar bills

What Is High Deductible Health Insurance

Content

High deductible health insurance is a plan structure that requires you to pay a larger amount out of pocket before your insurer begins covering most medical expenses. In exchange for accepting this higher upfront financial responsibility, you typically pay lower monthly premiums compared to traditional plans.

The IRS defines specific thresholds that qualify a plan as a high deductible health plan (HDHP). For 2026, individual coverage must have a minimum deductible of $1,650, while family coverage requires at least $3,300. These plans also cap your total out-of-pocket spending at $8,300 for individuals and $16,600 for families.

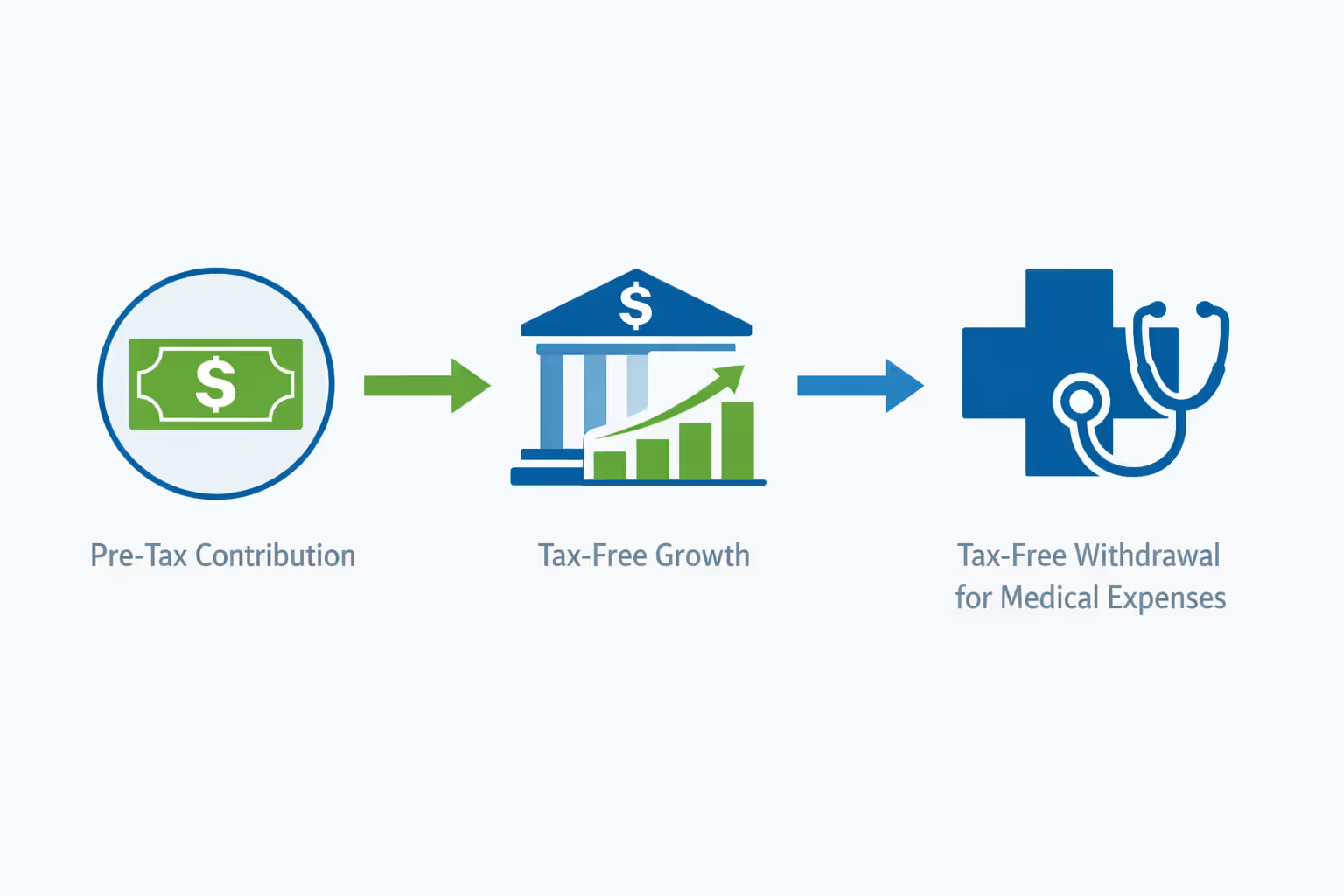

Beyond the basic definition, HDHPs offer a unique advantage: eligibility to open and contribute to a Health Savings Account (HSA). This tax-advantaged account lets you set aside pre-tax dollars specifically for medical expenses, creating a powerful financial tool that extends well beyond simple insurance coverage.

Understanding whether this plan type aligns with your healthcare needs and financial situation requires looking beyond premium savings alone. The structure fundamentally shifts when and how you pay for care, making it essential to evaluate your actual medical usage patterns, emergency fund status, and risk tolerance.

How High Deductible Health Insurance Works

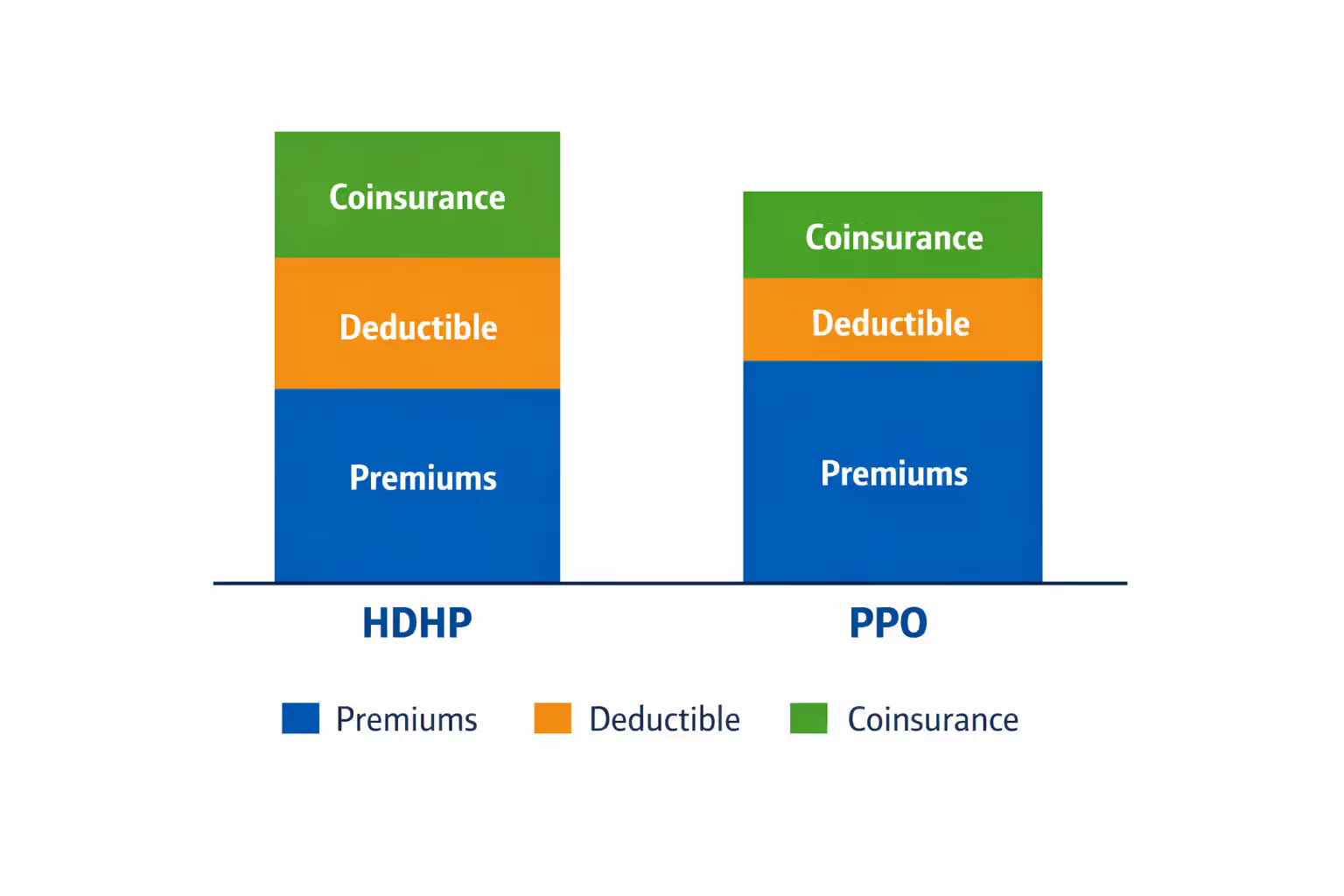

The mechanics of an HDHP differ substantially from traditional health plans. When you receive medical care, you pay the full negotiated rate your insurer has arranged with providers until you've spent enough to meet your deductible threshold. After crossing that line, your plan typically begins cost-sharing through coinsurance—commonly 80/20 or 70/30 splits where the insurer covers the larger percentage.

Consider a plan with a $2,500 deductible and 80/20 coinsurance. You break your arm and receive treatment costing $4,000. You'll pay the first $2,500 to meet your deductible, then 20% of the remaining $1,500 ($300), totaling $2,800 out of pocket for that incident.

Monthly premiums for HDHPs run significantly lower than comparable PPO or HMO options. Where a traditional PPO might cost $550 monthly, an HDHP from the same insurer could run $325—a difference of $2,700 annually. This premium savings becomes your primary financial benefit, but only if you can manage the deductible when medical needs arise.

The HSA component adds another dimension. For 2026, you can contribute up to $4,300 as an individual or $8,550 for family coverage. These contributions reduce your taxable income, grow tax-free, and can be withdrawn without taxes for qualified medical expenses. Unlike flexible spending accounts, HSA balances roll over indefinitely, functioning as a healthcare-specific investment account.

Author: Lauren Prescott;

Source: blaverry.com

One critical protection: all HDHPs must cover preventive care at no cost before you meet your deductible. Annual physicals, immunizations, cancer screenings, and other preventive services defined by the Affordable Care Act remain fully covered. This provision ensures you can maintain basic health monitoring without financial barriers.

The coverage activation point matters tremendously. If you need a $15,000 surgery in January and your deductible is $3,000, you'll pay that $3,000 plus your coinsurance share of the remaining balance. But if you spread smaller medical expenses throughout the year and never hit your deductible, you'll pay full price for each visit, prescription, and test.

Who Should Consider a High Deductible Plan

HDHPs work best for specific financial and health profiles. Young, healthy individuals who rarely visit doctors beyond annual checkups often benefit most. If your typical year involves one physical and perhaps an urgent care visit for flu symptoms, paying $2,000 less in premiums while risking a $2,500 deductible creates favorable math.

People with substantial emergency savings find HDHPs less risky. Having $5,000 to $10,000 set aside specifically for unexpected medical costs means the deductible represents an inconvenience rather than a financial crisis. Without this cushion, a single emergency room visit could trigger debt or force impossible choices about seeking care.

Strategic HSA users gain compounding advantages. If you can afford to pay medical expenses from regular income while letting HSA contributions grow untouched, you're essentially building a tax-advantaged investment account. After age 65, HSA withdrawals for non-medical expenses face only income tax (no penalty), functioning like a traditional IRA with the bonus of tax-free medical spending at any age.

Author: Lauren Prescott;

Source: blaverry.com

Families with healthy children who need mainly preventive care—well-child visits, vaccinations, occasional strep throat treatment—often find HDHPs economical. The premium savings can fund 529 college accounts or other family priorities while the HSA covers predictable minor expenses.

Conversely, several groups should approach HDHPs cautiously. People managing chronic conditions requiring regular specialist visits, ongoing prescriptions, or frequent monitoring face nearly guaranteed deductible hits. Paying full price for monthly endocrinologist appointments and diabetes supplies until meeting a $3,000 deductible erases premium savings quickly.

Those living paycheck to paycheck without emergency reserves risk delaying necessary care. When a potential $2,000 deductible stands between you and addressing chest pain or investigating persistent symptoms, the financial barrier becomes a health hazard.

Individuals who value predictable budgeting may find HDHPs stressful. Traditional copay-based plans let you know each doctor visit costs $30 and prescriptions run $15. HDHPs create variable monthly healthcare spending that complicates budgeting, especially early in the year before meeting the deductible.

The biggest mistake I see is people choosing HDHPs purely based on premium savings without honestly assessing their ability to handle a $3,000 or $5,000 surprise expense. The plan works beautifully for disciplined savers who can fund an HSA and maintain separate emergency reserves, but it becomes a trap for families already financially stretched

— Lisa Thornton

High Deductible Plans vs HMO and PPO

Understanding how HDHPs compare to HMO and PPO structures helps clarify which approach matches your priorities. These plan types differ fundamentally in cost distribution, provider flexibility, and administrative requirements.

| Plan Type | Average Monthly Premium | Typical Deductible Range | Network Flexibility | Referral Requirements | Best For Whom |

| HDHP | $320-$420 | $1,650-$5,000 | Usually PPO-style network | Rarely required | Healthy individuals, HSA savers, low healthcare users |

| HMO | $380-$480 | $500-$1,500 | Strict network only | Required for specialists | Budget-conscious with primary care focus |

| PPO | $480-$620 | $500-$2,000 | In/out-of-network options | Not required | Those wanting provider choice and flexibility |

Premium and deductible ranges reflect 2026 individual coverage averages in mid-sized US markets

HMO plans emphasize coordinated care through your primary care physician, who acts as a gatekeeper for specialist access. You'll pay moderate premiums and low copays but sacrifice provider choice and must stay within network for coverage (except emergencies). The structure works well when you have an established primary doctor and don't mind the referral process.

PPO plans maximize flexibility, allowing you to see specialists without referrals and providing partial coverage for out-of-network providers. You'll pay the highest premiums but enjoy predictable copays and moderate deductibles. This approach suits people who value choice, travel frequently, or have established relationships with specific specialists.

HDHPs occupy a different space entirely. Rather than emphasizing care coordination (HMO) or provider freedom (PPO), they shift financial responsibility toward the member in exchange for lower premiums and HSA access. Most HDHPs use PPO-style networks without referral requirements, but the cost structure creates different decision-making dynamics.

Key Differences in Cost Structure

The fundamental financial distinction lies in when you pay. HMO and PPO plans spread costs through higher premiums plus modest copays for each service. An HMO member might pay $450 monthly and $30 per office visit. Across a year with six visits, total spending reaches $5,580 ($5,400 premiums plus $180 in copays).

An HDHP member with a $2,000 deductible might pay $350 monthly and full price for those six visits—perhaps $150 each if negotiated rates run that high. Annual spending totals $5,100 ($4,200 premiums plus $900 toward the deductible). The HDHP saves $480 in this scenario, plus any HSA tax benefits from contributing that $900.

But change the scenario to fifteen visits, several specialist consultations, and a $3,000 MRI. The HMO member pays $5,400 in premiums plus perhaps $750 in copays ($6,150 total). The HDHP member pays $4,200 in premiums, meets the $2,000 deductible, then pays 20% coinsurance on remaining expenses. Total out-of-pocket could easily reach $6,500 or more, erasing the premium advantage.

The break-even point varies by specific plan details, but a useful rule of thumb: if you anticipate significant medical utilization exceeding routine preventive care, traditional plans often cost less overall despite higher premiums.

Author: Lauren Prescott;

Source: blaverry.com

When Each Plan Type Makes Sense

Choose an HDHP when you're healthy, financially stable, and want to maximize HSA contributions. The plan structure rewards low utilization and benefits those who can absorb occasional high costs without financial strain. It's particularly valuable if you're building long-term tax-advantaged healthcare savings rather than just buying insurance.

Select an HMO when you prioritize low per-visit costs and don't mind coordinated care requirements. These plans work well for families with children needing frequent pediatrician visits, or anyone who wants predictable copays and doesn't need specialist access without referrals. The premium sits between HDHP and PPO rates while providing better cost protection than HDHPs for regular users.

Pick a PPO when you need provider flexibility, see multiple specialists, or want coverage while traveling. The higher premiums buy freedom from referrals and network restrictions. People with complex medical conditions requiring care coordination across multiple specialists often find PPO structures worth the extra cost.

Real-World Examples of High Deductible Plans

Examining specific plan scenarios illustrates how HDHPs perform under different usage patterns.

Example 1: Healthy Single Adult Emily, 29, rarely visits doctors beyond annual checkups. Her employer offers an HDHP with a $2,200 deductible, $375 monthly premium, and 80/20 coinsurance after deductible. She contributes $200 monthly to her HSA.

In a typical year, Emily spends: - Premiums: $4,500 - Annual physical: $0 (preventive care covered) - One urgent care visit for bronchitis: $125 - Antibiotics: $35 - Total out-of-pocket: $4,660 - HSA contribution: $2,400 (reduces taxable income by this amount) - Net tax benefit (25% bracket): $600

Her effective cost after tax benefits: roughly $4,060. A comparable PPO would cost $520 monthly ($6,240 annually) with $30 copays—two visits totaling $6,300. Emily saves approximately $2,240 while building HSA assets.

Example 2: Family with Moderate Healthcare Use The Martinez family has two adults and two children. Their employer HDHP carries a $5,000 family deductible, $850 monthly premium, and 70/30 coinsurance. They contribute $500 monthly to their HSA.

Annual expenses include: - Premiums: $10,200 - Four well-child visits: $0 (preventive) - Two adult physicals: $0 (preventive) - Child's broken arm treatment: $3,200 - Various sick visits and prescriptions: $1,200 - Allergy specialist consultation: $450 - Total medical expenses: $4,850 (doesn't quite meet deductible) - Out-of-pocket: $15,050 - HSA contribution: $6,000 - Tax benefit (22% bracket): $1,320

After tax benefits, effective cost is $13,730. A family PPO at $1,150 monthly with $40 copays and $1,500 deductible would run roughly $14,600 including the broken arm. The HDHP saves money but requires managing $4,850 in unpredictable medical expenses.

Example 3: Individual with Chronic Condition Marcus manages Type 2 diabetes requiring quarterly endocrinologist visits, monthly prescriptions, and regular blood work. His HDHP has a $3,000 deductible, $390 monthly premium, and 80/20 coinsurance.

Annual costs include: - Premiums: $4,680 - Four specialist visits at $220 each: $880 - Monthly medication at $180: $2,160 - Quarterly lab work at $95: $380 - Total medical: $3,420 (exceeds deductible) - He pays: $3,000 deductible + 20% of $420 = $3,084 - Total out-of-pocket: $7,764

An HMO at $450 monthly with $50 specialist copays and $20 prescription copays would cost $5,400 in premiums plus $840 in copays ($6,240 total). Marcus would save $1,524 annually by choosing the HMO despite its higher premium.

These examples demonstrate that HDHPs aren't universally better or worse—they perform differently based on actual healthcare consumption patterns.

Author: Lauren Prescott;

Source: blaverry.com

Common Mistakes When Choosing a High Deductible Plan

Many people select HDHPs based on incomplete analysis, leading to financial surprises and regret. Avoiding these pitfalls improves outcomes substantially.

Underestimating medical needs tops the list. Optimism bias leads healthy people to assume they'll remain that way, ignoring the reality that accidents and unexpected illnesses strike unpredictably. Planning solely around last year's minimal healthcare use sets you up for shock when this year brings appendicitis or a skiing injury.

Ignoring the out-of-pocket maximum creates false security. Some focus exclusively on the deductible, forgetting that serious medical events can push costs far higher. A $2,500 deductible sounds manageable, but the $8,000 out-of-pocket maximum represents your true worst-case scenario. Ensure you could handle that full amount if necessary.

Not funding the HSA adequately wastes the plan's primary advantage. Opening an HSA but contributing minimally means you're paying HDHP deductibles without capturing tax benefits. If cash flow prevents meaningful HSA contributions, you're shouldering high deductibles without the offsetting advantages, making traditional plans potentially better choices.

Failing to budget for the deductible causes cash flow crises. Unlike predictable copays, HDHP costs concentrate unpredictably. You might pay nothing for nine months, then face $2,000 in expenses during month ten. Without setting aside monthly reserves, that spike forces difficult choices about delaying care or carrying credit card debt.

Overlooking preventive care coverage leads to unnecessary out-of-pocket spending. Some people avoid their free annual physical because they mistakenly believe it counts against their deductible. Others skip covered cancer screenings or vaccinations. Understanding what qualifies as preventive care under ACA guidelines helps you maximize covered services.

Switching plans impulsively mid-crisis creates problems. If you choose an HDHP, need expensive care in March, then want to switch to a lower-deductible plan, you're generally stuck until the next open enrollment period (unless you have a qualifying life event). Some people select HDHPs without confirming they can commit for a full year regardless of medical surprises.

Neglecting to compare total cost scenarios results in choosing based on premiums alone. Calculate your potential spending under different utilization levels—minimal, moderate, and high—for each available plan. The HDHP might win at minimal and high utilization (due to out-of-pocket maximums) while losing at moderate levels.

Frequently Asked Questions About High Deductible Health Insurance

High deductible health insurance represents a specific financial strategy rather than simply "cheaper insurance." The structure works brilliantly for healthy, financially stable individuals who can absorb upfront costs while building tax-advantaged HSA savings. It performs poorly for people with chronic conditions, limited emergency savings, or high healthcare utilization.

The decision hinges on honest assessment of your health status, financial cushion, and risk tolerance. Premium savings mean nothing if a $3,000 deductible forces you to delay necessary care or carry medical debt. Conversely, paying $200 extra monthly for a traditional plan wastes money if you rarely need care beyond preventive services.

Evaluate HDHPs by calculating total potential costs under multiple scenarios—minimal usage, moderate needs, and serious medical events. Factor in HSA tax benefits if you can contribute meaningfully. Compare these projections against traditional HMO and PPO alternatives using the same scenarios.

The right choice aligns your insurance structure with your actual circumstances rather than abstract notions of "best" plans. For some, that means embracing HDHP cost-shifting and building HSA wealth. For others, it means paying higher premiums for the security of predictable copays and lower deductibles. Neither approach is universally superior—they simply serve different needs and priorities.