Insurance policy document on a desk with calculator, coin stacks, miniature house and car models representing insurance deductible concept

What Is an Insurance Deductible and How Does It Work

Content

An insurance deductible represents the money you'll spend from your own pocket before your insurance provider begins paying toward a covered claim. Picture it as your share of the financial responsibility for any loss or medical service your policy covers. Let's say your deductible sits at $500 and you submit a $3,000 claim—you're responsible for the first $500, while your insurance handles the remaining $2,500 (accounting for any additional expenses like copays or coinsurance).

Why do deductibles even exist? Insurance companies use them for two key purposes: preventing customers from filing claims for every minor incident, and maintaining reasonable premium costs by requiring policyholders to shoulder some of the risk. When you commit to covering more expenses upfront whenever you file a claim, your insurer responds by charging you less each month or year. This creates a financial seesaw—what you save regularly versus what you'd spend during an emergency.

You'll encounter deductibles across nearly every insurance category—car insurance, homeowners policies, health plans, and various business coverage options. The dollar amounts swing wildly depending on which policy you purchase, what it covers, and the selections you make when signing up. Getting a solid grasp on deductible mechanics puts you in control of smarter coverage decisions and helps you sidestep nasty financial shocks when submitting claims.

How Insurance Deductibles Work in Practice

Deductibles come into play whenever you submit a qualifying claim, though when and how often depends entirely on what type of insurance you carry. With car and homeowners insurance, you'll encounter the deductible each time something happens. File three separate claims within twelve months? You're paying that deductible three separate times. Health insurance operates on a different calendar—most plans establish an annual threshold that starts fresh every January 1st or whenever your coverage year begins.

Here's something that confuses people: you won't actually mail a check to your insurance company for the deductible. What happens instead is your insurer deducts that amount from whatever they owe you. Say your car needs $2,200 in repairs and your deductible is $500—the insurance company cuts a check for $1,700 to the body shop, and you cover the remaining $500 when you pick up your vehicle.

Author: Derek Whitmore;

Source: blaverry.com

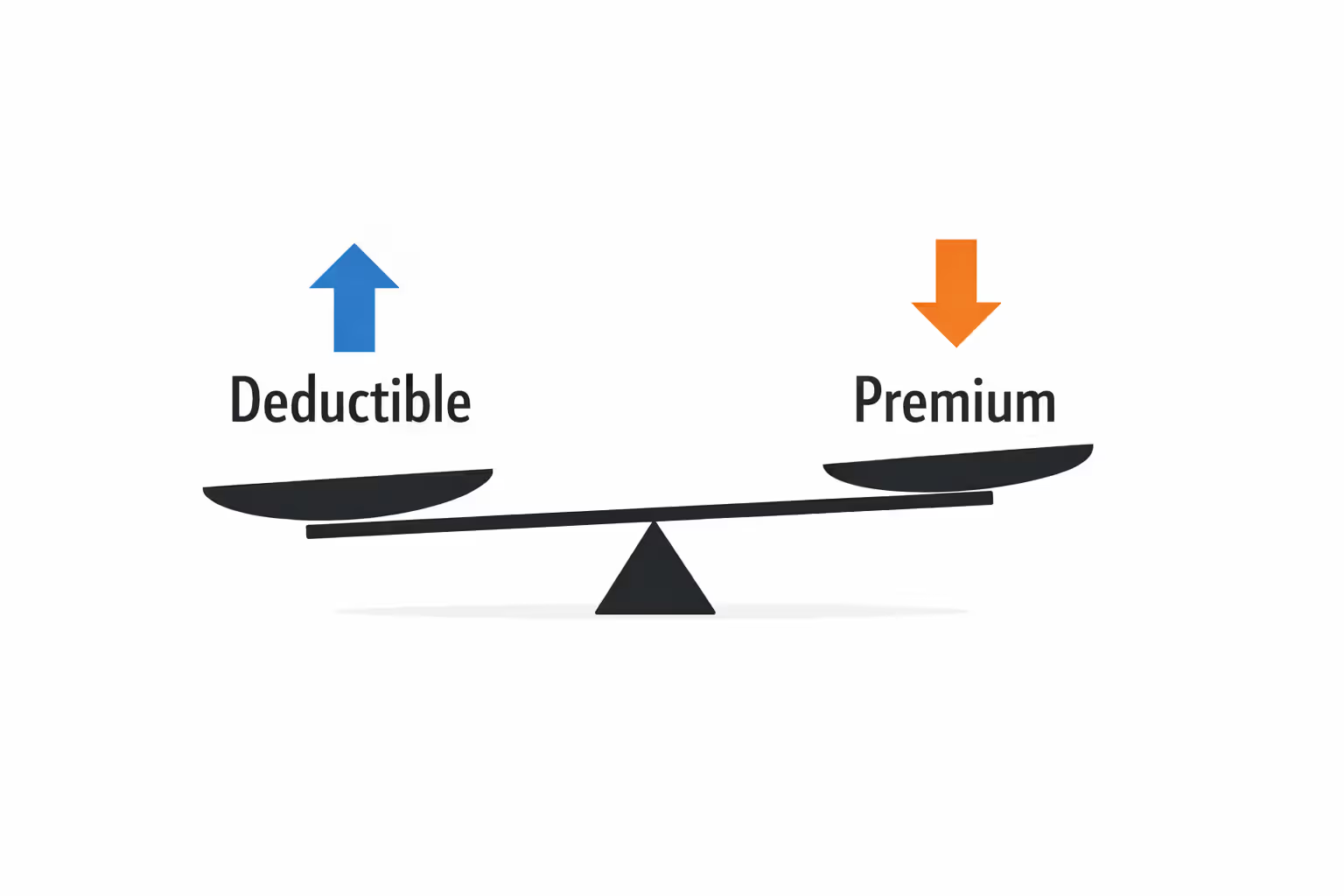

Premiums and deductibles move in opposite directions. Pick a higher deductible, watch your premiums drop. Choose a lower deductible, and your premiums climb. This happens because you're deciding how much financial uncertainty you're comfortable accepting. Selecting a $2,000 deductible tells your insurer you'll handle smaller mishaps yourself, so they reduce what they charge you. Meanwhile, a $250 deductible means your insurance company will be writing checks more often, which they offset by charging higher premiums.

Not everything you do with your insurance triggers the deductible. Most health plans won't touch your deductible for preventive care—think annual physicals, flu shots, and routine screenings. Certain auto policies throw in free glass repair or roadside help without any deductible. Dig into your policy paperwork to discover which services bypass the deductible requirement entirely.

Common Types of Insurance Deductibles

Fixed Dollar Amount Deductibles

You'll run into fixed dollar deductibles more than any other variety. During enrollment, you pick a set figure—commonly $250, $500, $1,000, or $2,500—that stays the same no matter how big or small your claim turns out to be. Choose $1,000 and file a $1,500 claim? You're paying $1,000. File a $50,000 claim next month? Still just $1,000 from your pocket.

This consistency makes planning your emergency fund straightforward. You know precisely what dollar amount you need available when trouble strikes, which takes the guesswork out of financial preparation. Car insurance and homeowners coverage stick almost exclusively to fixed dollar deductibles, presenting you with clear-cut choices when shopping for policies.

Percentage-Based Deductibles

With percentage deductibles, your out-of-pocket expense gets calculated as a slice of your home's total insured value or the claim's full amount. Homeowners insurance brings these out primarily for particular disasters—hurricanes, earthquakes, or major wind events. When you see a 2% deductible on a $300,000 house, you're looking at a $6,000 payment before your coverage activates.

Health plans occasionally deploy percentage arrangements, especially within coinsurance agreements. Once you've satisfied your deductible, you might cover 20% of whatever's left while your insurer handles the other 80%. This split continues until you hit your out-of-pocket ceiling.

Percentage deductibles catch homeowners off guard when they haven't done the actual math. A 5% hurricane deductible sounds reasonable enough until you realize it equals $15,000 on a $300,000 property. Always run the numbers and convert those percentages into real dollars before committing to these policies.

Author: Derek Whitmore;

Source: blaverry.com

Disappearing and Aggregate Deductibles

Disappearing deductibles reward you for staying claim-free by shaving money off what you'd owe. Certain auto insurers knock $50 or $100 off your deductible annually when you don't file claims, sometimes wiping it out completely after five clean years. File one accident claim, though, and you're typically back to square one.

Aggregate deductibles show up mainly in family health coverage. Rather than requiring each person to satisfy their own separate deductible, these policies establish one household cap. After your family collectively reaches that threshold, coverage kicks in for everybody. You might see individual deductibles of $1,500 but a family aggregate of just $3,000—preventing you from paying $9,000 if you've got six people on the plan.

Real-World Insurance Deductible Examples

Auto Accident Scenario

You're sitting at a red light when your foot slips off the brake and you bump the car ahead, causing $4,200 damage to their vehicle and $1,800 to your own. Your policy includes $500 collision coverage and standard property damage liability. Here's where it gets interesting: for the other driver's repairs, your liability coverage cuts a check for the complete $4,200 without touching your wallet—liability claims don't involve deductibles. For fixing your own car's $1,800 worth of damage, you'll pay $500 out of pocket while your collision coverage handles the leftover $1,300.

Home Damage Scenario

Your kitchen catches fire from an unattended stove, leaving behind $18,000 in damage. Your homeowners policy carries a $2,500 deductible. The adjuster approves everything you submitted. Your insurance company writes a check for $15,500, leaving you on the hook for $2,500. When you hire contractors for the repairs, expect to pay them your deductible portion directly while the insurance payment covers the bigger chunk.

Health Insurance Scenario

You're scheduled for surgery with a price tag of $25,000. Your health plan includes a $3,000 annual deductible, 20% coinsurance once you've met that threshold, and a $6,000 out-of-pocket cap. You've already spent $1,200 on your deductible from earlier doctor visits this year. Let's break down the math: You'll pay the outstanding $1,800 to satisfy your deductible first. That leaves $23,200 subject to coinsurance—you're responsible for 20% ($4,640) while insurance covers 80% ($18,560). But here's the twist: your $1,800 deductible payment combined with that $4,640 coinsurance totals $6,440, pushing you past your $6,000 maximum. Your actual payment caps at $6,000, and insurance picks up the remaining $19,000.

Author: Derek Whitmore;

Source: blaverry.com

Homeowners Percentage Deductible

A brutal windstorm tears up your roof, requiring $12,000 worth of repairs. Your policy specifies a 2% wind and hail deductible based on your home's $400,000 insured value. Your deductible equals $8,000 (2% of $400,000)—not 2% of the $12,000 claim amount. You'll pay $8,000 while insurance covers just $4,000. Had you gone with a standard $1,000 fixed deductible for wind damage instead, you'd be paying considerably less, though your monthly premiums would run higher.

How to Choose the Right Deductible Amount

Picking your deductible comes down to juggling three elements: how much money you've got sitting in emergency savings, how likely you are to file claims, and what you can afford in monthly premiums. Start by taking an honest look at your accessible cash. Financial experts recommend setting your deductible at whatever amount you could pay immediately without creating hardship. Got $2,000 in emergency funds? Then a $2,500 deductible puts you in a vulnerable position—one claim could wipe out your safety net and push you toward credit card debt.

Think about your personal risk situation and claims track record. Filed several car insurance claims over the past few years? A lower deductible shields you from paying large amounts repeatedly. Haven't filed anything in ten years? A higher deductible lets you pocket the premium savings you'd never reclaim otherwise. If you own a home in tornado alley or hurricane country, lower deductibles make more sense given the elevated probability of weather damage.

Run the actual numbers on premium differences between your deductible options. Ask for quotes comparing annual costs at $500, $1,000, and $2,000 deductibles. Say bumping your deductible from $500 to $1,000 saves you $150 each year—you'd need to go 3.3 claim-free years ($500 difference ÷ $150 annual savings) just to break even. Most drivers find those odds appealing, particularly since careful driving keeps many risk factors under your control.

Don't ignore your personal comfort level with financial uncertainty. Some folks rest easier knowing they'll face smaller bills during a crisis, even when it means paying more every month. Others would rather keep extra cash available now and accept the possibility of a bigger expense later. Neither philosophy is incorrect—it's about matching your coverage to your financial personality and current situation.

Make deductible review part of your annual routine. As your emergency fund grows or your income improves, raising deductibles could trim hundreds from your premium costs. Conversely, if you've added new debt or your savings took a hit, lowering your deductible adds protection when you're financially stretched.

How Deductibles Affect Your Insurance Premiums

The deductible level you select creates an immediate impact on your coverage costs. Insurers adjust what they charge based on how often they expect to pay claims and how much those claims will cost. Agreeing to higher deductibles cuts their anticipated expenses, which translates directly into lower premiums for you.

| Your Deductible | Auto Policy (Annual) | Homeowners Policy (Annual) | Health Plan (Monthly) |

| $250 | $1,640 | $1,580 | $520 |

| $500 | $1,380 | $1,320 | $465 |

| $1,000 | $1,150 | $1,095 | $410 |

| $2,500 | $980 | $890 | $355 |

These premium figures reflect national averages for typical coverage and fluctuate based on where you live, how much coverage you purchase, and your individual risk factors.

The percentage you save grows larger as deductibles increase, but not in a straight line. Jumping from $250 to $500 might cut your premium by 15%, while leaping from $1,000 to $2,500 might only shave another 12%. This diminishing payoff means extremely high deductibles don't always deliver worthwhile savings unless you've built substantial emergency funds and hardly ever file claims.

Most families hit the sweet spot with a deductible matching one month's take-home pay. That amount generates real premium savings while remaining manageable enough that you won't derail your finances when filing a claim. I've watched too many clients pick $5,000 deductibles to save $40 monthly, then face impossible financial decisions when they actually need their coverage

— Sarah Mitchell

Where you live influences the deductible-premium equation significantly. Coastal homeowners deal with substantial percentage-based hurricane deductibles that create dramatic premium swings. City drivers might notice smaller premium gaps between deductible tiers compared to rural drivers, since urban base rates already account for elevated theft and collision frequency.

Common Mistakes People Make With Deductibles

Selecting a deductible beyond your financial reach tops the list of frequent errors. People get drawn to dramatically lower premiums, then find themselves in crisis mode when they actually need to file a claim. Can't access your deductible amount within 30 days without borrowing or missing other financial obligations? You've set it too high.

Plenty of policyholders mix up deductibles with copays or coinsurance, treating them as interchangeable terms. That $30 you pay for doctor visits doesn't chip away at your health insurance deductible on most plans. You could make copay after copay throughout the year and still owe your complete deductible when you need surgery. Coinsurance works differently too—it's your percentage responsibility for costs after satisfying the deductible, representing separate expenses on top of what you've already paid.

Another common assumption: your deductible applies uniformly across all claim types. Reality check—your comprehensive auto coverage might carry a different deductible than your collision coverage. Homeowners policies frequently include separate deductibles for everyday perils versus hurricanes or earthquakes. Always verify which deductible applies to your specific situation before submitting paperwork.

Filing small claims barely exceeding your deductible frequently backfires. A $1,200 claim when you carry a $1,000 deductible nets you just $200 but could trigger rate increases or even non-renewal. Insurance providers track claim frequency closely, and multiple minor claims raise bigger red flags than one substantial claim. Consider covering small damages yourself to keep your claims record clean.

Neglecting to update deductibles when your financial picture changes either wastes money or exposes you to unnecessary risk. That $250 deductible made perfect sense when you had three kids and tight cash flow, but now as an empty-nester sitting on healthy savings, you're overpaying for protection you don't require.

Author: Derek Whitmore;

Source: blaverry.com

Frequently Asked Questions About Insurance Deductibles

Grasping how insurance deductibles function gives you the knowledge to make coverage choices that fit your actual financial situation. Your deductible selection influences both what you pay regularly for premiums and how much you'll spend during claims, creating a balance that should mirror your available savings, comfort with risk, and probability of needing to file.

There's no universal "correct" deductible—it's deeply personal. Take a realistic inventory of your emergency fund, compare premium costs across various deductible levels, and factor in your claims history before committing. Remember you're not locked in forever—adjust your deductible as circumstances evolve, and recognize that different insurance types might warrant different deductible approaches.

Steer clear of typical pitfalls like choosing deductibles that exceed your liquid savings or confusing them with other out-of-pocket expenses. When you've got clarity on exactly what you'll pay and when those payments occur, budgeting becomes manageable and you avoid unpleasant surprises during claims. Spend a few minutes reviewing your current deductibles to confirm they still align with where you are financially—that small time investment could save you hundreds annually or protect you from serious financial strain when you actually need your coverage working for you.