Wallet with dollar bills and health insurance card next to calculator and stethoscope on wooden desk

Copay vs Coinsurance Explained for Health Insurance

Content

Your monthly premium gets auto-drafted every month like clockwork. That payment keeps your policy alive, sure—but it doesn't cover the actual medical care you receive.

When you walk into a doctor's office or hospital, two completely different billing systems determine what you'll owe. They're called copays and coinsurance, and they calculate your responsibility using opposite math.

One charges identical amounts every single time you use a service. The other changes based on the total cost of whatever treatment you received.

Most people can't tell you which one applies to their upcoming appointment. They assume they'll pay their standard $30 fee, then open a bill for $315 and panic. What happened? That first visit used copay pricing. The second one switched to coinsurance without warning.

Let me walk you through when each kicks in, the formulas that determine what you owe, and why identical medical appointments sometimes cost nine times more than you expected.

What Is a Copay?

Think of copays as set prices your insurance company establishes ahead of time. These dollar amounts appear right on your insurance card, and they don't budge no matter what the doctor actually bills.

Copay meaning: You hand over a predetermined dollar amount when getting medical care. Whatever the provider charges beyond that flat fee? Your insurer handles it.

Here's what you'll typically see:

- Primary care visits: Between $25 and $40 each time

- Specialist consultations: Anywhere from $50 to $75 per appointment

- Urgent care facilities: Usually $75 to $100 when you show up

- Emergency departments: Often $150 to $300 per visit

- Generic medications: Around $10 to $15 when you pick them up

- Brand-name drugs: Generally $40 to $80 per prescription

Flip your insurance card over right now. See those numbers? "PCP $35" means primary care copay. "Spec $65" means specialist copay. "Urg $85" means urgent care.

Let me give you a real scenario. You book an appointment with your family doctor because you've been getting killer migraines. Your card lists a $35 primary care copay. You pay $35 at checkout—period. Doesn't matter if your doctor bills the insurance company $165 or $240 or $310 for that visit. Your portion stays at $35.

That predictability defines how copays work. Picking up your thyroid medication on Friday? You already know it'll cost $12. Scheduled your annual dermatology check for next month? That $60 stays locked in.

But copays have limits. They only cover certain types of services—mostly office appointments and prescription pickups. Need bloodwork or an MRI? Those usually fall under different rules entirely.

What Is Coinsurance?

Coinsurance throws fixed pricing out the window. You pay a slice of the total bill—expressed as a percentage—after you've knocked out your yearly deductible.

Coinsurance meaning: The portion of medical expenses you're responsible for, calculated as a percentage (anywhere from 10% to 40%), that kicks in once you've met your deductible.

Whatever percentage you don't pay? That's what your insurer covers. Let's say your plan document shows "80/20 coinsurance." You pay 20% of the bill. Your insurance company picks up the other 80%.

Here's how it plays out. You're playing pickup basketball, land wrong, and tear your rotator cuff. The MRI costs $1,500. You already hit your deductible back in March. Your plan includes 20% coinsurance. You're writing a check for $300. Your insurer sends the imaging center $1,200.

Coinsurance usually applies to bigger-ticket items:

- Hospital admissions

- Surgical procedures

- MRI and CT scans

- Ambulatory surgery centers

- Physical therapy sessions

- Durable medical equipment

- Specialty-tier prescription drugs

Notice something? These are expensive services with massive price swings. Basic outpatient surgery might run $850. Complex orthopedic surgery could hit $28,000. With 20% coinsurance, you'd owe $170 for that simple procedure but $5,600 for the complicated one.

That's the headache with percentage-based responsibility. You can't know your exact cost until the provider sends the final bill and your insurer finishes processing everything. Makes it tough to budget, unlike those predictable copays.

Critical timing note: coinsurance doesn't even start until you've wiped out your annual deductible. Before that threshold? You're covering 100% of these services yourself (except preventive care, which federal law requires insurers to cover completely).

Key Differences Between Copay and Coinsurance

The difference between copay and coinsurance boils down to how they're calculated, when they activate, and whether you can predict what you'll owe.

| Feature | Copay | Coinsurance |

| What it is | Set dollar amount per service | Percentage of the total charges you split |

| Calculation method | Your plan sets it (like $40) | Percentage of negotiated rate (like 20%) |

| Payment timing | Starts immediately, usually before you touch your deductible | Only activates after you've satisfied your deductible |

| Amount range | Generally $10 to $300 depending on the service | Typically 10% to 40% of what the provider bills |

| Cost certainty | You know the exact amount every time | Changes based on the final bill |

| Typical services | Office visits, prescriptions, urgent care | Hospital stays, surgery, imaging, therapy |

How they calculate differently: Copays completely ignore what the service actually costs. Your physical therapist might charge $195 one session and $275 the next—you hand over the same $50 copay both times. Coinsurance ties directly to the bill. Higher charges automatically mean you pay more. Lower charges mean you pay less.

When they kick in: Visit your primary doctor on January 8th with a plan that includes $35 copays? You're paying $35—even though you haven't made a dent in your $2,500 annual deductible yet. But book a CT scan that same week? When your plan uses coinsurance for diagnostic imaging, you'll likely pay the complete negotiated rate until that deductible gets satisfied first.

The predictability factor: Copays eliminate surprises. Your asthma inhaler costs $25 every single refill—January, July, December, doesn't matter. Coinsurance introduces variables you can't control. That cardiology consultation might cost you $92 or $218 depending on billing codes and what the cardiologist actually charges your insurance.

People tell me they've paid $40 at every single doctor visit for ten months straight, then act totally blindsided when a hospital bill shows they still owe $1,950 toward their deductible. Those copays never touched it. That's what trips people up—thinking their copays were chipping away at the deductible when those two systems run on separate tracks

— Sarah Mitchell

Which costs less overall? Neither one wins automatically. Someone seeing doctors twice a month while avoiding hospitals could rack up more in copays annually. Someone needing surgery faces potentially brutal coinsurance bills even if they're paying lower premiums each month.

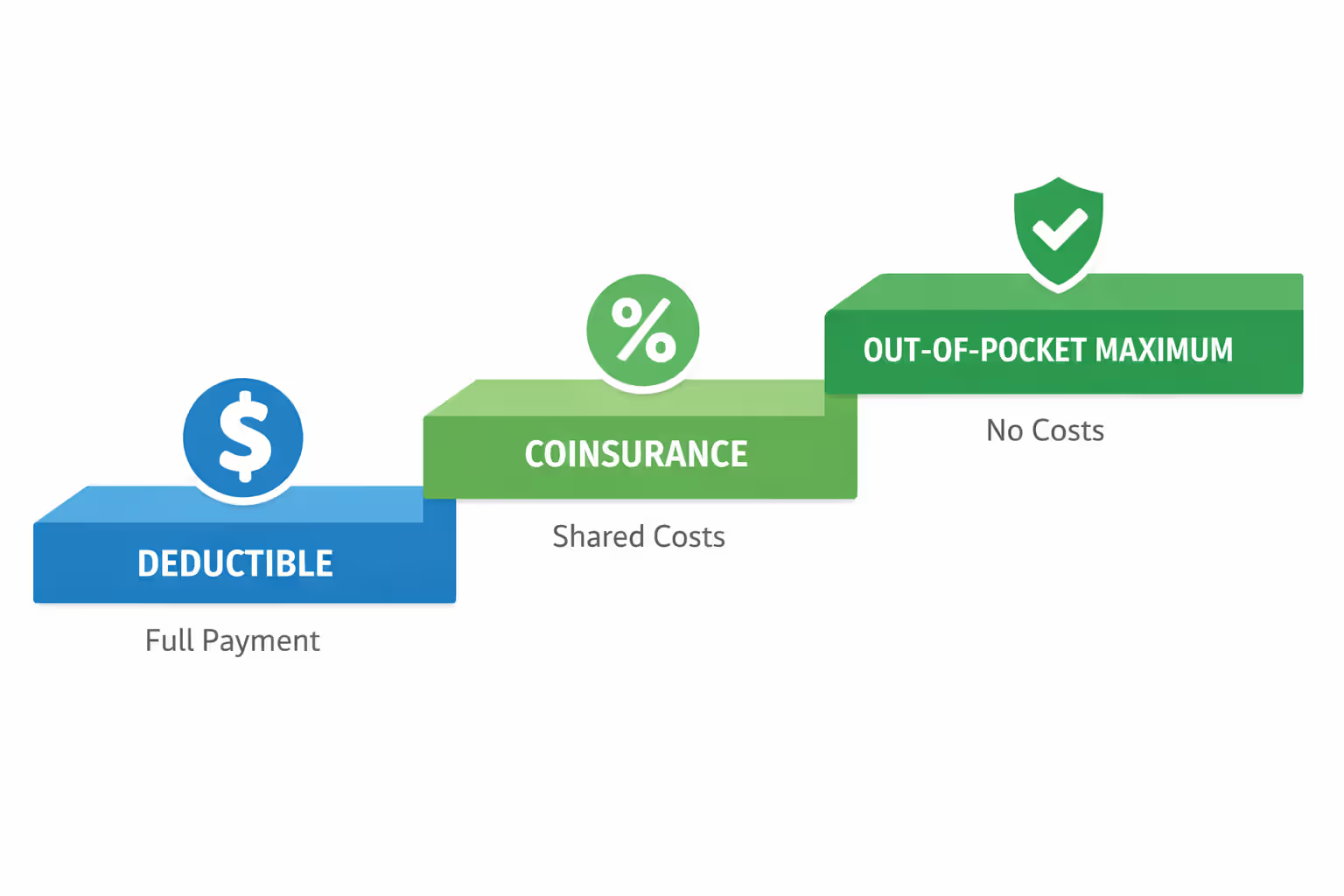

How Copays and Coinsurance Work With Your Deductible

The copay vs deductible connection confuses more Americans than almost any other insurance concept.

Your deductible represents what you must spend on covered services before your plan starts splitting costs with you through coinsurance. Looking at 2026 data, typical individual deductibles run between $1,000 and $3,000 for standard plans. High-deductible options start around $1,600 and climb from there.

Your spending throughout the year typically moves through three stages:

Stage 1: Before you've met your deductible - Services with copays: you pay whatever your card shows - Everything else: you cover the full negotiated cost - Those copay payments? They usually don't touch your deductible - Full-price services you pay? Those generally do count toward it

Stage 2: After you've satisfied your deductible

- Services with copays: same amounts as before - Services that were full-price: now split according to your coinsurance percentage - Everything you pay now counts toward your out-of-pocket maximum

Stage 3: After hitting your out-of-pocket maximum - You pay zero for covered services the rest of the year - Your insurer covers 100% of allowed amounts through December 31st

Real timeline: Maria's plan includes a $2,000 deductible, $35 copays for primary care, and 20% coinsurance for everything else once she meets that deductible.

Author: Derek Whitmore;

Source: blaverry.com

January through March: She visits her doctor three times at $35 each—that's $105 in copays. She also needs lab work that costs $600. She pays the entire $600 (which counts toward her deductible), but those three copays don't count at all. What she's spent: $705. Deductible progress: only $600.

Early April: Her doctor orders an MRI priced at $1,800. She still owes $1,400 more to hit that $2,000 deductible ($2,000 minus the $600 already credited). She pays $1,400. Deductible: complete.

Late May surgery: Hospital bills $8,000. Her deductible is done, so coinsurance takes over. She owes 20% of $8,000, which comes to $1,600.

June through December: Office visits still run $35 each time. Any major services trigger that 20% coinsurance until she maxes out her annual out-of-pocket limit.

Special carve-out: Preventive services—annual wellness exams, most screenings, recommended vaccinations—cost you nothing under federal law. No copay, no coinsurance, no deductible. The insurer covers these at 100% before you've spent a penny.

The copay-deductible question: Do copays count toward your deductible? Almost never. They typically count exclusively toward your out-of-pocket maximum while skipping right past your deductible. You could pay copays at appointments for the entire year and still owe your complete deductible when something expensive happens. A tiny handful of plans count copays toward both, but that's extremely rare. Your Summary of Benefits and Coverage spells out your plan's actual rules—don't guess.

Real-World Examples of Copay and Coinsurance Costs

Let me show you actual scenarios with real dollar amounts. These coinsurance example situations happen to millions of people every year.

Scenario 1: Managing chronic health issues

James has PPO coverage with a $1,500 deductible, $30 copays for primary care, $60 copays for specialists, and 20% coinsurance on everything else.

February rolls around and his back pain becomes unbearable. He visits his primary doctor: pays $30 at the front desk. His doctor sends him to an orthopedist. Specialist visit: pays $60 when he checks in. The orthopedist orders X-rays costing $250—but James hasn't touched his deductible yet, so he pays the full $250 out of pocket.

February total expenses: $340 ($30 + $60 + $250) Deductible progress: Just $250 (X-rays count; those copays don't)

Scenario 2: Emergency triggering multiple payment types

Lisa carries high-deductible coverage: $3,000 deductible, $100 emergency room copay, 30% coinsurance after meeting the deductible.

She's playing basketball, lands awkwardly, fractures her ankle badly. Emergency room charges hit $2,500. She pays the $100 ER copay right away, plus the remaining $2,400 toward her deductible—total of $2,500 walking out that night.

Two weeks later: She needs surgery to repair the fracture—total bill of $12,000. She still owes $600 to finish that $3,000 deductible. After that, coinsurance kicks in on the remaining $11,400. Thirty percent of $11,400 equals $3,420.

Her complete cost from one injury: $6,520 (broken down as $2,500 at the ER, $600 finishing the deductible, plus $3,420 in coinsurance)

Author: Derek Whitmore;

Source: blaverry.com

Scenario 3: Chronic condition requiring regular medication

Robert manages diabetes with two daily medications. His plan charges $15 copays for generics, $50 for brand-name drugs. He takes one of each—$15 monthly for metformin, $50 monthly for brand-name insulin.

Annual prescription costs: ($15 + $50) × 12 months = $780

Quarterly diabetes checkups with his primary doctor: $35 copay × 4 visits = $140 Lab work twice yearly: $300 total cost, but his $2,000 deductible never gets met, so he pays full price = $300

His complete annual cost: $1,220 out-of-pocket

Here's what stings: None of those copay payments helped him reach his deductible. If Robert lands in the emergency room or needs surgery, he starts from scratch—still owes that entire $2,000 deductible before coinsurance would start reducing his costs.

Which Health Plans Use Copays vs Coinsurance?

Different insurance structures take dramatically different approaches to splitting costs through copays versus coinsurance.

HMO (Health Maintenance Organization) plans lean heavily on copays. You'll pay flat amounts for almost everything—primary appointments, specialist visits, emergency care, prescription drugs. HMOs rarely touch coinsurance except for hospital stays or major surgery. This copay-heavy structure keeps costs predictable and pushes members to stay in-network where copays remain lowest.

PPO (Preferred Provider Organization) plans blend both methods. Expect copays for routine appointments and medications, but coinsurance takes over for hospitals, surgeries, diagnostic imaging, and ongoing therapy. PPOs often charge different coinsurance rates depending on network status (maybe 20% in-network but 40% or 50% if you go out-of-network).

Author: Derek Whitmore;

Source: blaverry.com

HDHP (High-Deductible Health Plans) paired with HSAs often eliminate copays entirely. Many charge zero as a copay—you pay complete negotiated rates for everything until satisfying that high deductible (minimum $1,600 for individual coverage in 2026), then coinsurance kicks in. Some HDHPs include limited copays for specific services, though this gets less common each year.

EPO (Exclusive Provider Organization) plans mirror HMOs with their copay emphasis, though some layer in coinsurance for expensive procedures.

Medicare Advantage plans (covering people 65 and older) typically structure costs as copays throughout—fixed amounts for doctor visits, specialists, even daily hospital charges (like "$350 per day for days 1 through 5 of hospitalization").

Employer-sponsored coverage varies wildly. Large companies with serious negotiating power might design custom plans combining generous copays for preventive and primary care while applying coinsurance for specialty services. Smaller employers often choose simpler designs dominated by one primary cost-sharing method.

Shopping during open enrollment? Match plan design to how you actually use healthcare:

- Frequent doctor visits but rarely hospitalized? Plans built around low copays might save money even if coinsurance rates run higher.

- Generally healthy, mainly want catastrophic protection? HDHPs with coinsurance-only structures and lower premiums could work great—especially if you can max out an HSA.

- Managing chronic conditions requiring specialists and procedures? Run the math both ways—estimate your expected annual spending under copay-heavy versus coinsurance-heavy plans using your actual service usage from last year.

Frequently Asked Questions About Copays and Coinsurance

Copays and coinsurance represent fundamentally different philosophies about splitting medical expenses. Copays establish fixed amounts that stay constant—making your budget completely transparent. Coinsurance links your costs directly to the service's actual price—creating variability but generally lowering your monthly premiums.

Stop worrying about which approach is "superior" in abstract terms. Your health status, anticipated medical needs, and financial circumstances determine what works for your situation. Someone managing a chronic condition with monthly doctor appointments probably benefits from low copays, even if premiums run higher. Someone in excellent health might prefer a high-deductible plan using coinsurance only—accepting uncertainty for lower monthly costs and HSA tax advantages.

Real financial clarity comes from understanding how these payment mechanisms interact with your deductible and out-of-pocket maximum. That's your complete picture of maximum annual spending. During open enrollment, skip the mistake of comparing premiums alone—calculate different scenarios using your actual healthcare usage, regular prescriptions, scheduled appointments, and tolerance for unexpected medical bills.

Grab your insurance card, locate your Summary of Benefits and Coverage, and review your plan documents to know exactly what you'll pay for your most frequently used services. This preparation prevents billing shocks and helps you make smarter decisions about your healthcare throughout the year.