How to Bill Health Insurance for Auto Accident Injuries

How to Bill Health Insurance for Auto Accident Injuries

Content

Medical expenses after a fender-bender or serious collision can drain your savings fast. Here's something many accident victims don't realize: your regular health coverage might pick up these bills, even though you'd expect auto insurance to handle them.

But there's a catch—actually, several catches. Your policy's fine print, where you live, and how your accident happened all determine whether your health plan will cover anything at all.

Getting your health insurer to pay for crash-related injuries takes more than just submitting a claim form. You'll need the right paperwork, perfect timing, and a clear understanding of which insurance should pay first. This comprehensive guide shows you exactly how to navigate the billing maze so you're not stuck with thousands in unpaid medical bills.

When Health Insurance Covers Auto Accident Medical Bills

Your health plan can absolutely pay for injuries from vehicle crashes, though it typically won't jump in as the first payer. Think of it as backup coverage that activates under specific conditions.

Here's how the payment hierarchy usually works: auto insurance medical coverage takes priority. Your health benefits generally kick in only after you've tapped out those auto policy limits. Insurance companies call this "coordination of benefits"—a bureaucratic term that basically means figuring out who pays what and when.

Your health policy likely includes coverage for accident injuries. That said, buried in your member handbook you'll probably find language stating you must use available auto insurance first. So if your car insurance includes personal injury protection (PIP) or medical payments (MedPay) provisions, those dollars get spent before your health plan contributes a dime.

Where you live matters tremendously. Michigan, Florida, New York, and about a dozen other states operate under no-fault systems that mandate PIP coverage. In these places, your auto insurer handles medical bills automatically after a crash, regardless of who caused it. Your health insurance stays on the sidelines until those PIP benefits run dry. Meanwhile, in traditional fault-based states, your health coverage might become primary immediately if the other driver lacks sufficient liability protection or if you're still hammering out a settlement.

Your health benefits move into the primary position when:

- Your auto policy lacks medical expense coverage (no PIP, no MedPay provisions)

- You've burned through your auto insurance medical limits

- You were walking or cycling and don't have your own auto policy

- You were riding in someone else's car and their coverage won't stretch far enough

One complication you should know about: your health insurer will likely place a lien on any eventual settlement from the at-fault party. This recovery process—known as subrogation—lets them recoup what they paid for injuries someone else caused. You'll need to inform them about the accident and any potential third-party claims you're pursuing.

Some health plans specifically carve out motor vehicle accidents from coverage. Check your policy's coordination of benefits language and scan for any exclusions mentioning auto accidents. When the language seems murky, call member services before scheduling that first doctor's appointment.

Author: Ethan Bradford;

Source: blaverry.com

Steps to Bill Your Health Insurance After a Car Accident

Getting your health plan to pay accident-related medical bills isn't complicated, but timing and thoroughness make all the difference. Skip a crucial step, and you're looking at claim denials and unexpected bills.

Notify Your Health Insurer Within Required Timeframes

Get on the phone with your health insurance within the first day or two after the collision. Why so fast? Most policies have language requiring immediate notification when an accident might involve another party's liability. This early heads-up protects your coverage and helps them sort out payment responsibilities.

When you make that first call, share the basics: what day it happened, where, how many vehicles were involved, whether police came to the scene. Ask pointed questions about your policy's accident coverage and if they'll need any special forms beyond standard claim paperwork.

Write everything down from this conversation. The rep's full name, exact time you called, any confirmation or reference numbers they gave you. Request an email confirming they've documented your accident notification.

While you should notify them immediately, you'll typically have 30 to 90 days from each medical appointment to actually file claims with supporting documents. Don't confuse notification deadlines with claim submission deadlines—they're different animals.

Submit Required Documentation and Claim Forms

Pull together your paperwork before submitting anything. Your insurer needs proof connecting your medical treatment to the accident and evidence showing what other coverage exists or has been exhausted.

Fill out their standard claim form completely, but watch for supplemental accident questionnaires. These additional forms dig into specifics: detailed accident circumstances, information about other drivers involved, their insurance details, whether you've hired an attorney.

Attach photocopies (never your originals) of:

- The police report with its case number

- Medical documentation from the ER, urgent care, or your doctor

- Itemized statements from every provider who treated you

- Any explanation of benefits paperwork from your auto insurer showing what they paid

- A written narrative explaining exactly how the collision occurred

Send everything through whatever channel they prefer—their member portal, secure fax, or certified mail. Keep duplicates of every single page and get confirmation they received your submission.

Author: Ethan Bradford;

Source: blaverry.com

Track Your Claim Status and Follow Up

Expect processing to take 30 to 45 days for straightforward cases. Complex accident situations involving multiple insurers might drag on longer.

Check claim status weekly through their online system or by calling. Don't assume silence means everything's fine.

When they request more information, respond that same day if possible. Slow responses to documentation requests often trigger automatic denials.

Your explanation of benefits will arrive by mail showing what they paid, denied, or credited toward your deductible. Scrutinize it for mistakes—wrong billing codes or incorrect service dates cause improper claim rejections.

If you hit 45 days without payment or explanation, escalate to a supervisor. Keep a log of every follow-up call with dates, names, and what they told you.

Documentation You Need for Auto Accident Health Insurance Claims

Solid documentation separates claims that sail through from those that get rejected. Even one missing piece can stall processing for weeks.

| Document Type | Where to Obtain | Typical Processing Time |

| Official police crash report | Your local police department or highway patrol office | 3 days to 2 weeks post-accident |

| Complete medical records and itemized bills | Billing departments at hospitals, clinics, and doctor's offices | Same day up to one week |

| Auto insurance explanation of benefits (if you've filed there) | Your auto insurance claims department | 2 weeks to one month after filing |

| Supplemental accident questionnaire | Your health plan's website or claims department | Available immediately online |

| Photographic evidence of crash scene and injuries | Your phone or the police report | Take these immediately at the scene |

| Any witness contact information and statements | Directly from witnesses or included in police documentation | Within hours to 3 days |

| Proof of missed work and wages (when applicable) | Your employer's HR or payroll department | 24 hours to 3 business days |

Begin gathering this documentation the day of the accident, not when you're ready to file. Some records become harder to access as weeks pass.

Put your medical record requests in writing to each provider. Be specific: "I need all records related to treatment for injuries from the motor vehicle collision on

for insurance claims." Expect copying charges, usually 25 cents to a dollar per page.Set up a filing system—physical folder or digital—exclusively for accident paperwork. Organize everything by date and maintain a checklist tracking what you've collected and what you're still waiting on.

Make three copies of everything. One set stays with you, one goes to insurance, and keep another available for potential legal proceedings if fault disputes arise.

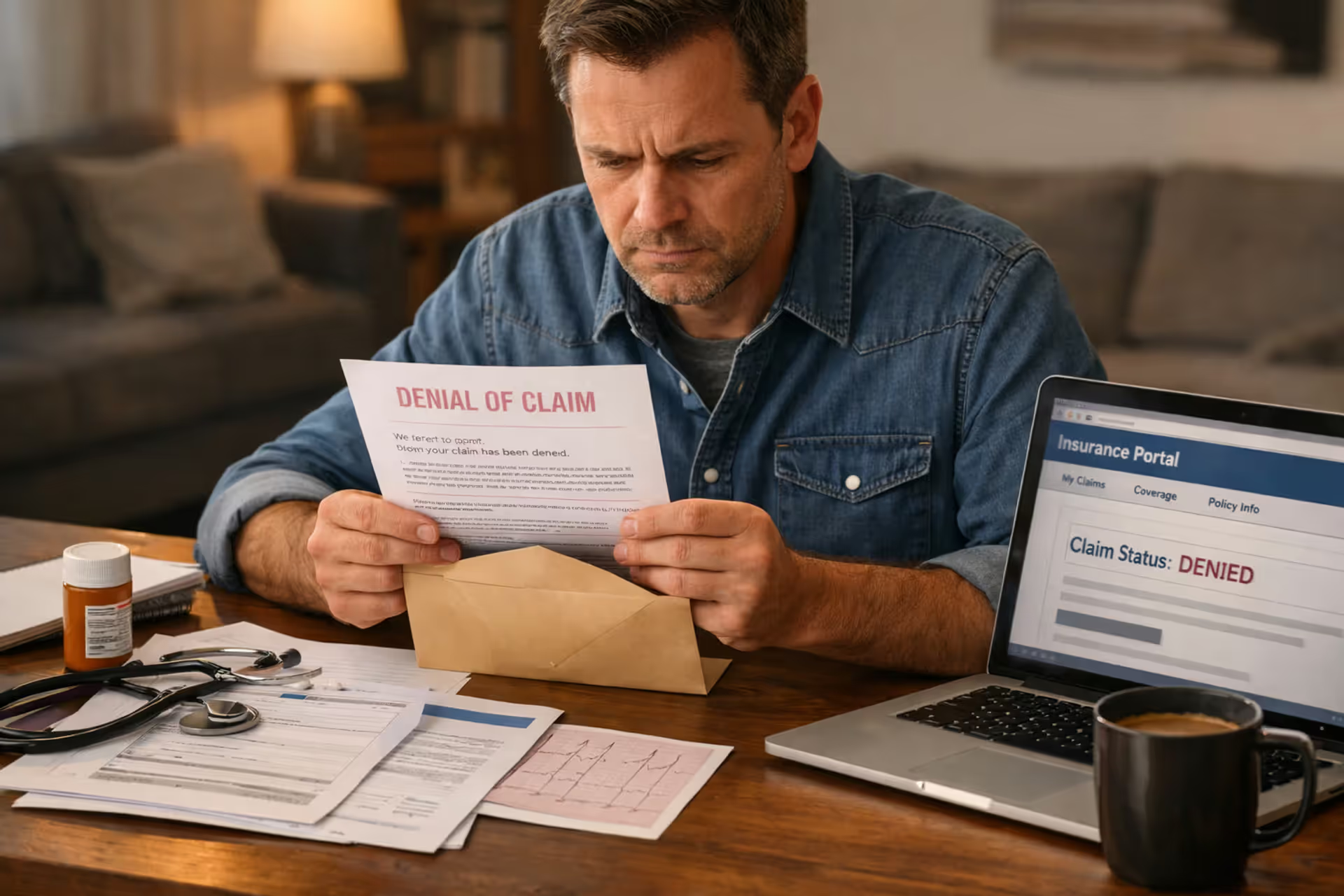

What to Do If Your Health Insurance Denies Your Auto Accident Claim

Claim rejections happen constantly with vehicle accident injuries, but here's the good news: proper documentation and persistence reverse most denials.

Common Reasons for Claim Denials

Knowing why claims fail helps you either prevent problems upfront or build winning appeals.

Coordination of benefits confusion: This tops the list. Your insurer thinks auto coverage should pay first, or they suspect you haven't maxed out available auto benefits. This happens when you fail to clearly prove your auto insurance limits are gone or that you have zero auto coverage.

Missed deadlines: Blowing past your policy's accident reporting or claim filing windows triggers automatic rejections. Even legitimate claims with perfect documentation get tossed for timing violations.

Incomplete paperwork: Claims missing police reports, detailed accident narratives, or clear proof linking injuries to the crash date get denied. Vague medical notes that don't explicitly tie injuries to the specific accident create doubt.

Coverage exclusions: Certain health plans completely exclude motor vehicle injuries, forcing members to rely entirely on auto insurance. This exclusion should appear somewhere in your policy documents, though finding it takes digging.

Third-party liability determinations: When your insurer decides another party is obviously at fault and carries adequate insurance, they may reject the claim while waiting for that liability settlement.

Duplicate billing attempts: Submitting claims for services your auto insurance already paid triggers rejections for duplicate payment.

How to Appeal a Denied Health Insurance Claim

Author: Ethan Bradford;

Source: blaverry.com

Every denied claim gives you appeal rights. Insurers provide multiple appeal levels, and success rates run surprisingly high when you present solid evidence.

Within five days of getting that denial letter, request your complete claim file. Study the denial letter closely—it must specify exactly why they rejected it and outline your appeal options.

Launch your first appeal within the deadline stated in your denial (typically 180 days). Write a straightforward, fact-based appeal letter targeting their specific rejection reason:

- For coordination of benefits rejections: Supply proof your auto coverage is exhausted or doesn't exist (like your auto policy declarations showing no medical coverage, or explanation of benefits showing you've hit limits)

- For documentation rejections: Provide the missing records with a cover letter explaining why they weren't in your initial submission

- For late filing rejections: Explain any special circumstances and provide evidence you notified them on time if you did

Attach supporting evidence: letters from your auto insurer confirming exhausted coverage, physician letters explicitly connecting injuries to the accident date, corrected forms, or additional medical documentation.

Mail appeals via certified delivery with return receipt requested. Duplicate everything you send.

First appeals usually resolve within 30 days. If denied again, request a second-level review, often handled by different claims staff or a medical review panel. This level may take 60 days.

When internal appeals fail, you can demand an external review by an independent reviewer. Your state insurance department manages this process. External reviewers overturn roughly 40% of denials.

For significant amounts, consider hiring a patient advocate or healthcare attorney. Some work on contingency, collecting a percentage only when they recover payment.

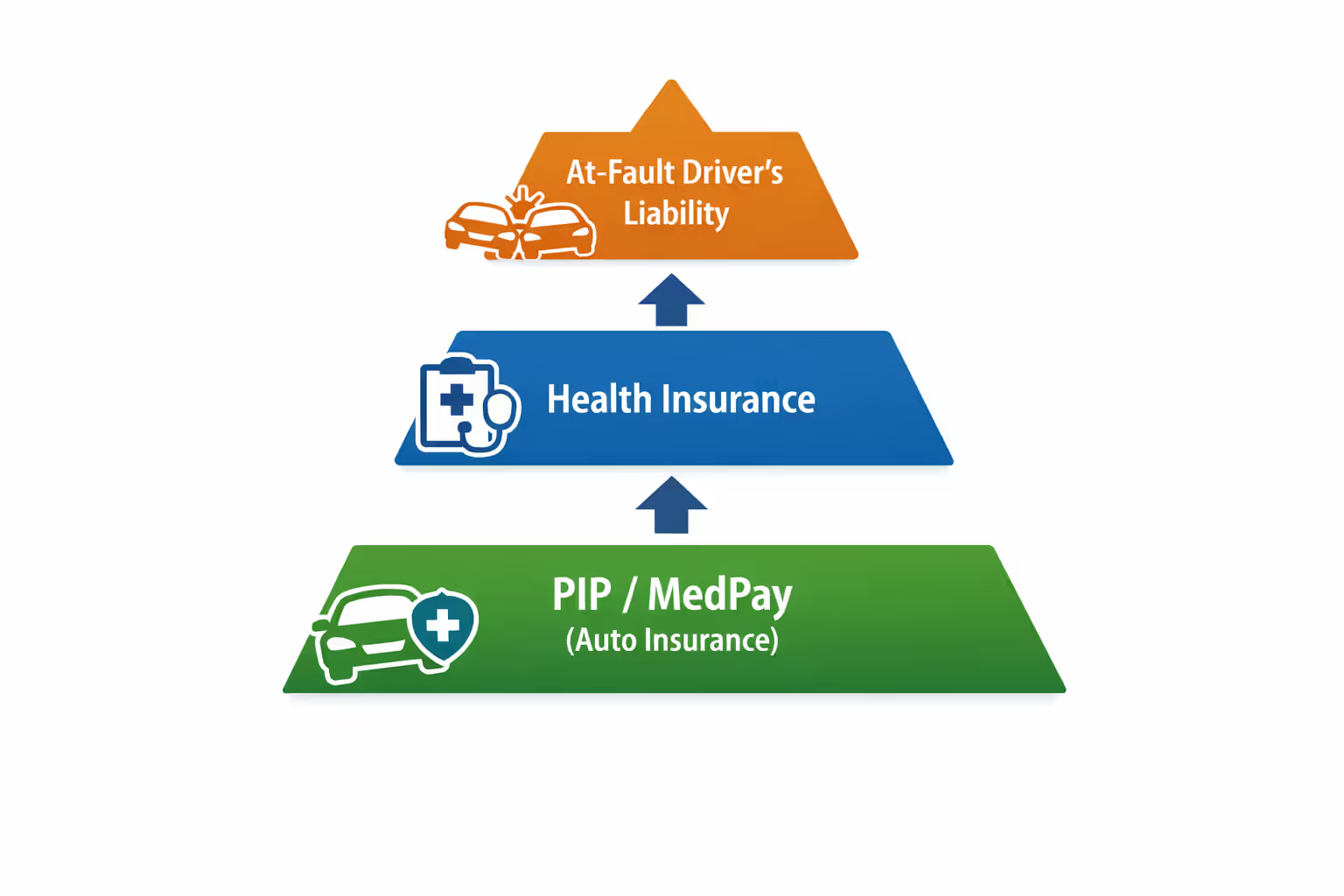

Health Insurance vs. Auto Insurance: Which Pays First

Understanding the payment pecking order between different insurance types prevents billing disasters and maximizes your available coverage.

| Coverage Type | When It Pays | Pros | Cons |

| Personal Injury Protection (PIP) | Pays first automatically regardless of fault (mandatory in no-fault states) | Quick payment processing, covers lost income and household services | Coverage caps typically range $10,000-$50,000 |

| Medical Payments Coverage (MedPay) | Pays first or alongside PIP, fault doesn't matter | Zero deductible, straightforward claims | Low maximum limits ($1,000-$10,000 common), unavailable in some states |

| Health Insurance | Steps in after exhausting auto coverage or when none exists | Much higher maximum coverage, protects against all injuries | Deductibles and copays apply, insurer can pursue subrogation |

| At-Fault Driver's Liability Coverage | Pays after settlement agreement or court judgment | Can cover complete damages including pain and suffering | Extremely slow payment, requires proving fault, often inadequate limits |

In no-fault jurisdictions, PIP handles payment automatically. Your health plan won't touch claims until you prove PIP limits are gone. Save every explanation of benefits from your auto insurer showing payments made and remaining balances.

In fault-based states, payment order depends on what coverage you carry. MedPay usually pays first with no deductible when you have it. After MedPay exhausts, health insurance takes over. The at-fault driver's liability coverage settles last, often many months after treatment wraps up.

Subrogation complicates this whole picture. When your health plan pays accident medical bills, they gain legal rights to recover those costs from any settlement you collect from the at-fault driver. You must tell your health insurer about settlement talks and might need to pay them back from your settlement money.

Certain health plans waive subrogation for smaller amounts or negotiate reduced payback. When you're pursuing a personal injury case, your lawyer can negotiate with your health insurer to shrink the lien amount.

Medicare and Medicaid enforce strict subrogation rules backed by federal law. You can't settle a personal injury case without resolving Medicare or Medicaid liens, and these government programs rarely negotiate.

Tips to Avoid Health Insurance Billing Problems After an Accident

Taking smart steps immediately after a crash prevents the majority of billing headaches later.

Alert all your insurers the same day. Don't adopt a wait-and-see approach hoping injuries won't develop—call both auto and health insurance within 24 hours. Early reporting creates a clear paper trail and preserves your policy rights.

Build a detailed file from the start. Create your accident documentation folder immediately. Snap photos at the crash scene of vehicle damage and visible injuries. Document every medical visit, medication, and symptom in a dated journal.

Know your auto policy's medical provisions before disaster strikes. Pull out your declarations page right now and check whether you carry PIP or MedPay and the dollar limits. Knowing this beforehand helps you anticipate coverage gaps.

Stick with network providers whenever possible. Even when billing health insurance for collision injuries, seeing out-of-network doctors creates higher costs and balance billing headaches.

Never sign unlimited medical release forms. The at-fault driver's insurer often requests sweeping authorization to access your entire medical history. Restrict any authorizations to records directly connected to accident injuries and specific timeframes.

Keep your insurers in the loop with each other. When your auto insurance pays certain bills and your health plan should cover others, verify both insurers understand what the other has handled. Forward explanation of benefits from one insurer to the other.

Catch provider billing errors early. Medical offices sometimes submit to the wrong insurance first or use incorrect billing codes. Review every bill before it goes to insurance and fix mistakes immediately.

Never accept settlement money without clarifying medical liens. Before accepting any personal injury settlement, get written confirmation from your health insurer about subrogation amounts owed. Settlements can collapse or shrink dramatically if liens surface unexpectedly.

Challenge denials immediately. Don't let rejected claims collect dust—your appeal window expires. Even denials that seem ironclad often reverse on appeal with proper documentation.

Get professional help for complicated situations. When you're dealing with severe injuries, multiple medical providers, and complex insurance coordination, a medical billing advocate or personal injury lawyer can navigate the system far more efficiently than you can alone.

Author: Ethan Bradford;

Source: blaverry.com

Real Examples of Auto Accident Health Insurance Claims

Real situations show how health insurance billing plays out in the messy real world.

Case 1: Maxed-out PIP benefits. Sarah got rear-ended at a stoplight and developed whiplash requiring months of physical therapy. Her auto policy carried $10,000 in PIP. After three months of twice-weekly therapy sessions, her PIP ran dry but her recovery wasn't complete. She filed claims with her health insurer, attaching documentation showing her PIP explanation of benefits with a zero balance. Her health plan paid the next $8,000 in therapy bills after her deductible and copays. When she eventually settled with the at-fault driver for $25,000, her health insurer exercised subrogation and recovered $4,800 of what they'd paid.

Case 2: Initial denial reversed through appeal. Marcus was crossing the street when a car struck him. He didn't own a vehicle and carried no auto insurance. His health insurer rejected his $12,000 emergency room claim, insisting auto insurance should pay first. Marcus filed an appeal with a letter explaining he owned no vehicle and had no auto policy, and the driver had fled the scene in a hit-and-run. He attached the police report documenting the unidentified driver. His health insurer approved the claim on appeal and paid the full ER bill.

Case 3: MedPay coordination. Jennifer carried both $5,000 MedPay on her auto policy and standard health insurance. A collision left her with a broken arm and $18,000 in medical bills. Her MedPay paid the initial $5,000 without any deductible. She then submitted the remaining $13,000 to her health insurance. After her $2,000 deductible and 20% coinsurance, her out-of-pocket hit $4,600. Since MedPay paid first and no third-party settlement was involved, her health insurer didn't pursue subrogation.

The biggest mistake I see is people not telling their health insurer the injuries came from a crash. When claims look like routine medical treatment but actually stem from an accident, it creates coordination nightmares that take months to fix. Always disclose the accident upfront, even when you assume auto insurance will handle everything

— Healthcare billing specialist Rebecca Martinez

Frequently Asked Questions

Successfully billing health insurance for vehicle accident injuries comes down to understanding how your health and auto policies coordinate, meeting documentation requirements precisely, and knowing how to fight claim denials. The process has complications, but most people do manage to get their health insurance to cover accident medical expenses when they handle procedures correctly.

Notify your health insurer immediately after any collision, even when you're confident auto insurance will cover everything. Assemble thorough documentation including police reports, complete medical records, and proof of auto insurance coverage or exhaustion. Submit complete claim forms within your policy's deadlines and monitor your claims closely.

When you receive a denial, don't assume it's final—proper documentation reverses most rejections. Learn how coordination of benefits operates between your various policies and prepare for potential subrogation if you're pursuing a personal injury settlement.

These steps protect your finances during recovery and ensure you tap into all available coverage from every source. When situations get complicated, consult a healthcare billing specialist or personal injury attorney who can guide you through scenarios involving multiple insurers and substantial medical expenses.