Top-down view of a desk with medical bills, insurance card, laptop showing insurance portal, calculator, pen, and a coffee cup

How to Submit Medical Bills to Insurance for Reimbursement

Content

Navigating the insurance reimbursement process can feel overwhelming, especially when you're already dealing with medical expenses. While many healthcare providers bill insurance companies directly, there are situations where you'll need to submit medical bills yourself. Understanding this process ensures you get the reimbursement you're entitled to without unnecessary delays or denials.

When You Need to Submit Medical Bills Yourself

Most in-network providers handle insurance billing on your behalf. However, several scenarios require you to take the reins and submit claims directly to your insurance carrier.

Out-of-network provider visits

When you see a doctor or specialist outside your insurance network, they typically don't have a billing arrangement with your carrier. You'll pay the full amount upfront, then submit a medical bill insurance claim yourself. The provider should give you a detailed receipt or superbill—a document containing diagnosis codes, procedure codes, and itemized charges that your insurer needs to process the claim.

Some out-of-network providers offer courtesy billing, but don't count on it. Assume you'll handle the paperwork unless explicitly told otherwise.

Emergency care situations

Emergency rooms often stabilize patients first and sort out insurance later. If you receive emergency care at an out-of-network facility, you might need to submit the claim yourself, particularly if the hospital doesn't participate in your plan's network. Federal regulations provide some protection against balance billing in emergencies, but you still need to file correctly to access those protections.

Keep every document from emergency visits: admission paperwork, treatment records, discharge summaries, and itemized bills. Emergency claims often face extra scrutiny, so thorough documentation matters.

Author: Lauren Prescott;

Source: blaverry.com

Upfront payment scenarios

Some situations require immediate payment regardless of network status. Dental procedures, certain mental health services, and alternative medicine treatments often operate on a pay-first basis. International medical care almost always requires upfront payment, with reimbursement handled later through your insurance company's international claims department.

Cash-pay discounts complicate matters. If you receive a reduced rate for paying upfront, your insurance reimbursement will typically be based on the amount you actually paid, not the provider's standard rates.

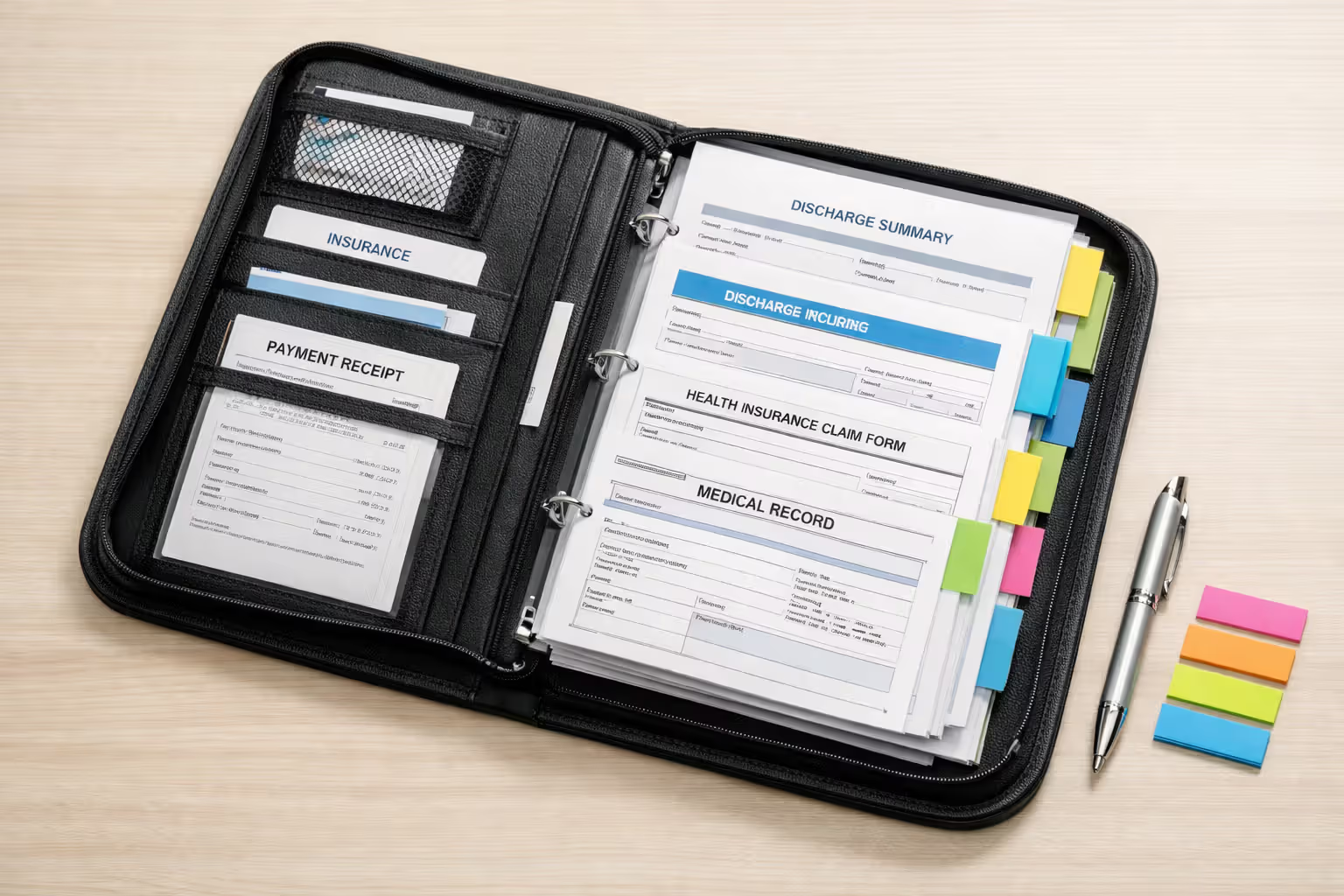

Documents Required for Your Medical Bill Claim

Submitting incomplete documentation is the fastest way to delay your reimbursement. Insurance companies can't process what they can't verify.

Itemized bills vs. summary statements

A summary statement showing "office visit - $250" won't cut it. You need an itemized bill listing every service with its corresponding CPT (Current Procedural Terminology) code and diagnosis code. These codes tell your insurer exactly what was done and why.

Request itemized bills from your provider's billing department within a few days of service. Waiting months makes it harder to obtain detailed records, and some providers charge fees for recreating old documentation.

The itemized bill should include: provider's name and tax ID number, your name and date of birth, date of service, detailed description of each service, procedure codes, diagnosis codes, and the amount charged for each line item.

Receipts and proof of payment

Your insurance company needs proof you actually paid the bill. A credit card receipt, canceled check image, or payment confirmation from the provider's billing system all work. If you paid cash, get a receipt with the provider's letterhead and signature.

Electronic payment confirmations should show the provider's name, payment amount, date, and your name. Screenshots from banking apps are generally acceptable if they clearly display these details.

Supporting medical records

Complex claims benefit from supporting documentation. If you're submitting a claim for specialized testing, include the ordering physician's referral and any consultation notes explaining medical necessity. For durable medical equipment like wheelchairs or CPAP machines, include the prescription and letter of medical necessity.

Prior authorization documentation should always accompany your claim if the service required pre-approval. Even if you obtained authorization by phone, reference the authorization number on your claim form.

Step-by-Step Medical Bill Claim Process

The medical bill claim process varies slightly by carrier, but follows a general pattern. Mastering these steps prevents most common errors.

Completing the claim form correctly

Every insurance company provides a claim form—usually called a "Medical Claim Form" or "Health Insurance Claim Form." Download the current version from your insurer's website rather than using an old form; requirements change.

Fill out every required field. Partial information triggers automatic rejections. Use your full legal name exactly as it appears on your insurance card. Policy numbers, group numbers, and member ID numbers must match precisely.

In the patient information section, provide your date of birth, address, and contact information. The provider information section requires the doctor's or facility's full name, address, tax ID number, and National Provider Identifier (NPI) number—all found on your itemized bill.

Sign and date the form. Unsigned forms get rejected immediately. If filing for a dependent, you'll sign as the policyholder.

The "Assignment of Benefits" section determines who receives payment. If you've already paid the provider, leave this blank so the check comes to you. If the provider is awaiting payment, you can assign benefits directly to them.

Where to submit your claim (online, mail, fax)

Most major insurers now prefer electronic submission through member portals. Log into your account, navigate to the claims section, and upload your documents as PDFs or clear photo images. Online submission provides instant confirmation and faster processing.

Mailing claims remains an option. Your insurance card lists the claims mailing address, but verify it online—addresses change. Send via certified mail with return receipt if you're near the filing deadline. Keep copies of everything you mail.

Fax submission works for some carriers but is becoming obsolete. If you fax, call to confirm receipt within two business days.

Never submit the same claim through multiple channels simultaneously. This creates duplicate claim issues that take weeks to untangle.

Author: Lauren Prescott;

Source: blaverry.com

Tracking your submission

After submitting, record the date, method, and any confirmation numbers. Most insurers assign a claim number within 48 hours of electronic submission or 7-10 days for mailed claims.

Check your online account weekly for status updates. Claims typically move through stages: received, under review, processed, and payment issued. If a claim sits in "under review" for more than two weeks, call the claims department.

When calling, have your member ID, claim number, date of service, and provider name ready. Ask specific questions: "What additional information do you need?" or "When will this claim be adjudicated?" Generic inquiries get generic responses.

How Insurance Reimbursement Works After Submission

Understanding the behind-the-scenes process helps you anticipate delays and recognize when something's wrong.

Claim review and processing

Once received, your claim enters a queue. A claims examiner verifies that the service is covered under your plan, checks whether you've met your deductible, confirms the provider's credentials, and ensures the diagnosis codes support the procedures billed.

For straightforward claims—a simple office visit or standard lab work—this review takes 5-10 business days. Complex claims involving multiple providers, surgical procedures, or expensive treatments undergo additional review by clinical staff or medical directors, extending the timeline to 30-45 days.

During review, the examiner applies your plan's cost-sharing rules: deductible, copayment, and coinsurance. They also check for duplicate claims (did you already submit this?) and coordination of benefits (do you have other insurance that should pay first?).

Explanation of Benefits (EOB) breakdown

Before you receive reimbursement, you'll get an Explanation of Benefits. This document isn't a bill—it's a detailed breakdown of how your claim was processed.

The EOB shows: the provider's billed amount, the allowed amount (what your plan considers reasonable), the discount or adjustment (the difference between billed and allowed), your deductible applied, your copay or coinsurance, and the amount the insurer will pay.

Read your EOB carefully. The "patient responsibility" section shows what you owe, while the "plan paid" section shows your reimbursement if you paid upfront. Discrepancies between what you expected and what the EOB shows warrant a call to member services.

EOBs arrive 1-2 weeks before reimbursement checks, giving you time to spot and dispute errors.

Author: Lauren Prescott;

Source: blaverry.com

Payment methods and timelines

Reimbursement arrives via check mailed to your address on file or direct deposit if you've enrolled in electronic payments. Direct deposit cuts 5-7 days off the timeline.

The check amount matches the EOB's "plan paid" figure. If you paid $500 but your EOB shows the plan only covers $350 after applying your deductible and coinsurance, you'll receive $350.

Processing times vary by claim complexity and submission method. Electronic claims submitted correctly typically result in payment within 15-20 business days. Mailed claims take 25-35 business days. Claims requiring additional documentation or medical review can extend to 45-60 days.

Insurance Claim Reimbursement Timeline by Carrier

Different insurers process claims at different speeds. This table reflects typical timelines for major carriers in 2026:

| Insurance Carrier | Standard Claims | Complex Claims | Electronic vs. Mail Difference |

| UnitedHealthcare | 14-18 days | 30-40 days | 5-7 days faster electronically |

| Anthem Blue Cross Blue Shield | 12-16 days | 28-35 days | 4-6 days faster electronically |

| Aetna | 15-20 days | 35-45 days | 6-8 days faster electronically |

| Cigna | 10-14 days | 25-35 days | 3-5 days faster electronically |

| Humana | 16-22 days | 32-42 days | 5-7 days faster electronically |

These timelines assume complete, accurate submissions. Missing information or errors can double these timeframes.

Common Mistakes That Delay Medical Bill Claims

Even minor errors trigger rejections. Avoiding these mistakes keeps your claim moving.

Missing information on forms tops the delay list. Blank fields, illegible handwriting, or missing signatures force the claim back to you for correction. Use black ink if handwriting forms, or better yet, type information directly into PDF forms before printing.

Provider information errors are particularly problematic. Transposing digits in the NPI number or using an outdated tax ID causes automatic rejections. Copy this information directly from your itemized bill—don't try to remember it or look it up independently.

Incorrect billing codes create confusion. If your itemized bill shows one procedure code but you accidentally write a different code on the claim form, the insurer can't match the documentation. Double-check every code you transfer.

Diagnosis codes must support the procedures billed. A claim for a knee X-ray with a diagnosis code for a sinus infection raises red flags. Make sure the codes on your claim form match your itemized bill exactly.

Late submissions past filing deadlines result in automatic denials. Most plans require claim submission within 90-180 days of service, but some allow up to one year. Check your plan documents for the exact deadline.

If you're approaching the deadline, submit what you have rather than waiting for perfect documentation. You can usually supplement with additional records later, but you can't revive a claim denied for late filing.

Mail delays count against you. If your deadline is December 31, mailing on December 30 might result in a January 2 receipt and denial. Build in a buffer.

Author: Lauren Prescott;

Source: blaverry.com

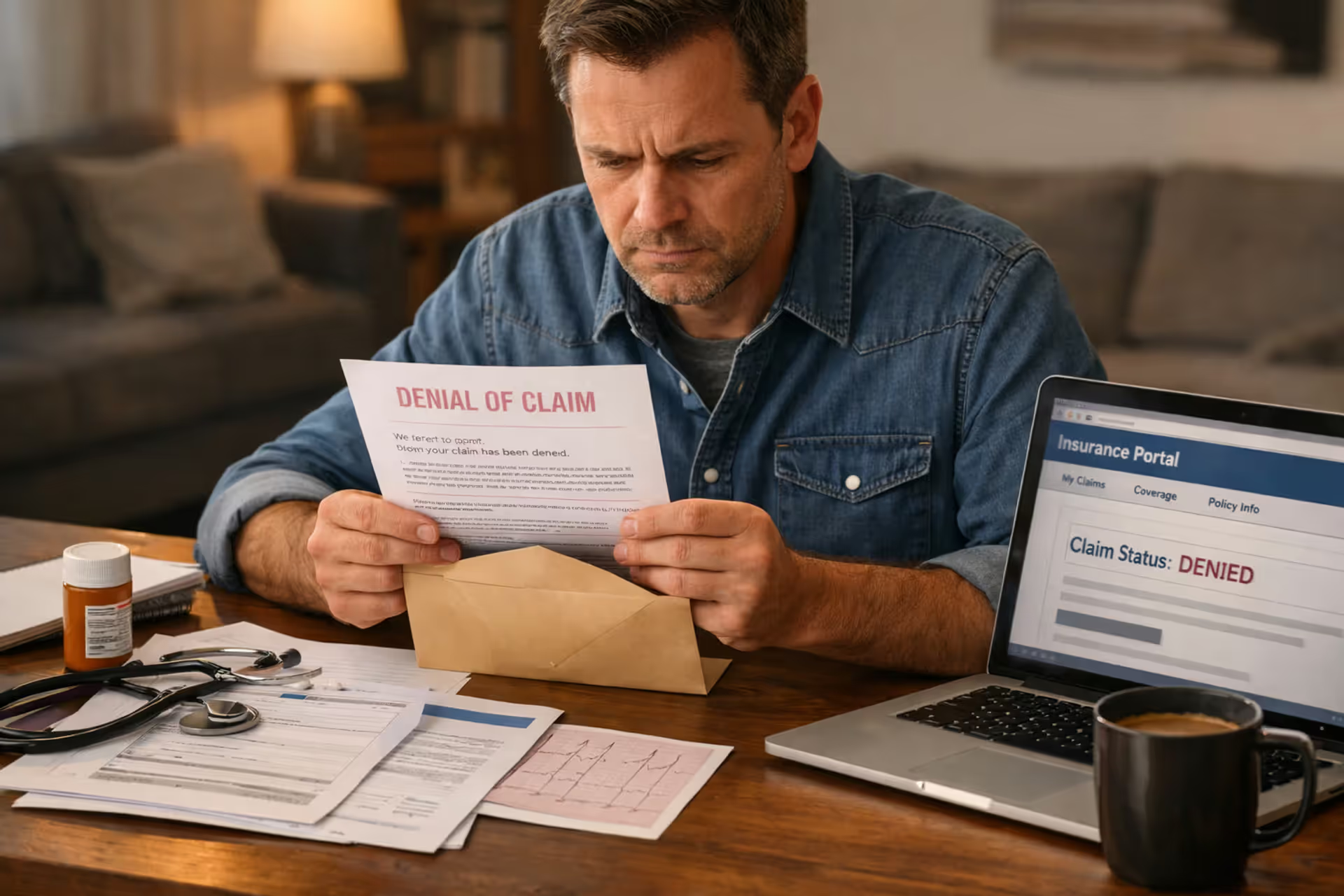

What to Do If Your Claim Is Denied

Denials aren't final. Most can be overturned with the right approach.

Understanding denial reasons starts with reading the denial letter carefully. Common reasons include: service not covered under your plan, lack of medical necessity, out-of-network provider without prior authorization, duplicate claim, or late filing.

Each denial reason requires a different response. If the service isn't covered, an appeal won't help unless you can argue the denial letter misinterprets your plan language. If medical necessity is questioned, you'll need supporting documentation from your provider.

Filing an appeal begins with your insurer's internal appeal process. Submit a written appeal within the timeframe specified in your denial letter—usually 180 days, but verify this.

Your appeal should include: a clear statement that you're appealing the denial, your claim number and member ID, the specific reason you believe the denial is incorrect, supporting documentation (medical records, letters from your doctor, relevant plan language), and your contact information.

For medical necessity denials, a letter from your physician explaining why the service was appropriate for your condition carries significant weight. For coverage disputes, quote the specific plan language that supports your position.

The single biggest mistake people make is failing to submit complete documentation upfront. Insurance companies can only process what you give them. An itemized bill with correct codes, clear proof of payment, and a fully completed claim form will move through the system in a fraction of the time compared to incomplete submissions that bounce back for corrections

— Sarah Mitchell

First-level appeals are reviewed by someone other than the person who made the initial denial. If denied again, you can request an external review by an independent third party.

When to escalate to your state insurance department becomes necessary if your insurer violates state law—for example, by exceeding processing time limits, failing to respond to appeals, or denying coverage for services clearly covered in your plan documents.

State insurance departments can investigate complaints and sometimes compel insurers to pay claims. File a complaint through your state's department of insurance website. Include all documentation: claim forms, EOBs, denial letters, appeal responses, and correspondence with the insurer.

External review and state intervention take months, so pursue these options only after exhausting internal appeals.

Frequently Asked Questions About Submitting Medical Bills

Submitting medical bills to insurance doesn't have to be complicated when you understand the process and prepare properly. Start by gathering complete documentation—itemized bills with correct codes, clear proof of payment, and any supporting medical records. Complete your insurer's claim form carefully, double-checking every field before submission.

Choose electronic submission when available for faster processing and immediate confirmation. Track your claim through your online account and follow up if you don't receive an EOB within 30 days. Read that EOB carefully when it arrives to ensure the claim was processed correctly.

If you encounter denials, don't assume the decision is final. Most denials result from correctable errors or missing information. File appeals with supporting documentation and escalate to external review or state regulators when necessary.

Keep organized records of all submissions, correspondence, and payments. A simple folder—physical or digital—containing claim forms, bills, EOBs, and tracking information saves hours of frustration if questions arise months later.

The reimbursement process rewards attention to detail and persistence. Submit complete, accurate claims on time, and you'll receive the benefits you're entitled to without unnecessary delays or complications.