Person reviewing health insurance card and medical bills at a desk with a laptop showing an insurance portal

How to Check Health Insurance Coverage Before Your Appointment

Content

Nobody wants a $4,000 surprise bill three weeks after a routine procedure. Yet that's exactly what happens when patients skip the verification step and make assumptions about their coverage. I've seen friends scramble to negotiate payment plans because they figured their insurance "probably covered" a specialist visit that turned out to be completely out-of-network.

Let's fix that. You'll learn exactly how to confirm what your plan actually pays for, verify you're still covered, and spot potential problems before they hit your bank account.

Why Verifying Your Coverage Matters

Here's the uncomfortable truth: medical debt contributes to more than 60% of personal bankruptcies in America. The worst part? A huge chunk of these cases involve people who had insurance but didn't understand what it actually covered.

Think you can just ask at the front desk and call it done? Not quite. Your receptionist might confirm you have insurance, but they won't know about that obscure exclusion buried on page 47 of your policy documents. They can't tell you whether your deductible reset last month or if your specific procedure needs approval first.

The money adds up faster than you'd expect. Let's say you schedule an outpatient surgery. You're thinking, "I've got a $50 copay for procedures." But that $50 might only apply to in-network facilities. Your surgeon could be in-network while the surgical center isn't. Suddenly you're looking at a bill for $8,000 because nobody checked the facility's status.

Your coverage probably changed since last year—maybe even since last month. Did your employer switch insurance providers during open enrollment? That doctor who treated you in March might not accept your new plan. Or your insurance company quietly dropped an entire hospital system from their network. It happens more often than you'd think.

Here's something else: many procedures require approval before you receive treatment. Miss that step, and your insurance company can deny the entire claim. You'll be stuck paying the full amount even though the service would've been covered with proper authorization.

Beyond the financial nightmare, verification gives you actual choices. When you know upfront that a procedure will cost $3,000 out-of-pocket instead of $300, you can look for alternatives. Maybe a different provider offers the same service at a better rate. Perhaps your doctor can suggest a covered alternative treatment. Without checking first, you've already lost those options.

Author: Derek Whitmore;

Source: blaverry.com

Where to Find Your Insurance Policy Information

That insurance card in your wallet does more than prove you're insured. Flip it over. You'll find several phone numbers—one for general questions, another for pharmacy issues, maybe a separate line for mental health services or urgent authorization requests. Screenshot both sides of your card right now. Seriously, do it. You'll thank yourself when you need that member ID number at 10 PM on a Sunday.

Every insurance company runs a member portal on their website. Once you create an account (you'll need your member ID and some personal details), you can access your complete coverage information anytime. These portals show real-time updates on your deductible progress, list every claim from the past year, and let you search for providers who accept your plan.

Mobile apps replicate everything from the website but make it easier to check details while you're already at the doctor's office. Most apps let you save your digital insurance card, look up nearby urgent care facilities, and check whether your pharmacy has your prescriptions in stock. Some even let you scan a prescription bottle to instantly see what you'll pay.

Somewhere in your filing cabinet (or more likely, your email inbox) sits your actual policy document. It might be called "Evidence of Coverage" or "Certificate of Benefits." Yes, it's boring. Yes, it's 80+ pages of legal terminology. But this document contains the definitive answer to every coverage question. When the customer service rep can't explain something clearly, this document settles the debate.

Get insurance through your job? Your HR department knows things. They can explain why certain treatments aren't covered, help you understand recent plan changes, and sometimes intervene directly with the insurance company on complicated cases. They might also maintain a benefits portal with plan comparison tools and educational resources.

That Summary of Benefits and Coverage arrives in your inbox every year around open enrollment. Don't delete it. This standardized, federally-required document explains your plan in plain English (or at least, plainer English than the full policy). Keep the PDF somewhere you can find it easily.

How to Check What Your Plan Covers

Reading Your Summary of Benefits and Coverage

Federal law requires every health plan to provide an SBC using the same format. This makes comparing plans easier, but more importantly, it means you can find information quickly once you know where to look.

The document splits coverage into everyday categories: primary care visits, specialist appointments, emergency room trips, hospital stays, prescription medications, and preventive care. For each category, you'll see exactly what comes out of your pocket—whether that's a flat copay, a percentage after your deductible, or no cost at all.

Scroll toward the end for the coverage scenarios. These walk through sample situations like childbirth or managing Type 2 diabetes, breaking down every charge you'd face. Your actual costs will vary (different complications, different providers, different circumstances), but these examples give you a realistic baseline. If the childbirth scenario shows $2,800 in out-of-pocket costs and you're pregnant, start planning for that amount.

The exclusions list tells you what's absolutely not covered. Cosmetic surgery usually appears here. So do experimental treatments, certain fertility procedures, and specific types of therapy. Read this section before assuming anything is covered—it'll save you arguments with customer service later.

A glossary appears at the end explaining insurance jargon. Reference it whenever you encounter a term you don't recognize elsewhere in your documents.

Understanding Common Insurance Terms

Your deductible is the amount you spend before insurance starts helping with costs. Say your deductible is $1,500. You'll pay the full negotiated rate for services until your spending hits that threshold within the calendar year. However, certain services bypass this requirement—preventive care like annual checkups and some primary care visits might cost you just a copay regardless of whether you've met your deductible.

When you see a copay amount, that's the flat fee you hand over for that type of visit. Your specialist charges $350 for an appointment, but your plan has a $40 specialist copay? You pay $40, insurance handles the rest. These payments typically don't chip away at your deductible, though they do count toward your annual out-of-pocket maximum.

After your deductible is satisfied, coinsurance becomes relevant. This means you split the bill with your insurance company according to a set percentage. With 30% coinsurance on a $2,000 procedure, you'd owe $600 while your insurer covers the remaining $1,400. You'll pay this percentage until you hit your out-of-pocket maximum for the year.

The out-of-pocket maximum protects you from catastrophic costs. After your combined spending on deductibles, copays, and coinsurance reaches this cap, your insurance covers everything else for the rest of that year at 100%. This ceiling includes only covered, in-network services—your premiums don't count, and neither do out-of-network charges on most plans.

In-network versus out-of-network status makes an enormous difference in your costs. In-network providers have agreed to accept discounted rates from your insurer. An MRI might be billed at $3,000, but the negotiated in-network rate could be $800. Out-of-network? You might pay that full $3,000, and it won't even count toward your deductible. Some plans offer zero coverage for out-of-network care unless you're facing an emergency.

Author: Derek Whitmore;

Source: blaverry.com

Checking Coverage for Specific Services or Procedures

When you need to verify a particular treatment, get the specific medical codes from your doctor's office. CPT codes identify procedures, while ICD-10 codes describe diagnoses. A code provides much more precision than saying "I need physical therapy."

Call your insurance company with these codes ready. Don't ask vague questions like "Do you cover MRIs?" Instead: "I need CPT code 72148, a lumbar spine MRI. Is this covered? What's my cost-sharing? Do I need prior authorization?" Write down the representative's name and get a reference number for your call. If they give you the wrong information, that reference number creates a record you can reference.

For prescriptions, look up your plan's formulary—the official list of covered medications organized by cost tiers. Tier 1 drugs (usually generics) cost you the least. Tier 4 or 5 specialty medications might require significant coinsurance. If your doctor prescribes something not on the formulary, you'll likely pay full retail price unless you request a formulary exception and your doctor justifies why you need that specific medication.

Preventive services get special treatment under the Affordable Care Act. Plans must cover specific screenings, vaccines, and wellness visits at zero cost when you use in-network providers. But here's the catch: if your doctor addresses any non-preventive issues during that "free" annual physical, the visit might generate additional charges. Ask upfront whether your appointment will stay purely preventive.

Methods to Verify Insurance Eligibility and Active Status

Active coverage confirmation means checking that your policy is currently in force. You might assume everything's fine, but premium payment hiccups, employment changes, or administrative mistakes can create coverage gaps you won't know about until you try to use your insurance.

Pick up the phone and call the number on your insurance card. Ask the representative to confirm your coverage is active today and will remain active on your appointment date. They can spot account issues, pending termination notices, or payment problems. Don't call the morning of your appointment—give yourself a few days in case something needs fixing.

Your insurer's website offers instant eligibility checking. Look for sections labeled "My Coverage," "Eligibility Verification," or "Member Status." These tools display your coverage effective dates, current status, and any upcoming changes. The information updates daily, so you're seeing near-real-time data.

When you schedule an appointment, healthcare providers run your insurance through eligibility systems that ping insurance databases. This confirms coverage at that moment, but things can change between scheduling and your actual visit. If your appointment is weeks away and something affects your coverage, that initial verification becomes outdated.

Recent Explanation of Benefits statements prove your insurance was active when those claims processed. An EOB from last week suggests your coverage continues, though it doesn't guarantee you're still covered today. Think of EOBs as historical evidence rather than current confirmation.

Watch for payment confirmations after your premium gets processed. Many insurers email or text you when they receive payment, giving you informal verification that your coverage continues uninterrupted.

| Method | Time Required | Information Needed | Best Used For |

| Online Portal Check | 2-5 minutes | Login username and password, member ID number | Quick coverage confirmations, reviewing what you've spent toward your deductible, examining past claims |

| Direct Phone Call | 10-20 minutes | Member ID, birthdate, the specific CPT codes for your procedure | Complex coverage questions, prior authorization requirements, detailed cost breakdowns |

| Provider Office Verification | Handled automatically by staff | Current insurance card, photo ID | Standard verification before routine scheduled appointments |

| Mobile App Lookup | 1-3 minutes | App credentials, fingerprint or face ID | Finding nearby in-network providers while traveling, accessing your digital insurance card, checking prescription coverage on the go |

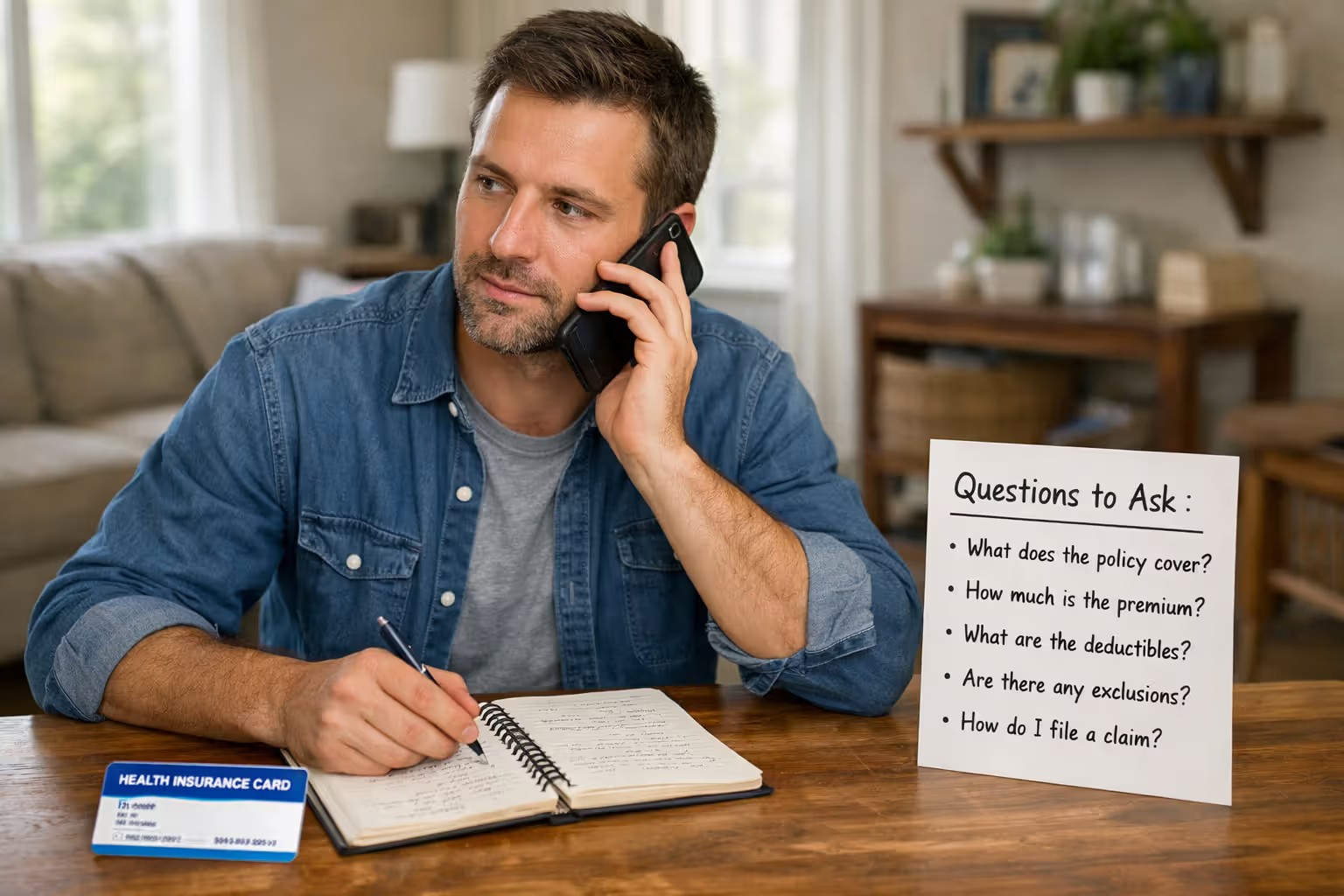

Questions to Ask Your Insurance Company

Generic questions get generic answers. When you call to verify health insurance, prepare specific questions about your exact situation.

Start here: "I've spent $X toward my deductible this year—how much remains before I hit my deductible?" This determines whether you're still in the paying-full-price phase or whether insurance starts sharing costs.

Get specific about copays: "What do I pay for a specialist consultation?" or "What's my copay if I need outpatient surgery?" These amounts vary significantly by service type. Your primary care copay might be $25 while a specialist runs $60.

Nail down provider network status: "Is Dr. Johnson at City Medical Center in my network?" Specify the exact location because some doctors are in-network at one office but out-of-network at their other location across town.

Ask directly about authorization: "Does this procedure need prior authorization? How do I get it? How long will approval take?" Some authorizations take 24 hours, others need two weeks. Missing this step often leads to denied claims.

Find out about limits: "How many physical therapy sessions does my plan cover per year?" or "What's my annual maximum for durable medical equipment?" Certain benefits cap out after a specific number of visits or dollar amount.

Request a cost breakdown: "What will this cost me out-of-pocket?" Make sure they're factoring in your current deductible status. Ask them to itemize facility fees, physician charges, and potential additional costs you might not expect.

Check whether related services are covered: "My surgery requires anesthesia—is my anesthesiologist in-network? What about pathology if they send tissue for testing?" Different specialists involved in one procedure might have different network statuses, creating surprise bills.

Author: Derek Whitmore;

Source: blaverry.com

How to Confirm Coverage Through Your Healthcare Provider

Your doctor's front desk staff verify insurance as part of their standard process, but that doesn't mean you should skip your own verification. They're checking you have insurance, not examining whether that insurance covers this specific service.

When scheduling appointments, give them your current insurance details and specifically ask them to verify coverage. Many offices check immediately during the scheduling call. Problems discovered now give you time to resolve them instead of finding out when you arrive for your appointment.

Prior authorization involves your doctor requesting permission from your insurer before delivering specific services. Your provider usually handles the submission, but you need to confirm they've actually done it. Ask your doctor's office: "Has the prior authorization been submitted? What's the status? When should we expect a decision?"

The billing department at your doctor's office can estimate your costs based on your specific insurance. They know the contracted rates between your insurer and their practice, so their estimates often beat the generic estimates you get from calling your insurance company. Just remember these are estimates, not guarantees.

Bring critical documents to every appointment: insurance card (or a phone screenshot), government-issued photo ID, and any prior authorization reference numbers. If you called your insurance company recently about this visit, bring those reference numbers too.

Understand what your provider's office can and cannot verify. They confirm you have active insurance and check basic eligibility. They typically don't know about your specific plan's exclusions, authorization requirements, or coverage limitations. You're responsible for understanding your own policy details.

Some practices collect estimated payments when you check in. If the actual insurance payment differs from their estimate, they'll refund overpayments or bill you for any remaining balance. Save your receipts and compare them against your EOB when it arrives to ensure everything matches.

Author: Derek Whitmore;

Source: blaverry.com

Common Coverage Verification Mistakes to Avoid

Banking on past experience creates expensive problems. Last year's coverage doesn't predict this year's benefits. Networks change, formularies get updated, and plan terms shift every January. Verify your current coverage instead of assuming things stayed the same.

Checking only your main provider's network status sets you up for surprise bills. During surgery, you might see an in-network surgeon but get separate bills from an out-of-network anesthesiologist, pathologist, or surgical assistant. Ask about every professional who'll be involved and verify each one individually.

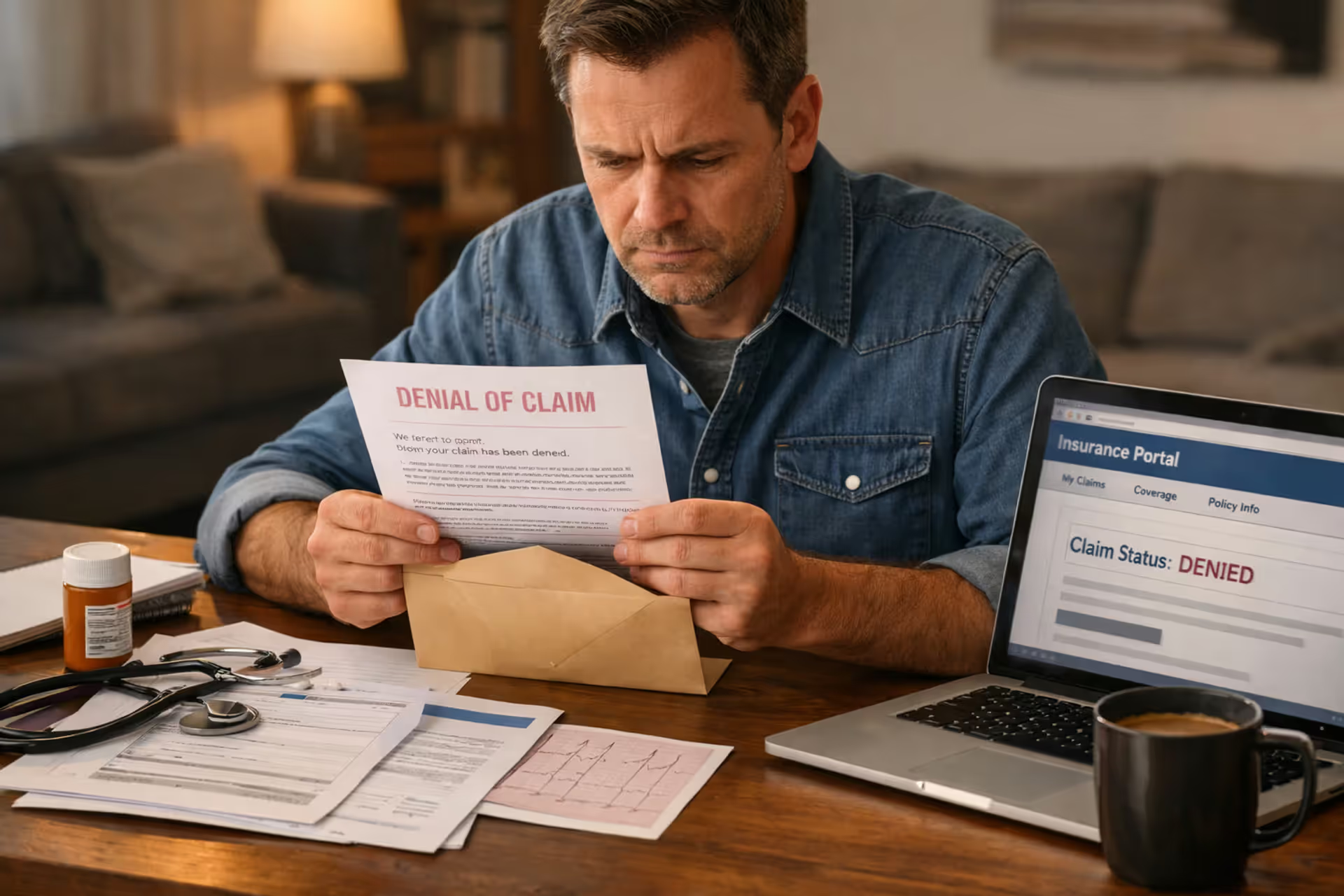

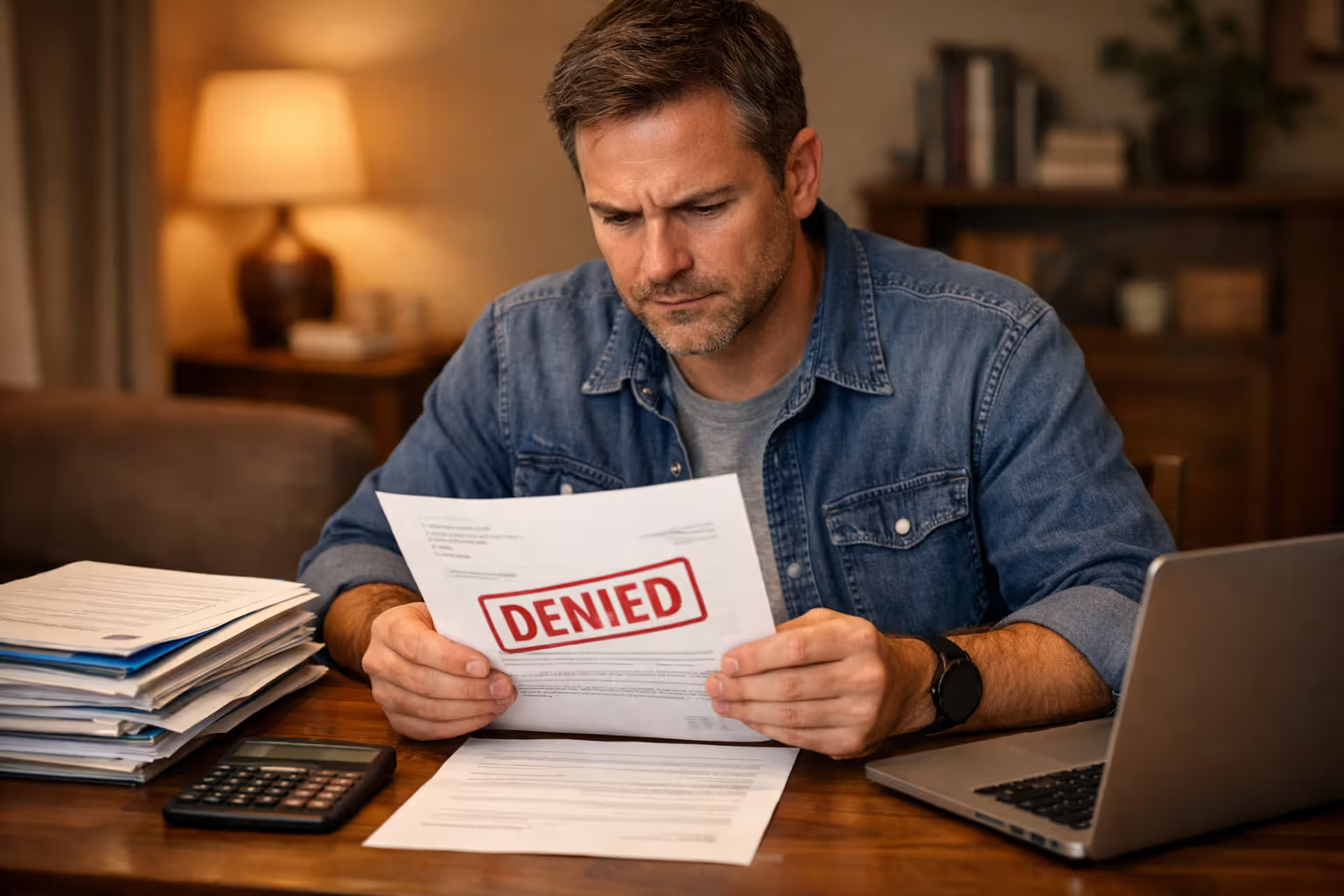

Skipping prior authorization because you forgot or didn't know results in claim denials. Your service might be covered in general, but without required pre-approval, insurers can refuse to pay. These denials typically make you responsible for the entire bill.

Confusing policy dates causes coverage gaps. Switching jobs? Your old insurance ends at midnight on your last day. Your new coverage might not start for two weeks. Schedule appointments carefully around these transitions, and verify which policy is active on your appointment date.

Trusting phone conversations without documentation leads to he-said-she-said disputes. After every call with your insurer, write down the representative's name, date, time, reference number, and exactly what they told you. Request written confirmation through your online portal or email when possible.

Mixing up medical necessity with coverage causes confusion. Your plan might cover a service in general, but the insurer can still deny your claim if they determine it wasn't medically necessary in your specific case. Work with your doctor to ensure medical necessity is clearly documented, especially for services that often get questioned.

Ignoring the appeals process means leaving money on the table. Insurers deny claims incorrectly all the time. If you receive a denial that seems wrong, file an appeal. Many denials get overturned, but you must respond within the deadline specified in your denial letter (usually 180 days for standard appeals).

The single biggest mistake I see patients make is waiting until after they receive care to think about insurance coverage. By then, it's too late to make different choices or prepare financially. Taking 20 minutes to verify coverage before an appointment can save thousands of dollars and countless hours of frustration dealing with surprise bills

— Jennifer Martinez

Frequently Asked Questions

Checking your health insurance coverage before medical appointments shifts the power back to you. Yeah, it takes some time upfront—maybe 20 minutes for a routine check, longer for complex procedures. But compare that to the hours you'll spend fighting incorrect bills or negotiating payment plans for services you assumed were covered.

Start by getting comfortable with your policy documents and online portal. Bookmark the login page. Download the mobile app. Save your member ID somewhere easy to find. When you need information quickly, you'll know exactly where to look.

Make verification a standard step whenever you schedule medical appointments. Add it to your pre-appointment checklist alongside gathering relevant medical records and writing down questions for your doctor. Those few minutes confirming benefits can prevent hours of frustration and potentially thousands in unexpected expenses.

Remember that healthcare providers and insurance companies both help with verification, but the final responsibility lands on you. Providers check eligibility and submit prior authorizations, but they don't know every detail of your specific policy. Insurance representatives explain your benefits, but they don't know exactly what services your doctor plans to deliver. You're the bridge between these parties, and staying informed protects your wallet.

Keep detailed records of all insurance communications. Save those reference numbers from phone calls. Download copies of prior authorization approvals. File away cost estimates from either your insurer or provider. These documents become crucial evidence if billing disputes pop up months later.

Medical costs keep climbing, making smart insurance navigation more critical every year. When you understand how to verify your coverage, interpret your benefits, and ask the right questions, you stop being a passive patient and become a strategic consumer who makes informed choices about healthcare spending. That knowledge translates directly into money saved and stress avoided.