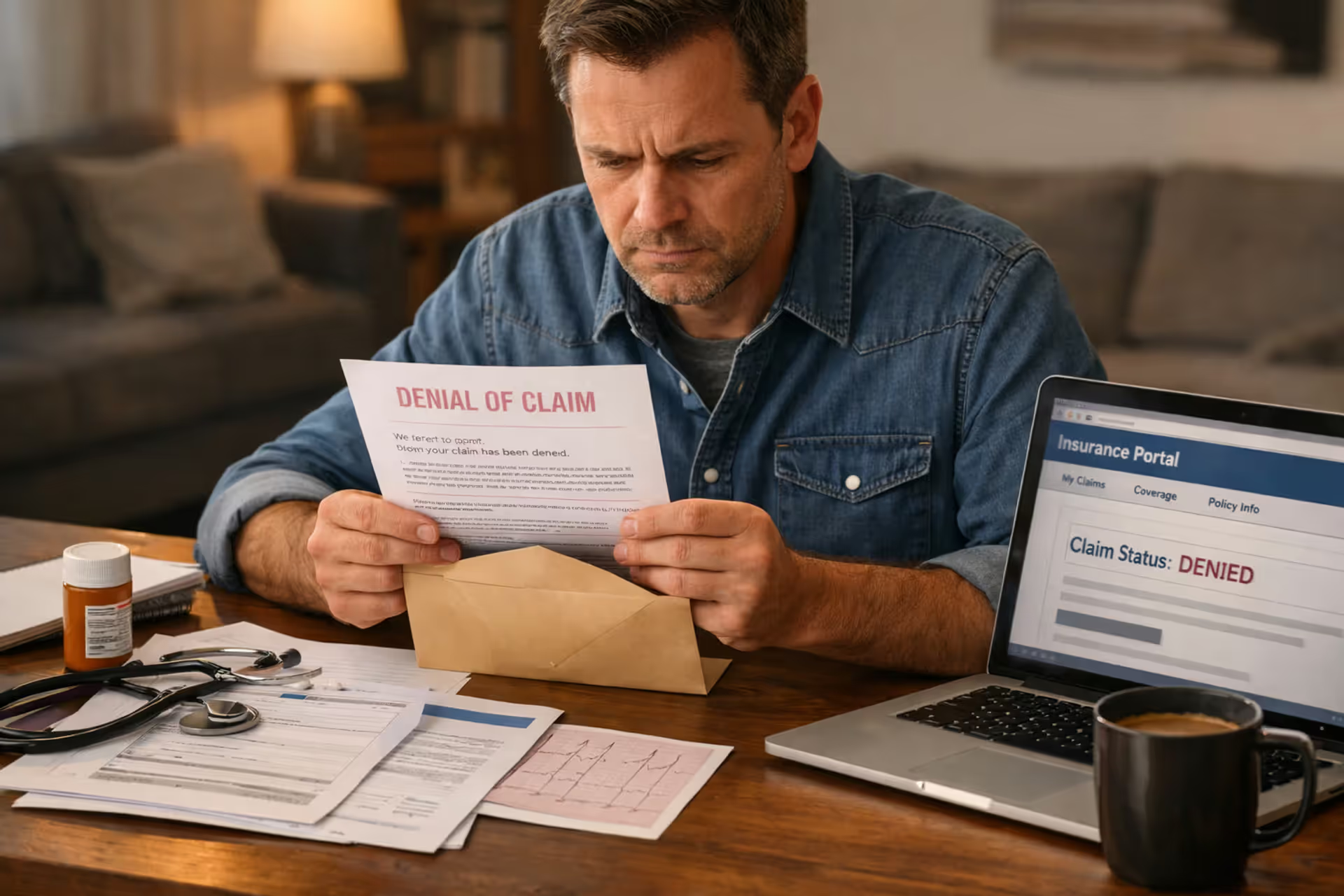

Person sitting at a desk reviewing a health insurance denial letter with medical documents and laptop nearby

Appeal a Health Insurance Denial Successfully

Content

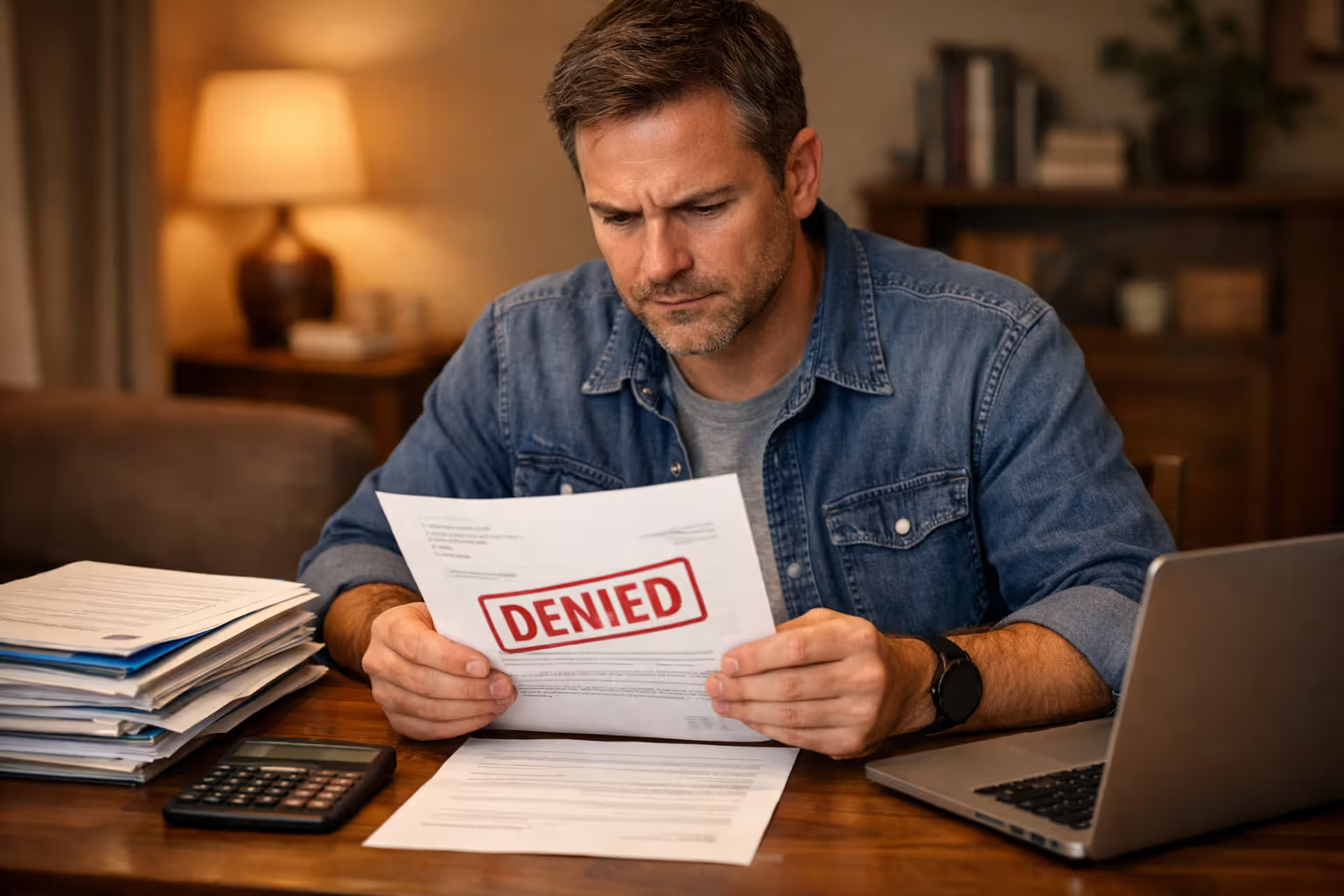

Receiving a denial letter from your health insurance company can feel like a punch to the gut, especially when you're already dealing with medical issues. The good news? Insurers reject roughly 17% of in-network claims, but approximately 60% of appealed denials are overturned when policyholders follow the proper procedures. Your denial isn't necessarily the final word—it's often just the beginning of a process you have every right to pursue.

Most people don't realize that insurance companies expect a certain percentage of denials to go unchallenged. They're counting on policyholders to give up after that first rejection. Understanding how to navigate the appeals process transforms you from a passive recipient of bad news into an active advocate for your own healthcare coverage.

Why Health Insurance Claims Get Denied

Before you can effectively challenge a denial, you need to understand why it happened. Insurance companies reject claims for surprisingly mundane reasons, many of which have nothing to do with whether you actually deserve coverage.

Coding errors top the list of denial causes. Medical billing uses thousands of specific codes to describe procedures, diagnoses, and treatments. A single transposed digit or an outdated code can trigger an automatic rejection. Your provider's office might have submitted code 99214 when they meant 99213, or failed to include a required modifier that explains why a procedure was medically appropriate.

Lack of prior authorization catches many policyholders off guard. Certain procedures, specialist visits, and medications require your insurer's green light before you receive care. Even if your doctor orders an MRI or prescribes a specialty drug, your policy might require advance approval. Miss this step—sometimes because your provider's office dropped the ball—and you'll face a denied claim appeal health insurance situation.

Medical necessity disputes represent a more subjective category. Your insurer might argue that the treatment wasn't essential, that a cheaper alternative exists, or that the service was experimental or investigational. These denials often involve newer treatments, elective procedures with medical components, or situations where clinical guidelines leave room for interpretation.

Out-of-network provider issues create denials even when you thought you were covered. Perhaps the hospital was in-network but the anesthesiologist wasn't, or you received emergency care at the nearest facility without time to verify network status. Some policies severely limit or exclude out-of-network coverage entirely.

Missing or incomplete documentation gives insurers an easy reason to reject claims. Your provider might not have submitted medical records proving the treatment was necessary, failed to include operative notes, or didn't provide a letter explaining why standard treatments wouldn't work for your specific condition.

Policy exclusions and limitations represent legitimate denials where the service genuinely isn't covered under your plan. Cosmetic procedures, experimental treatments, or services that exceed annual or lifetime limits fall into this category. These are harder to overturn but not always impossible, particularly if you can demonstrate the treatment serves a medical rather than purely cosmetic purpose.

Author: Lauren Prescott;

Source: blaverry.com

Understanding Your Right to Appeal an Insurance Decision

Federal law guarantees you the right to challenge coverage decisions, but the process has specific rules and timelines you must follow.

The Affordable Care Act established nationwide protections requiring all non-grandfathered health plans to provide both internal and external appeal options. Internal appeals mean the insurance company reviews its own decision, typically with different personnel than those who made the initial determination. You usually get two levels of internal appeal before moving to the next stage.

External appeals involve an independent third-party reviewer with no financial stake in the outcome. This reviewer examines your case fresh and makes a binding decision the insurer must honor. External review is available for denials based on medical necessity, experimental treatment designations, or rescissions of coverage.

Timeframes matter enormously. For standard pre-service denials (services you haven't received yet), you typically have 180 days to file an internal appeal. The insurer must respond within 30 days for standard appeals or 72 hours for urgent care situations. Post-service denials (for care already received) follow similar timelines, though some states mandate shorter response windows.

State-specific rights often exceed federal minimums. Some states require faster insurer responses, allow appeals for denials that federal law doesn't cover, or provide additional external review opportunities. Your state insurance commissioner's office can clarify which protections apply to your situation.

Keep in mind that different rules govern different plan types. Self-funded employer plans follow federal ERISA regulations, while individual marketplace plans and fully-insured group policies must comply with both federal and state laws. Medicare and Medicaid have entirely separate appeals processes with their own procedures and timelines.

Step-by-Step Health Insurance Appeal Process

Successfully navigating the insurance denial appeal process requires methodical attention to detail and strict adherence to deadlines. Here's exactly how to proceed through each stage.

Gather Your Denial Letter and Medical Records

Your denial letter contains critical information you'll need throughout the health insurance appeal steps. Look for the specific reason for denial, the plan provision or policy section cited, and the deadline for filing your appeal. Many denial letters are intentionally vague—"not medically necessary" without further explanation—which is why you need to dig deeper.

Request your complete medical records related to the denied service. Get office visit notes, test results, imaging reports, and your physician's treatment rationale. If the denial involves a prescription, obtain pharmacy records and any prior medications you tried that didn't work.

Call your insurance company and request the clinical criteria they used to evaluate your claim. Ask which medical policy, coverage guideline, or utilization management protocol led to the denial. Insurers must provide this information, though you may need to be persistent. Get the name and direct phone number of the claims examiner if possible.

Contact Your Insurance Company for Clarification

Before drafting your formal appeal, call the customer service number on your insurance card. Reference your claim number and ask specific questions: Was the denial due to coding? Missing information? A determination that the service wasn't medically necessary? Would different documentation change the decision?

Sometimes denials result from simple administrative errors that a phone call can resolve. The representative might discover that prior authorization was actually on file but not linked to your claim, or that your provider can resubmit with corrected codes. Document every conversation—date, time, representative's name, and what they told you.

If the denial stands, ask about the specific appeal procedures for your plan. Confirm the mailing address for appeals, whether you can submit electronically, and the exact deadline. Request any appeal forms you need to complete.

Author: Lauren Prescott;

Source: blaverry.com

Submit Your Internal Appeal

Your internal appeal should be comprehensive, organized, and persuasive. Write a cover letter clearly stating you're appealing the denial, referencing your claim number, and briefly explaining why the decision was wrong.

Include supporting documentation: your doctor's letter of medical necessity, relevant medical records, clinical studies supporting the treatment, and citations to your policy language showing the service should be covered. If coding errors caused the denial, include the corrected codes with an explanation.

Your physician's letter carries enormous weight. It should explain your diagnosis, why the denied treatment was medically appropriate for your specific condition, why alternative treatments were inadequate or contraindicated, and how the treatment aligns with accepted medical standards. Generic letters rarely succeed—specificity matters.

Send your appeal via certified mail with return receipt, or use the insurer's online portal if available (and save confirmation). Keep complete copies of everything you submit. Missing the deadline by even one day can forfeit your appeal rights, so build in buffer time.

Request an External Review if Denied Again

If your internal appeal fails, you can request an external review by an independent reviewer. Your insurer must provide information about how to request external review when they deny your internal appeal.

External reviewers are typically physicians or other healthcare professionals with expertise in the relevant medical area. They evaluate whether the denial was appropriate based on medical evidence and your policy terms. Their decision is binding—if they overturn the denial, your insurer must cover the service.

You don't necessarily need to exhaust all internal appeal levels before seeking external review for urgent situations. If waiting for internal appeals would jeopardize your life or health, or seriously impair your ability to regain maximum function, you can pursue simultaneous or expedited external review.

What to Include in Your Denied Claim Appeal

A strong insurance claim appeal guide emphasizes documentation quality over quantity. Here's what makes appeals succeed:

A clear, concise appeal letter that states the facts without emotion. Explain what was denied, why you believe the denial was incorrect, and what you want the insurer to do. Reference specific policy language that supports coverage.

Your physician's letter of medical necessity remains the cornerstone of most successful appeals. This should detail your medical history, current condition, treatments already tried, why the denied service is appropriate, and the expected outcome. Letters that cite clinical practice guidelines, peer-reviewed research, or FDA approval strengthen your case considerably.

Medical records and test results that demonstrate the severity of your condition and the appropriateness of the treatment. If you tried conservative treatments first, include documentation showing they failed or were contraindicated.

Clinical evidence and published research supporting the denied treatment's effectiveness for your condition. Medical journal articles, clinical trial results, and professional society treatment guidelines help counter "experimental" or "not medically necessary" denials.

Policy language analysis showing that the service should be covered under your plan. If the denial cites a specific exclusion, explain why that exclusion doesn't apply to your situation. If the policy language is ambiguous, courts and external reviewers typically interpret it in the policyholder's favor.

Completed appeal forms if your insurer requires specific paperwork. Leaving sections blank or failing to sign forms gives the company an easy reason to reject your appeal on procedural grounds.

Documentation of prior authorization if you obtained it but the claim was still denied. Administrative mix-ups are common, and proof that you followed the rules strengthens your position.

Author: Lauren Prescott;

Source: blaverry.com

Common Mistakes That Weaken Your Insurance Claim Appeal

Even strong cases fail when policyholders make avoidable errors during the appeals process.

Missing deadlines is the most devastating mistake because it's usually irreversible. Mark your calendar with the appeal deadline and work backward, giving yourself at least two weeks to gather documentation and prepare your appeal. If you're approaching the deadline without all your materials, submit what you have and indicate that additional documentation will follow.

Submitting incomplete documentation forces the reviewer to make decisions without full information, rarely in your favor. A physician's letter that says "this treatment is medically necessary" without explaining why carries little weight. Medical records without a clear narrative leave reviewers guessing about relevance.

Failing to address the specific denial reason is surprisingly common. If the insurer denied your claim for lack of prior authorization, your appeal needs to either prove you obtained authorization or demonstrate that the prior authorization requirement shouldn't apply. Arguing about medical necessity won't help if that wasn't why the claim was denied.

Not following your plan's appeal procedures can invalidate your appeal. If your insurer requires a specific form, use it. If they specify a mailing address for appeals, don't send it to the general claims address. Procedural mistakes give insurers easy grounds to dismiss appeals without reviewing the merits.

Giving up after the first denial means losing before the real fight begins. Internal appeals have lower success rates than external reviews because the same company is reviewing its own decision. External review is where many policyholders finally win.

Failing to keep copies and documentation of everything you submit leaves you unable to prove what you sent or when. If the insurer claims they never received your appeal or that you missed the deadline, your certified mail receipt and copies become crucial evidence.

Going it alone when you need help costs people successful appeals. Complex cases involving experimental treatments, high-dollar claims, or ambiguous policy language often benefit from professional assistance.

When to Get Help with Your Health Insurance Appeal

You don't have to navigate this process alone, and some situations practically demand professional assistance.

Patient advocates specialize in helping people appeal insurance denials. Some work independently, while others are employed by hospitals or nonprofit organizations. Many offer free or sliding-scale services. They understand insurance company tactics, know what documentation strengthens appeals, and can communicate effectively with insurers and providers.

Your state insurance commissioner's office provides free assistance to residents dealing with insurance disputes. They can explain your rights, help you understand your policy, and sometimes intervene directly with insurers. Many states operate consumer assistance programs specifically for health insurance issues.

Legal assistance becomes important for high-value denials, disability coverage disputes, or situations where the insurer appears to be acting in bad faith. Some attorneys work on contingency (taking a percentage of what they recover), while others charge hourly fees. Legal aid organizations sometimes handle insurance appeals for low-income individuals.

Nonprofit organizations focused on specific conditions often provide free appeal assistance to patients dealing with related denials. Cancer support organizations, rare disease foundations, and condition-specific patient groups frequently help members challenge coverage denials.

Professional appeal companies will handle your entire appeal for a fee, typically a percentage of the claim value if they win. They can be worth the cost for complex, high-dollar claims, though many situations don't require paid help.

Consider getting help when your appeal involves experimental treatment designations, when the denied service costs more than $10,000, when you've already lost an internal appeal, or when you're too ill to manage the process yourself. Free resources should be your first stop—many people pay for services they could have received at no cost.

Table: Internal vs. External Appeal Comparison

| Feature | Internal Appeal | External Appeal |

| Who reviews | Insurance company staff or contracted reviewers | Independent third-party reviewer with relevant medical expertise |

| Timeframe | 30 days for standard; 72 hours for urgent pre-service; 60 days for urgent post-service | 60 days for standard; 72 hours for urgent cases |

| Cost to you | Free | Free (insurer pays for external review) |

| Binding decision | No—you can appeal further if denied | Yes—insurer must comply with decision |

| When to use | First step for all denials; required before external review in most cases | After internal appeal denial, or simultaneously for urgent situations |

Expert Perspective

Most people don't realize that insurers routinely deny claims they know are legitimate, banking on the fact that the majority of patients won't appeal. When patients do appeal with proper documentation, success rates jump dramatically. The system isn't designed to be user-friendly, but it does work for those persistent enough to navigate it.

— Karen Pollitz

This observation highlights a critical reality: the appeals process exists precisely because initial denials aren't always correct or justified. Your persistence and thorough documentation often matter more than the initial strength of the insurer's position.

FAQ: Health Insurance Denial Appeals

Receiving a health insurance denial doesn't mean your fight is over—it means it's just beginning. The appeals process exists because insurers make mistakes, apply policies incorrectly, and sometimes deny claims they shouldn't. Your willingness to challenge a denial, backed by thorough documentation and persistence, often determines whether you'll receive the coverage you're entitled to under your policy.

Start immediately when you receive a denial. Time limits are strict, and gathering strong supporting documentation takes longer than most people expect. Focus on addressing the specific reason for denial with clear, factual evidence rather than emotional appeals. Your physician's detailed support matters more than any other single factor for medical necessity denials.

Don't let the process intimidate you into giving up. Insurance companies use complexity as a barrier, but the basic steps—gather your denial information, collect supporting documentation, submit a clear appeal with evidence, and escalate to external review if necessary—are manageable for most people. Free resources exist to help you at every stage, from state insurance departments to nonprofit patient advocacy organizations.

Remember that every successful appeal not only gets you the coverage you deserve but also makes insurers think twice about denying similar claims in the future. Your persistence creates accountability in a system that too often counts on patient exhaustion and confusion.